By now, just about everyone knows the boiling frog metaphor. The business parable now sits among the regal pantheon of Vince Lombardi quotes, TedTalks about body postures, and the mystical epiphanies which occur when you gaze deeply in your Steve Jobs mirror. So let’s take the boiling frog story and give it a new level of sophistication. We’ll call it the Big Lebowski moment. This moment occurs when you are chilling out in your bathtub, just like The Dude. Your candles softly glow, the water is nice and warm, and you probably just had some help to induce your tranquil state.

The Dude Abides

For real estate developers, this can be like the construction phase of the project. You’ve done the heavy lifting of designing the building and gaining approvals from the city. You’ve negotiated the contracts and obtained your financing. You sit back a little and marvel as your dream leaps off the paper (or digital file) and becomes reality. This building is really happening. Sure, you will worry about the rogue subcontractor, the deadlines that may ebb and flow, and the weather, but if you’ve set yourself up with a well-planned project you will enjoy the next 18 months.

Once construction winds down, the stress starts kicking in. Will my glorious creature be the pony that every child wants to ride or do I have an old nag who buries its nose in clover when a rider approaches? Or, even worse, did I open one of those dodgy carnivals in a parking lot of a vacant retail strip center and my ponies just got quarantined by the Douglas County Health Department? Rents get adjusted, special lease incentives are offered, sweat beads appear on your brow and the pulse quickens. In Big Lebowski terms, The Nihilists have just arrived while you’re sitting in the tub, and they’ve started to break your stuff in the living room.

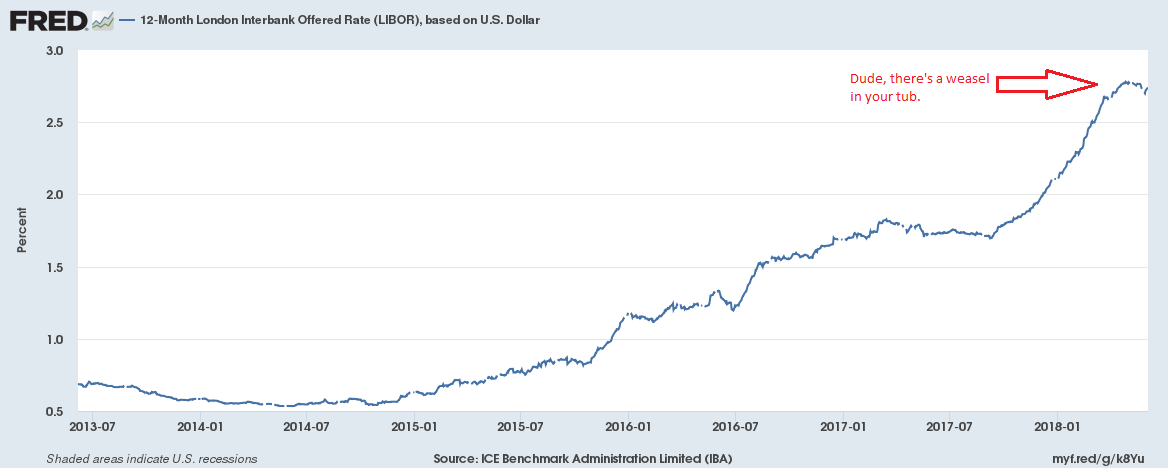

It gets worse. The Nihilists have brought a weasel with them (Hey, is that a marmot, man?). They throw the weasel in the bathtub. All hell breaks loose as the furry ferret turns into a screeching water snake keen on drawing blood from a sensitive region of the body. The tranquil tub becomes a frothing cauldron. For real estate developers, the angry weasel represents their debt. Real estate projects are highly dependent upon leverage. Most developers borrow 70% to 80% of their total project costs. Rising interest rates can threaten even the best developments.

Most construction loans have an interest-only period that terminate about 24 to 36 months after the start of construction. The end of the term is often referred to as the “conversion date”: the date at which the loan resets. On the conversion date, the interest rate adjusts to the current market level and the developer must begin paying some principal on the loan. For the past five years, rates have been in an innocuous range around 4%. Conversion dates came and went without much trepidation. Now, rates have risen dramatically. Many construction loans that were marked at LIBOR plus 3% two years ago will soon reset in a new and very weasel-ish world of 5% rates. One-year LIBOR sat at 1.73% in June of 2017, today it sits at 2.74%.

