During the pandemic months of 2020, I sought guidance about apartment industry trends from the earnings reports of major apartment real estate investment trusts. The REIT stocks had fallen by about 35% from their pre-pandemic peaks, yet the CEOs struck me as fairly optimistic about their levels of renter demand. AvalonBay (AVB), Mid America Apartment Communities (MAA) and Equity Residential Trust (EQR) had all taken the opportunity to refinance debt in the 2% range and their dividends seemed safe. In the case of MAA and AVB, they were especially bullish on Sunbelt state demographics. Although urban properties experienced weakness (particularly for EQR), suburban locations were booming. The stocks rose significantly. By the end of 2021, MAA’s share price had doubled.

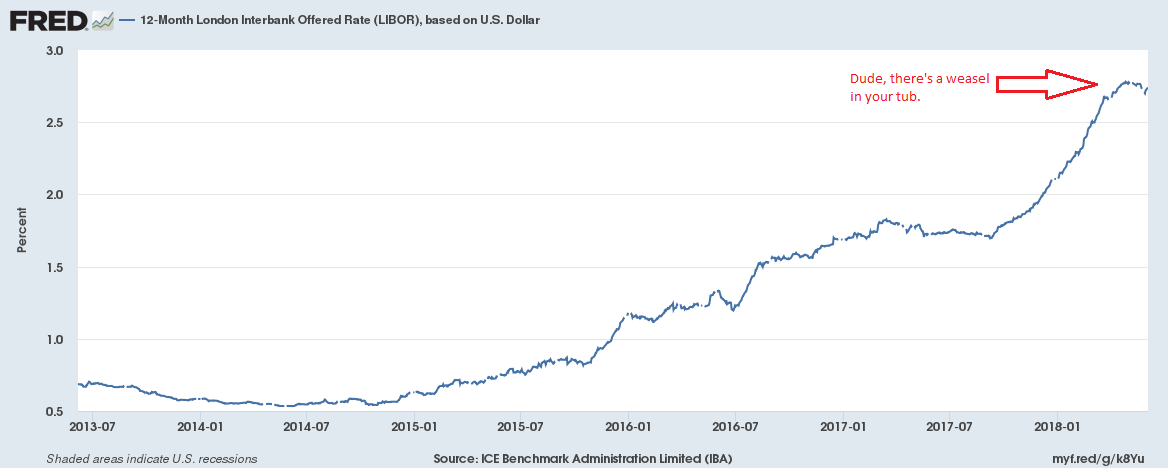

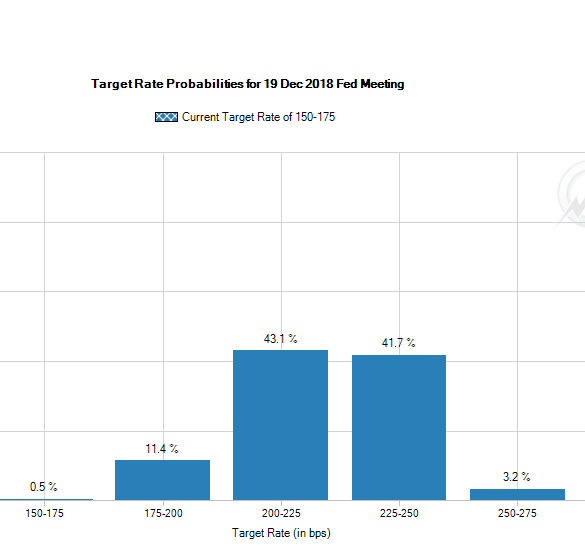

In hindsight, the massive amounts of fiscal and monetary stimulus introduced to the economy during 2020 and 2021 were generous gifts to the housing industry. It now seems apparent that these measures exceeded the output gap in the economy caused by the pandemic. Central banks are now facing extraordinary inflation pressures exacerbated by the Russian invasion of Ukraine. On April 21, 2022, Fed Chairman Jerome Powell said the job market was “too hot” and that a 50-basis point rate hike was “on the table”. Since that date, the Wilshere US REIT index has fallen 14%.

