The Code of Hammurabi dates back to 1750 BC. These ancient laws contained the essence of the first banking contracts for managing loans. The farmer would borrow a bushel of seeds, reap the harvest, give the king about seven bushels of rye and keep three bushels for the family. In the modern parlance of Hammurabi’s descendant Jamiz ur-Dimon, a sound business endeavor earns positive leverage: the return on one’s capital investment should exceed the cost of borrowed money – the rate of interest. What happened if the loan required the farmer to pay back eleven bushels? It would probably end with the removal of a finger or three.

As crazy as things got during the pandemic boom, the basic premise of positive leverage remained intact. Purchases of apartment complexes yielding 4.5% bordered on insanity, but at least lending rates could be found in the 3% range. Now, we have entered a strange, new post-pandemic era. Buyers of apartments have reduced their purchase prices in order to earn a higher rate of return on their capital. Low 5% levels are the reported “capitalization rates” that many buyers are willing to pay. This sounds logical until one realizes that the cost of fixed rate debt today is about 6%. Watch your fingers.

Why would a buyer accept such a meager deal? Three reasons. One, they are willing to earn a return on their own equity that is below the cost of debt. This seems nonsensical. Very liquid low-risk alternatives abound in the form of humble T-bills or, say, Chevron stock with a 4.2% dividend yield. Two, some believe interest rates will decline in the future. There are signs that such joy awaits: The Fed seems poised to reduce rates as inflation slowly approaches the target 2% level.