Well, that’s not so bad, you may say. After all it’s only 1% higher than it was a year ago. Yes, but the problem is exponential: your cost of money just went up by 20%. If you borrowed $10 million to build 100 apartments, you now face an additional $100,000 per year in interest expenses. On a per unit basis, that’s $83 per unit per month that you need to generate. From where I sit in Heartland, USA, $83 per month is a substantial amount of money. It’s probably a 10% increase on a one-bedroom apartment. My sister lives in San Francsco where they step over $100 dollar bills like soiled pennies, but here the number is the difference between two tanks of gas or an upper deck seat to see Kendrick Lamar. In other words, its a problem.

In a market facing over-supply, the pressure could become intense. Apartment construction has exceeded rates of household formation for the past six quarters. Higher interest rates will add to the challenges and pose a threat to developers in a way that has not been witnessed since 2007.

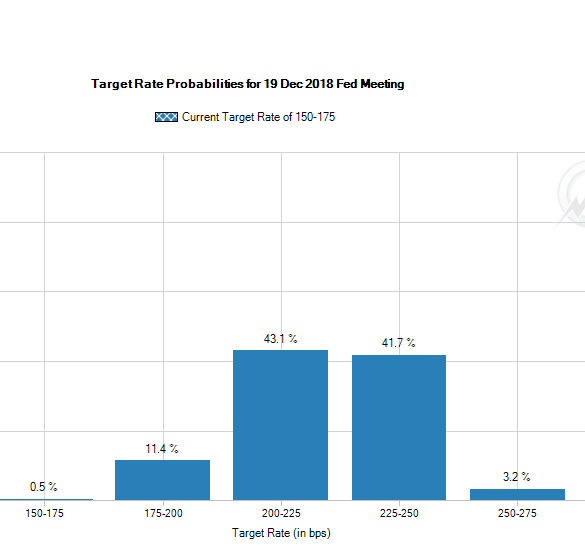

The interest rate environment places the Federal Reserve in a complicated position. The effective Federal Funds Rate is 1.75% and a 25 basis point increase is expected this week. Right now, markets place a probability of 41.7% on rates landing in the range of 2.25% to 2.5% by the December 2018 meeting.

Source: CME Group

There are three problems with this outlook:

- The 10 Year Treasury Yield stands at 2.96%. A surge in short term rates would almost certainly invert the yield curve – a signal that portends most recessions. The 5 Year Treasury is already at 2.80% which demonstrates a flattening yield curve.

- LIBOR rates track short term Fed Funds rates. Most short term financing is set on LIBOR plus a spread. If you extrapolate my example above regarding apartment rents to the entire economy, I do not believe that borrowers can cope with another 1% increase in the cost of short term funds.

- Increased rates will draw capital to the US and strengthen the US Dollar. The foreshadowing of this momentum has already set central banks into a frenzy of currency market intervention in Turkey, Brazil and Argentina. If the Mexican Peso joins the crowd, you could have a full blown currency crisis like 1994 or 1998.

The Mexican Peso (MXN) has fallen dramatically against the US Dollar (USD) since April. Source XE.com Currency Charts

Therefore, Jerome Powell must walk a tightrope. He must work to reduce inflation pressure and curb lending excesses, yet the risk of a recession rises with each quarter-point increase. He surely does not wish to create a lending crisis.

The intersection of interest rates, inflation and housing is even more complicated. Most measurements of the CPI show that housing costs are the major driver of inflation. I highly recommend reading the Bloomberg piece on the topic. There is some frustrating irony here: my industry, the one most susceptible to the risks of rising interest rates, is also the cause of the inflation which requires the Fed to raise rates. It’s a logical spiral that circles the drain like dirty water in a candlelit southern California bathtub.

A couple of years ago I published my views about the supply and demand of multifamily rental housing in the Omaha metropolitan area. My conclusion was that softness would appear by late 2017 due to an acceleration of supply. I have been pleasantly surprised by the continued strength of the market. Occupancy levels are at 95% or better in most parts of the city.