Memorial weekend offered me a chance to survey the REIT landscape once again. I present some nuggets from various companies below. This is my own research and interpretation of results, and my commentary should not be considered investment advice.

AvalonBay (AVB): A turn towards lending

AVB owns about 80,000 multifamily units and has a market capitalization of $29 billion. The dividend yield is 3.02%. AVB posted a healthy 15.9% increase in funds from operations (FFO) during the 1st quarter of 2022. The REIT continues to focus on developing new projects in the Sunbelt’s highest-growth metro areas. Five new projects representing about $700 million in investments are currently in lease-up at yields of 6.1%. The company estimates that its $4 billion development pipeline will have a yield-on-cost of 5.5%. Meanwhile, AVB exited 3 assets in the New York metro area during the quarter at a weighted average cap rate of 3.9%.

These development yields are probably satisfactory in a world where bonds still yield less than 3%, but AVB has calculated the math and decided that lending to other developers may be more profitable. AVB has established the Structured Investment Program to make mezzanine loans and preferred equity investments. They aim to grow the pool of capital to $500 million in 2-3 years. In addition to an expanded line of credit, AVB plans an equity share offering as needs arise in the amount of $495 million. AVB figures that mezzanine debt earning 8-12% is a low-risk way to deploy its cheap cost of capital. The Structured Investment Program isn’t a massive change of direction, but it would seem to indicate that runaway cost inflation has narrowed the opportunities to generate significant shareholder gains from development.

AVB has declined by 22.5% since it’s April peak, yet the company (along with MAA) remain the best ways to invest in the long-term Sunbelt demographic housing story.

LTC Properties: Skilled nursing challenges continue

I was intrigued by the 5.89% dividend yield available to shareholders of LTC Properties at current market prices. LTC has a market cap of $1.52 billion. LTC invests in seniors housing and health care properties primarily through sale-leasebacks, mortgage financing, joint-ventures and structured finance solutions, including preferred equity and mezzanine lending. LTC’s investment portfolio includes 202 properties in 29 states with 33 operating partners consisting of real property investments, first mortgages, mezzanine loans, working capital notes and unconsolidated joint ventures. Based on its gross investments, LTC’s investment portfolio is comprised of approximately 50% seniors housing and 50% skilled nursing properties.

My interest in LTC didn’t go far. Although occupancies continue to improve from the challenges presented during the pandemic, several operators in the portfolio remain under pressure. LTC, like AvalonBay has increased its focus on mortgage financing and mezzanine lending to operators and developers of senior housing. The rates charged to the developers and operators are well in excess of 7%, so the company should be able to leverage its balance sheet. Two weeks ago, LTC raised $75 million in senior unsecured notes at 3.66%. The company has a strong tailwind of demographics at its back, and occupancy should continue to recover. On the other hand, one must wonder about the credit quality of the operators in need of financing between 7.5% and 10% versus conventional bank loans.

The entire skilled nursing industry is facing tremendous pressure. Since the start of the pandemic, the skilled nursing industry has lost 241,000 workers or 15.2% of its total workforce. Wendy Simpson, CEO, also raised concerns about the efforts by Medicare to reduce reimbursement rates for skilled nursing. Last month, the Centers for Medicare and Medicaid Services (CMS) announced a $320 million cut in the reimbursement rate. This will undoubtedly put pressure on marginal operators. There is possibly an argument to be made that the stock has priced in these challenges, and LTC could capitalize on distress to increase its market share.

Blacktone’s REIT: Premium properties…at a price.