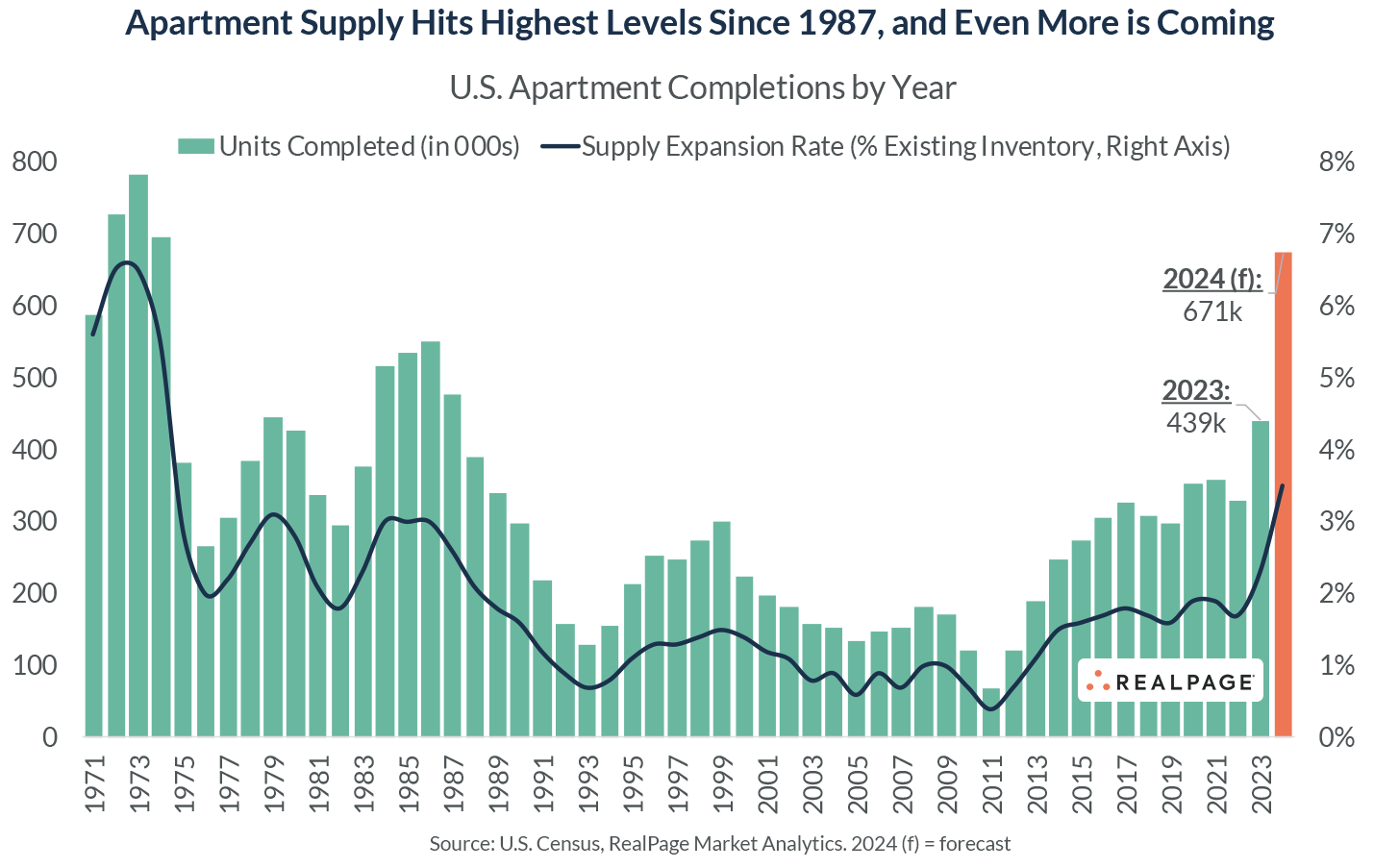

The third reason takes the opposite tack. There is a belief that inflation will lift rents faster than expenses in future years, and negative leverage will pleasantly reverse itself. This theory has merit. The greatest supply of apartments since the 1970’s is about to come to an end. Construction costs and interest rates have risen so high, that most new developments are unfeasible. Home purchases are out of reach for most Americans. The incumbents have a long runway to raise rents once the period of apartment oversupply abates. This is the theory behind KKR’s purchase of Lennar’s multifamily portfolio.

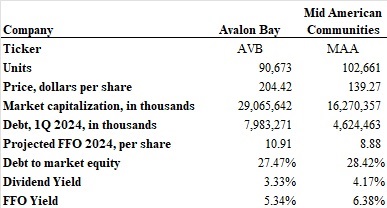

Publicly traded apartment real estate investment trusts (REITs) benefit from a low cost of debt and continue to earn positive leverage. Unlike their private competitors who must grovel for 6% permanent loan rates and 7% construction loan costs, the REITs have healthy balance sheets and can borrow at 5%. Mid-American Apartment Communities (MAA) and AvalonBay (AVB) are two of the largest landlords, and they are projecting returns of 6.5% on their (much reduced) development pipeline.

Both firms locked in low-rate long-term financing during the pandemic. Even as notes mature, healthy balance sheets at MAA and AVB provide pricing power in the bond market. In early January, MAA raised $350 million of debt at 5.1% for ten years – just slightly above a 100 basis point spread to the Treasury note. Assuming their development yields hold to projections and leverage is in the 30% range, they should be able to drive returns on equity to low 7% levels. Not fantastic, but sufficient to sustain dividend yields in the 3%-4% range and grow values in line with the broader economy. Both companies reported record low levels of resident turnover as home purchases have become less affordable.

Not everything is rosy for the REITs. The apartment supply hangover has arrived to pandemic boomtowns like Dallas, Atlanta, Houston and Nashville. Indeed, both MAA and AVB offered some sobering news: rents on newly vacant units were trending negatively in the first quarter. MAA, focused primarily on sunbelt markets, posted a negative 6.5% new lease rate. AVB was closer to negative 0.5%. Fortunately, high resident retention and rent increases of 5% on renewal leases kept the top line growing at both companies. Neither of these stocks is cheap. Taking projected 2024 funds from operations (FFO) – the preferred measure of operating earnings for a publicly-traded REIT – AVB trades at an FFO yield of 5.35% and MAA trades at a 6.43% forward FFO yield.

Meanwhile Farmland Partners (FPI) presents the perils of negative leverage. FPI owns and manages farms (177,000 acres) and has a market capitalization of $553 million. FPI shares peaked at $15 in 2022 and sit at $11.50 today. The dividend yield is a paltry 2.09%. Corn prices have round-tripped during the past five years from $4 per bushel in 2019 to $8 per bushel in 2021, and back to around $4.25 today. Not even Russia’s invasion of one of the world’s top grain-producing nations was enough to sustain wheat prices much higher than $6 per bushel.

Given these daunting agricultural prices, FPI doesn’t offer shareholders much value. The company generated $57.5 million in revenues in 2023 and had $31.3 million of EBITDA. The company spent about $25.6 million on interest and divdends to preferred shareholders, leaving just $5.7 million for common shareholders. This diminutive profit is not sufficient to cover the common shareholder dividends of $12.2 million.

FPI has been selling land to cover its dividend, and really, this is probably the best path forward – sell assets, reduce debt and retrench for the future. The floor on the stock is probably the market value of the land. A swag number of $6,000 per acre means there may be well over $1 billion of land vs $480 million of debt and preferred stock.

Positive leverage feeds your family. Negative leverage only feeds the king.

I remember watching the World Cup back in 2006. Italy won the tournament after Zinedine Zidane of France was sent off for headbutting Marco Materazzi in one of the most infamous moments modern football, er, soccer. The network must have thought Americans would get bored watching guys kick a ball around for 90 minutes, so they decided to scroll instant messages from worldwide fans across the bottom of the screen during several games.

