My sister and I always knew it was a big deal when Dr. Sidney Freedman showed up on MASH. The psychiatrist wasn’t there to join the wise-cracking banter in the triage tent. And he sure wasn’t going to put on dresses with Klinger or pull pranks on Dr. Winchester. Somebody was about to get their psychological puzzle dis-assembled right there on national television.

In the final seasons of the comedy show’s 11-year run, MASH explored some dark territory. Even though MASH was set during the Korean War, just about everyone knew it was really about Vietnam. As the series went into its last few years, CBS seemed to stop pretending. Alan Alda’s hair grew pretty long, and so did his dramatic scenes.

Not only was it ground-breaking to put a psychiatrist on television in the 1970s, the writers gave him the rank of major. Dr. Freedman outranked the surgeons, BJ and Hawkeye. CBS seemed to be asking a generation of Americans burdened by the Vietnam era the ultimate question: What good is fixing a broken body if you can’t heal the soul?

It was actually our mother who clued us in to Dr. Freedman. Mom took a keen interest in Sid, just like she preferred the wit and charm of John Chancellor to the gruff Walter Cronkite. Mom had a master’s degree in social work, so Sid was her kind of people. Yep, when Dr. Sidney Freedman came to the camp, we knew it was time to go deep.

Having a mother with an MSW was like having Dr. Sidney Freedman right in our home. Well, in Mom’s case, it was more like a combination of Sid plus a mixture of Helen Reddy and Maria from Sesame Street. The childhood distress of silent treatments from girls in the classroom, peer pressure, embarrassment about acne – Mom was always ready with the right words. “Maybe they’re being mean because of their own insecurities”. Thanks, Mom!

They could make a modern spin-off of MASH with Dr. Sidney Freedman as the lead character. Only this time he wouldn’t be a shrink in a military hospital unit, he’d be running a private credit firm. Preferably one named for a Greek or Roman god. “Welcome to my office. Make yourself comfortable. Some of my clients sit, but most prefer to lie on the SOFR.” This script practically writes itself. It would be like having Dr. Wendy Rhoades on Billions, only better.

You need to have a degree in psychology to understand today’s markets. The keen ability to diagnose and treat delusional thinking is a prerequisite. Consider this: an electronic token generated by a computer algorithm has reached a price of $100,000. The “currency”, invented by Satoshi Nakamoto in 2008, is backed by no government and has few nodes of exchange except for illicit activities. Who is Satoshi Nakamoto? To quote Nate Bargatze, “Nobody knows.”

Let’s take it a step further. There is a company called MicroStrategy (MSTR). It is nominally a software business, but it really has only one purpose. It issues shares in the company to the public for which it receives old fashioned United States dollars. These dollars are backed by the world’s most powerful military, the largest economy, and is recognized around the globe as “legal tender for all debts public and private”. But instead of putting these dollars to work as investable capital for economic production, what does MicroStrategy do? It simply turns around and uses the real dollars to purchase electronic “crypto currency”.

MicroStrategy now owns $43.4 billion of this digital currency. Logic would tell you that the value of this company should be in the neighborhood of, say, and I’m just guessing here… $43.4 billion? Nope. The company trades with a market cap of $80 billion. “Investing” in MicroStrategy means that you are paying $2 to receive $1. And that $1 may not even actually be $1 because its digital money invented by some random guy with a computer in 2008.

There is a paragraph that I came across recently that seemed to leap from the page. Looking back from their perch in 1940, Benjamin Graham and David Dodd made this observation in Security Analysis: “The advance of security analysis proceeded uninterruptedly until about 1927, covering a long period in which increasing attention was paid on all sides to financial reports and statistical data. But the “new era” commencing in 1927 involved at bottom the abandonment of the analytical approach; and while emphasis was still seemingly placed on facts and figures, these were manipulated by a sort of pseudo-analysis to support the delusions of the period.”

Pseudo-analysis? Here’s another head-scratcher. Let’s see if we can understand the concept called “Yield Farming”. Yield farming is a high-risk investment strategy in which the investor provides liquidity, stakes, lends, or borrows cryptocurrency assets on a DeFi platform to earn a higher return. Investors may receive payment in additional cryptocurrency.

Got it?

Yield farming sounds very sophisticated. It also sounds an awful lot like something Charles Ponzi would have invented were he alive in 2025 instead of 1925. If you prefer time traveling to 1635 Amsterdam, you could easily replace the word “cryptocurrency” with “tulip bulb”. For those of you earning such a high return, I wish you well. When the music stops, someone will be holding an empty bag.