Blackstone (BX) has been aggressively growing it’s REIT over the past two years. BREIT has about $102 billion of assets and a net asset value of $66 billion. The annualized distribution rate is 4.5%. It is a non-publicly listed real estate trust that requires investors to be accredited, however the bar to invest is low – $2,500 is the minimum purchase. Fifty percent of the assets are concentrated in the residential sector and BREIT now owns 232,000 units including a massive portfolio of single-family rental homes. In July of 2021, BREIT purchased the 18,909-home inventory of Home Partners of America for $5.9 billion. BREIT will also become a major player in university housing by purchasing American Campus Communities for $13 billion. The deal was announced in April. Industrial represents 29% of the portfolio. BREIT also owns the net leases for the Mandalay and Bellagio hotels in Las Vegas and recently concluded the purchase of the 3,000 room Cosmopolitan through a joint venture.

Blackstone’s REIT offers investors a chance to earn a good yield on some of the finest real estate in North America. The share price is pegged to the net asset value, so an investment in BREIT should be insulated from the whims of the public markets. Blackstone has one of the most talented teams in the industry and can use its enormous balance sheet to uncover unique investment opportunities. However, an investor in BREIT needs to be aware of the fee structure. It isn’t cheap. There is a 3.5% broker commission fee and a 0.85% annual stockholder servicing fee. Blackstone, as the Adviser, receives a management fee calculated at 1.25% of net asset value. Finally, the Special Limited Partner (Blackstone) is entitled to 12.5% of the upside in NAV over a 5% hurdle.

The performance participation fee can be very large. In 2021, it amounted to $1.37 billion on revenues of $3.7 billion. The Special Limited Partner opted to receive this compensation in the form of shares at the end of December 2021. In January, a portion of the shares were redeemed for $566 million. In fairness, the massive scale-up in operations during 2021 and the cap rate compression that occurred during the year created a windfall that is unlikely to be as large in the future. The provision also contains a “claw-back” and “high water mark” condition which means that any declines in net asset value essentially subtract from the ability to earn the fee in the future. The fees are also not excessive when compared with what a private investor would face in a typical private real estate syndication transaction.

Due to the fee structure, investors should look at BREIT the way they would evaluate a private property acquisition: plan to hold the investment for longer than five years and let the Blackstone machine do the heavy lifting. I would also use BREIT as a sort of private property investment gut check. When evaluating investment prospects, Charlie Munger often asks himself, “Can it beat Wells Fargo? Can it beat See’s Candies?” In this case, ask yourself, “Can the deal I’m looking at for Shady Lane Apartments beat Blackstone’s REIT”? Lately, the answer is usually… “probably not”.

Broadmark Realty Capital: Cheap for a reason?

Another REIT that captured my attention was Broadmark Realty Capital (BRMK), a mortgage lender with a dividend yield of 11.44%. The market cap of the company is about $975 million and the stock is down by nearly 29% over the past year. BRMK makes construction loans, bridge loans and land development loans. Their website boasts the “Highest Degree of Leverage” with the ability to “loan against the completed value of your project, with no loan-to-cost requirements.” At the end of the 1st quarter of 2022, the loan portfolio had a weighted average interest rate of 10.4% and weighted average maturity date of 18 months. BRMK requires that their loans do not exceed 65% of estimated completed value.

BRMK had about $97 million of cash on its balance sheet at the end of the quarter, largely the result of $100 million of proceeds raised from an unsecured debt offering in November of 2021 at 5%. The company has about $931 million in loans on its balance sheet against the only debt of $100 million in unsecured notes. Apartments and senior living account for about 19% of the assets. Residential lots and single-family homes make up another 12% each.

It was unsettling to read that BRMK has over $186 million of loans in contractual default at the end of the 1st quarter of 2022. The company also has about $63 million in real estate assets on the balance sheet from foreclosures. BRMK has the ability to raise $200 million through at-the-market share offerings but has not issued any new shares through the end of the first quarter. It seems very possible that the market is pricing in a dilution of shareholders, or a dividend cut. Either way, loaning money to developers at high interest rates sounds like a great business, until it’s not.

Bert Hancock, May 31, 2022

Note: This article contains the opinions and observations of the author. No investment recommendations are being provided and no representations are made to the accuracy of the content provided.