I’m getting a little weary of Charlie Munger quotes, to be honest. Don’t get me wrong, there’s no question that we recently lost an intellectual giant and a man of high moral character. His investment acumen and the genius ability to cut straight to the heart of a matter was legendary. But I think the elevation of his aphorisms to a form of business gospel reduces our own capacity to think for ourselves. He was just a man. Mortal. It’s ok to have heroes, but it’s not safe to put them on pedestals.

I imagine Munger could be insufferable at times. A real crusty bastard. Did you ever see his dorm design for USC? He must have been a dynamo when he was earning his capital as a lawyer and real estate developer. You probably regretted getting in his way. He was unapologetic about his desire to be rich and I’m sure he never suffered fools gladly. Ah, but yes, at his core he was among the wisest of the wise. So, after a long-winded preface, here is my Charles Munger quote: “If something is too hard to do, we look for something that isn’t too hard to do.”

I’m filing Welltower in the “too hard” category. Welltower (WELL) is a $62 billion market cap REIT that owns senior living facilities and medical office buildings. WELL is also a bank of sorts. It lends money to developers of properties. It has JVs with a bunch of developers. Some of the assets are leased triple-net to operators, many are operated directly by Welltower. The company is also a prolific issuer of new stock and an expert at churning real estate. It’s head-spinning and hard to completely grasp. This is a company whose CEO, Shankh Mitra, quoted Jensen Huang in the annual report. I’m not saying that running real estate for old people doesn’t have much in common with NVDIA. Ah hell, who am I kidding? This is the vibes economy. Everything runs on NVDIA.

In fairness to Mr. Mitra, he also candidly told a 2023 audience, speaking of the industry, “On average, in the last 10 years we haven’t made any money for capital [providers].” The oversupply conditions of the middle part of the last decade were just beginning to recede when COVID hit. Now, prospects for better economics seem to finally be destined for senior housing operators due to the unfeasibility of new supply and the rapid aging of the boomer generation. The stock market seems to agree. The stock has run up 24% since the start of the year as occupancy and margins vaulted upwards.

Despite Mr. Mitra’s humility, there’s not much for me to like about the company as an investment. A REIT with a mixed collection of properties doesn’t deserve to trade at a higher multiple than apartment buildings, and certainly not better than medical office buildings. The demographic story has legs, I’ll grant you that. But you can say that about Skechers slip-ons or Hey Dudes.

I was first intrigued by Welltower late in 2022, when Hindenburg published a report questioning the absorption of some troubled JV assets. The short-seller specifically cast doubt upon the relationship with Integra Healthcare Properties. There was a lot of mystery about Integra. Hindenburg called it a phony transaction. Integra’s website is still just a collection of canned photos of smiling elderly folks with zero substance (at least they updated the copyright date to 2024!). Crickets from the market.

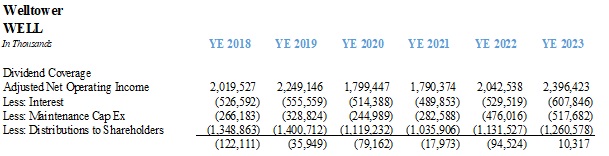

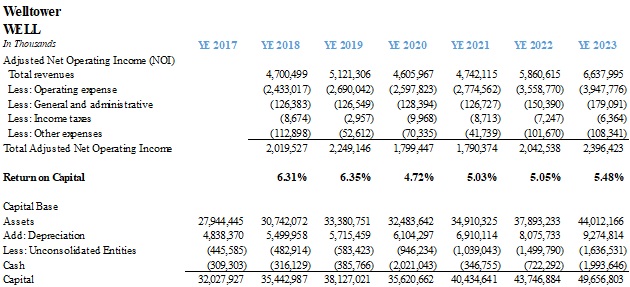

In my view, the only thing Welltower is guilty of is being exceptionally underwhelming. Welltower generated $6.4 billion in revenues during 2023. Property operating expenses absorbed 59% of revenues vs 52% of revenues in 2018. The industry sees itself getting back to pre-pandemic margins as staffing issues abate. I’m not so sure. States have ramped up calls for minimum staffing levels. The industry is also facing a lot of scrutiny about Medicare reimbursements. I don’t know enough about these challenges, so I can’t opine about the true risks to the company. I just know they exist.

What I can tell you is that I don’t think Welltower has much room to expand its distributions to shareholders above it’s current paltry yield of 2.35%. Once you deduct maintenance capital items from operating income and interest on over $15 billion of debt, there’s not much left.

No matter how many assets the company churns, the return on capital seems mired in the mid-single digits. The company has issued over $14.4 billion of stock since 2018, acquired $18 billion of assets during the period, while selling $9.9 billion. All this huffing and puffing hasn’t produced a formula that shows it can distribute increasing levels of cash to shareholders in a sustainable way. It is not unfair to say that some of the distributions are being funded with new equity. That’s not a great recipe. And for a CEO that says there aren’t many opportunities for new construction, the deal guys didn’t get the memo because Welltower had about $1 billion of construction in progress at the end of 2023.

Apparently, the market completely disagrees with me about the Welltower story. A 25% stock increase for a senior housing play is impressive. I am equally impressed that Welltower just raised over $1 billion of new debt at 3.25%. Is it pure debt? No, not for Welltower. It’s another dilutive offering. A convertible note due in 2029 that vests once the stock price rises 22.5%. I’m not sure who buys such debt when the five-year Treasury yield can be had for 4%, but it was probably a couple of fund managers who were feeling as frisky as Wilfred Brimley and Don Ameche in swim shorts.

So, I bid you adieu, Welltower. Low returns on capital, poor coverage on a low dividend yield, a churn of assets, acting like a loan shark, pumping new stock and forming a lot of unconsolidated JV’s… sounds like this one’s just too hard.

The easy column. I missed a fat pitch. I looked at it and didn’t have time to get my bat off my shoulder. It may not be too late, but I still need to dig deeper. Hat tip to Adam Block on social media who noticed Peakstone Realty Trust (PKST) was trading around $11 per share on July 10, giving the REIT a market cap of about $382 million. It sported a dividend yield north of 8%. Alas, it ran up 20% in two days. It still trades well below the $39 per share of last summer, so there may be juice left in the squeeze.

Peakstone had $436 million in cash at the end of March with a book value of real estate (excluding depreciation) in the neighborhood of $3.3 billion. Yes, there is debt of $1.4 billion. It costs Peakstone about 6.75% to finance the loans which roll over during the 2025-26 period. So, there’s loan renewal risk as well. But this is a pretty good portfolio of assets. The buildings consist of office and industrial space, but they’re mostly leased to single users with high credit such as Pepsi Bottling, Amazon and Maxar. Total square footage of the assets is 16.6 million. Net operating income for the quarter was $47.6 million. As far as I can tell, the market was essentially ascribing zero value to the assets at the beginning of last week. Even if you figure a monstrous 12% capitalization rate on an annualized run of quarterly NOI, there is adequate cushion above the debt. Seems like one to dig into. Easy? No. Simple to comprehend? Yes.