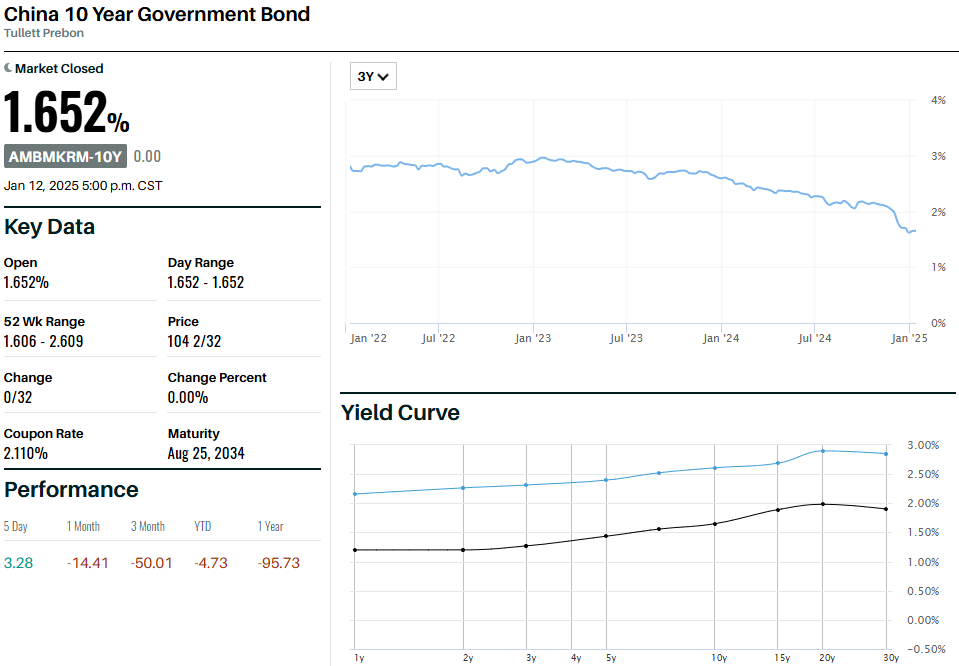

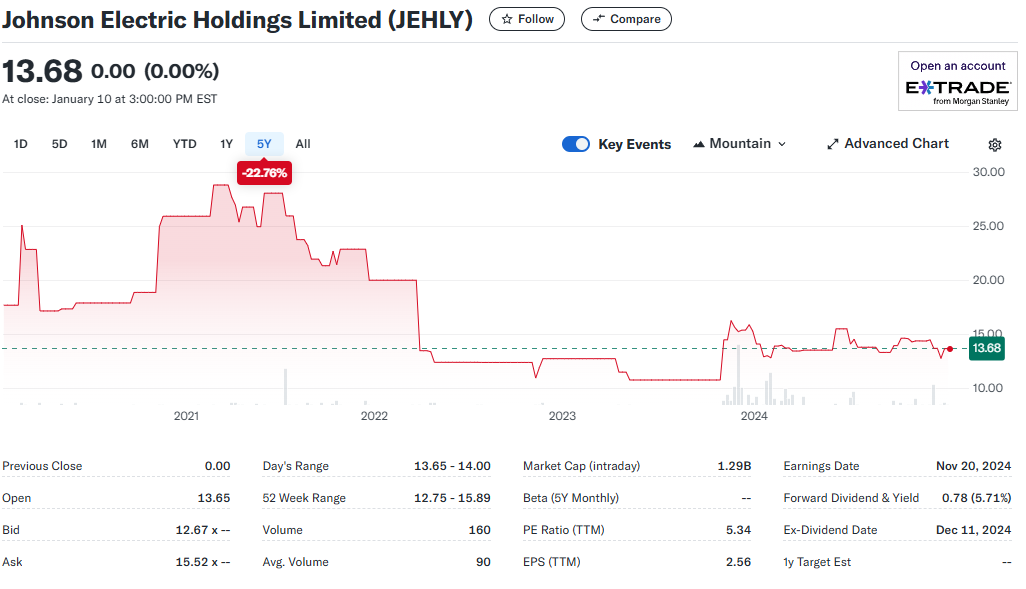

The hunt for rational market prices has led me to Hong Kong. Don’t laugh. The Hang Seng index is down by about 17.5% since its October-2024 peak. Fears of a Chinese debt-deflation spiral have begun to make the headlines as 10-Year Chinese bond yields have tumbled to 1.65%. China has too much real estate, not enough population growth, and massive levels of government debt at the local levels where municipalities became far too dependent upon the real estate market.

