Are the Cornhuskers back? They seemed unstoppable in the first half. Fun times. The stadium was electric. The second half was a little underwhelming. I’m not so sure about the post-game field invasion by the students. Let’s hold off the pandemonium until we get some bigger wins under our belt. Despite all the flashy antics from the Sanders family, Colorado probably just wasn’t that good.

I rushed the field on a freezing November afternoon in 1991. We came from behind to beat Oklahoma. It was a Big 8 championship. In a testament to just how good our offensive lines were during the Osborne era, our quarterback on that day was neither Gill, Frazier, Crouch, nor Frost. Not even Gdowski. It was none other than the merely adequate Keithen McCant. Of course, he was backed in the I-formation by the Omaha Central grad, Calvin Jones. The future All-American 200-lb machine was only in his sophomore year.

Looking around Memorial Stadium, it is readily apparent that Nebraska is truly dependent upon agriculture. You can’t miss all those seed and insecticide banners among the flashing Dororthy Lynch signs. We tend to forget this in Omaha. We’re an ag state, but lately the state of ag isn’t so great. Corn at $4 a bushel won’t buy you much name, image and likeness recognition.

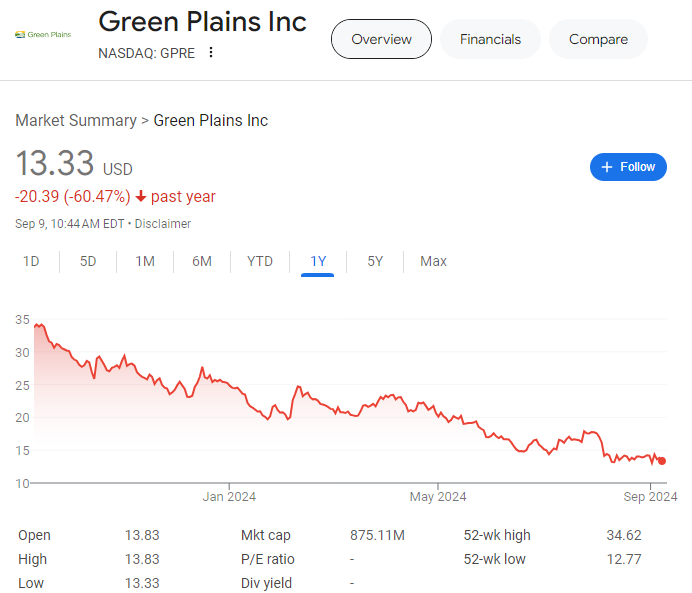

You might think that the ethanol business would be a good place right now. Reasonable gasoline prices and lower corn input costs should help the ethanol producers improve their margins. Unfortunately, Omaha’s Green Plains (GPRE) doesn’t seem to be heading in the right direction. The company is losing money and they are the subject of an activist investor campaign seeking to liquidate the business.

GPRE trades around book value; they’ve got some debt but it is mostly in the form of low-rate convertible notes. I think someone with better industry knowledge can decipher whether or not the stock is bargain at it’s nearly 52-week lows. It would have to be someone who can conduct a sum-of-the-parts valuation. I decided to not hurt my brain too much and search for a profitable ethanol producer instead.

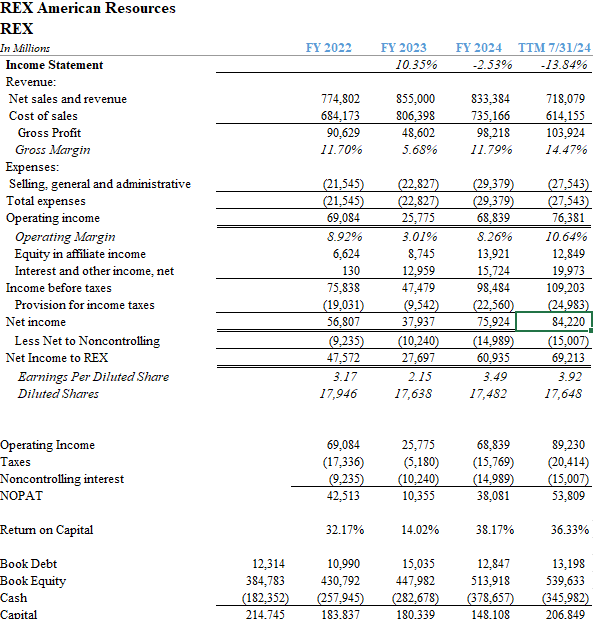

REX American Resouces (REX) seems to be the kind of ethanol investment that makes sense. The Dayton, Ohio company has a market cap near $750 million and zero debt. They had nearly $350 million of cash on hand at the end of July, and they are currently plowing profits into a plant expansion. Sales run about $800 milion per year with gross profits approaching $100 million last year. Operating margins for the fiscal year ending Janaury 2024 were above 8%. I generally dislike businesses that rely on government mandates to sustain their operations, but with nearly 40% of all corn being grown for ethanol it seems unlikely that the program will ever be ended.

REX plans to spend $150 million to expand its One Earth facility in Illinois. At the end of January 2024, entities affiliated with REX shipped approximately 716 million gallons of ethanol over the preceding 12 month period, of which 290 million gallons can be attributed to the parent company. Most imporantly, REX is generating returns on capital in excess of 30%. The strong balance sheet allows the company a wide berth to weather another cyclical turn in the corn and energy markets. The stock is trading well below it’s highs from earlier this year. REX looks like an attractive investment.

Peakstone Realty Trust

I’m still gnawing away at my Peakstone Realty Trust (PKST) analysis. The company has a market cap of $500 million and currently yields slightly less than 7%. They have a marquis client roster with a focus on industrial warehouses, and (gasp) office space. Peakstone has about $1.4 billion of debt to go with $2.5 billion of (undepreciated) real estate, but most of the interest rates are capped in the 4.5% range. The weighted average life of remaining lease terms exceeds seven years, so there is a long runway here. The company has sold off some troubled office. This one’s not for the faint of heart, but if you had to make a bet on babies being thrown out with bathwater, you should consider PKST.

Total net operating income for the trailing twelve months was $191.8 million. I capitalized these amounts by sector using 6.5% for industrial, 7.5% for “other,” and 20% for office and arrived at an asset value of $1.73 billion. Subtract the debt and add the ample cash balance of $461 million, and the net asset value is nearly $800 million. The stock is selling for $13.70 and the assets seem to pencil at $21 a share. You might even call this a margin of safety.

These aren’t self-storage facilities in Hastings, people. We’re talking Amazon warehouses here. The office? You’ve got the Freeport McMoRan HQ building in Phoenix, for example. Class A stuff. Is there more downside in office? Maybe. Is a 20% cap rate something I just pulled out of the air? A little bit. Certainly, the next step is to evaluate the office portfolio on a building-by-building basis and decide what is a zero and what is valuable. There’s also this troubling notion of the market being fairly efficient most of the time, and 25 cents aren’t just lying around waiting to be picked up. But sometimes that quarter on the ground really is there for the taking.