Everyone remembers the headbutt and red card, but I remember a message on the screen. It was a Roma fan’s tribute to Italy’s beloved midfielder Francesco Totti that is forever etched in my memory. “Totti, Totti, Totti…We love him so much we name our dog Totti”. I don’t know what it was about this message of devotion to a piccolo cane italiano, but the little pooch earned a place in my heart. In my imagination, Totti is a gray Italian dachshund who loves to mangia soppressata. Oh Totti, ti amo.

I’m a day late. Already, my goal of therapy writing investment insights on a bi-weekly basis has gone the way of Monsieur Zidane – straight down the tunnel and into the locker room. But hey, rain or shine, we’re gonna walk Totti. Scrivi bene!

Before we get to the Totti of the matter, here’s a musical diversion that blew my mind. Seven Nation Army’s signature bass line is not from a bass guitar. It was actually played by Jack White on a Kay hollow-body guitar. According to Rick Beato, he used a DigiTech digital whammy pedal with the octave-down setting. Maybe I shouldn’t have been surprised. After all, Jack White is a masterful musician and the White Stripes were pretty much a drum/guitar duo. I never saw White Stripes live, so I had no reference point. Totti for you, my friend.

You like some Totti, you say? I think I have a couple of dividend ideas. Equity Commonwealth has a preferred yielding just below 6.5% and trades slightly less than the call price of $25. Equity Commonwealth was founded by the legendary Sam Zell to take advantage of commercial real estate bargains. Sadly, Zell passed away last year. Distress that he predicted in the industry was postponed due to all that pandemic juice. Present management sits on a cash pile of $2 billion and a handful of assets. They have said that if they can’t come up with a strategy to deploy the funds, they will wind down the business. The common is appealing, but the preferred is a fairly low risk way to park some cash.

A more adventurous dividend can be found in BCE, Inc. This is the old Canadian Bell. Like the AT&T of yore, it contains a lot of good (fiber optic and cellular networks, some tv networks), a lot of bad (legacy landlines, pension funds, debt), and some intangibles (37% of the Maple Leafs & Raptors, 20% of the Canadiens). The business is basically sound ($30 billion USD market cap) and the dividend is well-covered with a yield above 8.5%. The stock is down 50% since 2022 as government funds to boost the expansion of fiber optics networks were dialed back (pun for the boomers). They have curtailed capital expenditures and are laying off 9% of the workforce. I intend to do a deep dive on BCE because there may be some hidden value in a break-up and I like the positive Canadian demographic trend. I think you are adequately compensated for what is probably, at worst, a stagnant business. In a world of NVDA go up, 8.5% dividend checks sound like a snoozer but that’s where we be at. Vibes. 🔥

I took the Myers-Briggs test for the third time in my life yesterday. Wait for it. The first letter is an “I”. Shocking, I know. The rest of it actually was a surprise. I came in with an INTJ. Now, this made me well pleased. Uncle Warren is an INTJ. Zuckerberg, Musk? INTJ. F#%*ing Schwarzenegger is an INTJ! This is a small segment of the population. Rare air. Yes *silently pumps fist*.

I don’t recall exactly where I scored back when I took the M-B in my 20’s. I think it was INTP. Can’t remember. My Mom, a world-famous and passive-aggressive “I”, didn’t scrapbook those results. But this score contrasts sharply with my result from two years ago: INFP. I didn’t like that one. Too much feeling. Too many emotions. Now, it is true that some cool people are INFP’s. Creators. Bob Marley, John Lennon, Kurt Cobain, William Shakespeare, Johnny Depp. But not a lot of 4-star generals, Navy Seals, or NBA legends on that list. That’s probably not accurate. Dennis Rodman has got to be an INFP. You catch my drift here. Doris Kearns Goodwin isn’t pitching any biographies of INFPs to Penguin Classics. These are Oprah’s guests.

Questions naturally arise when you read the cast of characters. Did Arnold Schwarzenegger really sit for a Myers-Briggs exam? Did William Shakespeare truly prefer a quiet pub lunch with his mates to the crowded midsummer fayre? I am now on a search for the deeper meaning behind these two personality test results. INFP? INTJ? Who am I? Can I be both? Can I have Bob Marley’s soul and Zuckerberg’s bank account? It doesn’t work that way. Sorry. Or maybe it does? Maybe we are all coins with two sides? Janus with two faces. Jesters with two masks. Totti the man…Totti the dog.