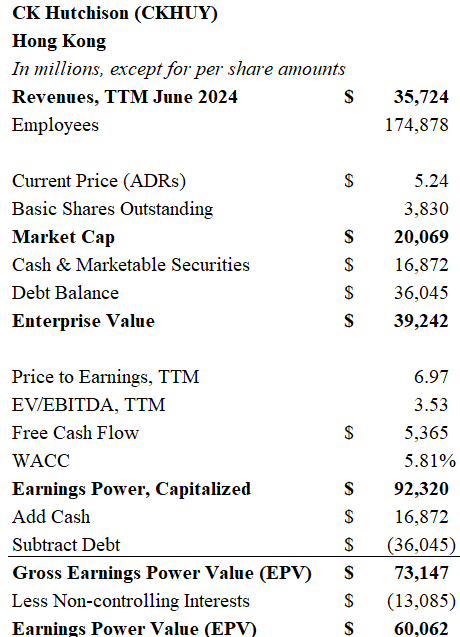

Amid the gloom, there are bargains to be found. Earlier, I wrote about the major discount to book value on offer at CK Hutchison (CKHUY). Meanwhile, Budweiser APAC (BDWBY) trades for 14 times earnings and pays a 6% dividend yield. The oil refiner, Sinopec Kantons (SPKOY) can be bought for a PE of 7.6 yielding 6.58%. But Johnson Electric is the biggest bargain of them all.

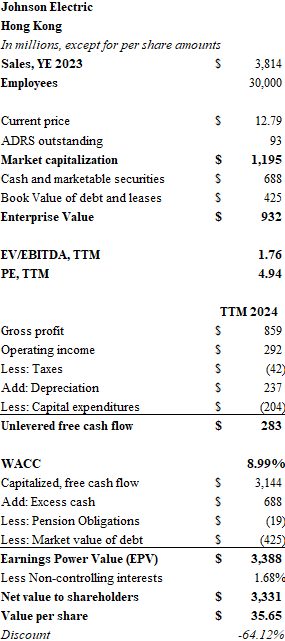

Johnson Electric (JEHLY) shares are valued at $1.2 billion by the market, trading hands at a price-to-earnings ratio below 5x for the trailing twelve-month period ending September 2024. The Hong Kong-based maker of small electrical motors racked up sales of $3.8 billion for the fiscal year which ended in March of 2024. Sales declined over the most recent 6-month period compared with 2023, but gross margins expanded from 22.2% to 23.6% resulting in gross profits over the trailing twelve months at $859 million. Net margins are in the 7.5% range, and operating income for the 12-month period amounted to $292 million.

Johnson Electric makes small motors which are an integral part of the automotive, factory automation, life sciences, and HVAC sectors. The automotive sector accounts for 84% of sales and therein lies the rub. Peter Lynch often warned about buying cyclical companies with low-PEs, and the current cycle may not be favorable for autos. Interest rates in much of the West have placed auto affordability beyond the reach of most consumers, and China faces a possible oversupply problem in its domestic EV market.

Johnson Electric can weather a cyclical downturn. The company was started by Mr. & Mrs. Wang Seng Liang in 1959, so this won’t be their first rodeo. The balance sheet is strong. Nearly $700 million of cash offsets the $425 million of debt. The company is rated BBB by Standard & Poor’s. PricewaterhouseCoopers is the auditor. Johnson Electric has over 1,600 customers with sales split roughly by thirds between Asia, North America, and EMEA. Over 30,000 employees manufacture more than 4 million products per year in factories across the globe.

The stock is exceptionally cheap. Unlevered free cash flow over the most recent 12-month period was approximately $283 million. Using a weighted average cost of capital of 9%, the earnings power value exceeds $3.1 billion. Deduct net debt and some pension obligations, and the intrinsic value of the equity is $3.3 billion or $35.65 per ADR. The current market price represents a 64% discount. The market value is a whopping 50% discount to book value. Meanwhile, the 5.7% dividend yield seems well-covered.

Johnson Electric may be in the early days of a difficult downturn for the global auto sector. The saber-rattling between China and Washington certainly isn’t helpful. Despite these concerns, a 60% discount represents a massive margin of safety. I will be adding Johnson Electric to my portfolio.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.