Florida panhandle beaches are some of the finest in the world. Pristine white powder. Pensacola is not the kind of place I wanted to visit for lessons about the fleeting nature of human existence, yet there I was. Life is full of cruel twists and turns. Throw the genetic dice often enough and someone you love (maybe even you) will roll snake eyes. It’s not fair.

Philistines are met by the Holy upon arrival in Pensacola. Bible-clasping gentlemen stand on four corners proferring salvation to drivers. Can a young man in a white shirt and black tie with perspiration rings forming under the sleeves reach a sinner with averted eyes at a red light? Does it ever work? Does anyone ever turn into the Dollar General parking lot to ask for directions to the on-ramp of righteous eternal existence? One is all it takes. One driver. One soul.

If you’ve read this far, you may be thinking, “Death and salvation? Is this guy always so serious?” The answer is “hell, no”. I just sat down to ponder the weighted average cost of capital and this is the weighty path I took. I offer no salvation, no divine guidance. I’m not even very good with Google maps. But I decided to stand on a corner for the first time in a long time. Pen in hand. It’s good for my soul.

Mortality can be a pretty good business if you’re a skilled actuary. Promise to hand someone a large pile of dollars in the distant future in exchange for small cash payments over many years. Find enough healthy mortals to make lots of small payments, and immense wealth can be generated by investing these premiums before you have to return the piles of cash. The life insurance industry is really just about winning at the game of death. Outlast your policy holders and beat the clock. There are no Luka Doncic three-pointers at the buzzer on the court of life insurance. That’s because there’s no buzzer. The best life insurance companies tick along perpetually with Swiss precision.

Mutual of Omaha has been very good at the business of reinvesting insurance policy premiums. I decided to take a look at their most recent public financial reports. The venerable institution had over $9.6 billion in cash and invested assets at year-end 2023, and nearly $4 billion of policy holder surplus. I wanted to look at their financials to see how they are paying for the largest development in Omaha: the $650 million skyscraper that will soon become the tallest building on the horizon. I learned a few things reading their report:

- Similar to most real estate developers, a big slug of leverage is invloved: At March 17, 2023, “the Company entered into a $550,000,000 senior unsecured credit agreement that is available for purposes of funding the new home office building.” In real estate terms, Mutual of Omaha is just like Bruce Dickinson – they put their pants on one leg at a time.

- The bond bear market has not been kind to the fixed income portfolio. The worst sell-off of bonds in a generation left Mutual of Omaha with over $526 million of gross unrealized capital losses.

- Mutual of Omaha has $214 million of short-term outstanding borrowings from the Federal Home Loan Bank. This represents a significant increase from the $40 million borrowed at the end of 2022.

I don’t know that many conclusions can be drawn from these observations. Personally, I would not have sunk 7% of my investable assets in a building that will likely be worth 20% less the day it opens. But Mutual of Omaha is a perpetual financial insitution, not a cyncial and balding middle-aged guy with a computer and a finite time horizon. They will hold the asset for longer than its depreciation schedule and it is an emphatic statement of corporate strength. In other words, $650 million is a fair price to pay for permantently establishing your image as a solid financial giant when such an image is essential to your brand. There’s a reason why Louis Vuitton sells bags in a palace on the Champs-Elysees instead of a Carrefour in Nanterre.

Second, the losses on the bond portfolio present no threat. Unrealized losses are actually much improved from 2022 when they amounted to over $690 million. Mutual of Omaha matches its investments to its policy obligations and they epitomize the definitition of “held-to-maturity”. There is no risk of an imminent loss of capital. There is a downside, however, in the form of opportunity cost. $500 milion could be earning 2-3% more per year. Instead, Mutual of Omaha has to let those underwater bonds mature. Because the only thing worse than unrealized losses are…realized losses. It’s just the sort of income you might wish you had available if you were to, say, pay for a new office building.

Finally, the Federal Home Loan Bank borrowing raises some concerns. The FHLB window was opened wide last spring when some banks ran into liquidity issues. Are there liquidity issues in the Mutual of Omaha portfolio? It seems unlikely, yet the $175 million increase didn’t suddenly materialize out of nowhere. Calls were made. Flesh was pressed. Deals were done. Frankly, I did not even know that insurance companies could borrow from the FHLB. This was news to me. Apparently $134 billion has been loaned to insurers, and the low cost of funds present a wonderful arbitrage opportunity. Imagine that. A taxpayer-backed hedge fund mechanism. I’m not sure how I feel about being the backstop for more leverage in the housing system. But as the saying goes, “Teach a man to arbitrage…”

So, there you have it. Dante might be proud. We started our little story with damnation and ended with a cursory look at the financial results of an insurance company specializing in death benefits. As a wise man once sang, “Don’t fear the reaper.”