Unfortunately, the day of reckoning has only been postponed, not cancelled. I believe 2018 will be the first year since 2010 that landlords will be caught short-handed. While I don’t see vacancies rising to the 10%-plus levels we experienced during the dark days of 2004-06 when just about anyone with a pulse was purchasing a house, any pullback in occupancy will feel painful simply because we haven’t been exposed to much adversity in recent years.

Omaha has become large enough now, at nearly 950,000 people, that submarkets can have widely disparate experiences. Northwest Maple Street is an entirely different beast from the Blackstone neighborhood. However, on a macro level, a decline in occupancy of 2-3% seems possible.

There are two reasons why my prediction of market softness has been delayed until 2018. Omaha has grown faster than I thought and developers have been mindful of delivering units at a slower pace.

On the supply side, it’s hard not to ignore the revival of midtown Omaha. Over 1,200 apartments are under construction or just opening south of Dodge and east of 72nd St. Prudent builders released units to the market more slowly than anticipated, however, and the real impact will be felt in 2018 and 2019 when major projects in Blackstone, Aksarben Village and other midtown neighborhoods hit the streets.

On the demand side, population and employment growth have been stronger than I thought possible. We have exceeded 1% population growth for the past few years with a high degree of contributions from international and domestic migration.

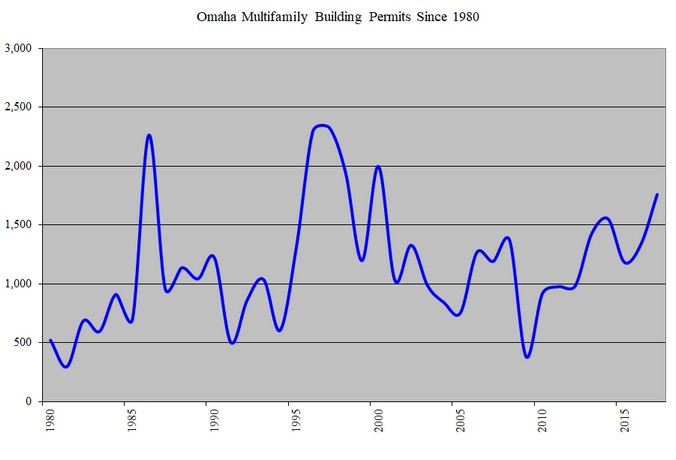

My theory has been for many years now that Omaha can absorb 1,200 apartments per year without disrupting decent rent growth in line with inflation. During the recession multifamily permits dropped precipitously to just over 300 units in 2009. Pent up demand and pinched supply signaled a robust market from 2010 – 2016. Now supply is exceeding the 1,200 unit “magic number”. By 2019, Omaha could experience a glut of 2,000 apartments. In the grand scheme of all rental housing, this amounts to about a 2-3% weakening in occupancy levels. This is not disastrous when taken in the context of the metro area.

The pain will be be felt at the top end of the market. The 2,000 unit overhang will attempt to command units nearing $2 per square foot due to the massive building cost and land inflation since 2013. Geography matters. East Omaha will suffer the brunt of the weakness. Developers are correct to recognize the trend towards urban living. It’s unfortunate that they all decided to recognize the trend at the same time.

Like most booms, the story is more about cheap money than it is about demographics. There was a moment this past summer when the 10 year Treasury bond yield began to head towards 3%. Cassandras who had been warning for years that hyperinflation was lurking just around the corner and gold was a safe haven, suddenly began to sound like they were on to something. But as the summer waned, the Treasury dropped to nearly 2% again. It is only about 2.3% now. This rate reprieve has given green lights to many new projects.

Forecasting interest rates is a fool’s errand, but what can not be disputed as we enter our 10th year of extraordinary central bank intervention in the money supply, is that asset price inflation has been rampant. Stock market multiples are as high as they were during the dotcom bubble. If you call a broker looking to purchase an investment property today, you will go straight to voicemail.

The problem is not one of America’s sole making. The Federal Reserve is planning to decrease its purchases of agency bonds and Treasuries. Under normal circumstances, this would signal a dramatic rise in rates. But America does not operate in isolation. Japan, Europe and China have been increasing their supply of money at an ever faster pace. If the US Treasury rises to 2.75%, a fund manager in Zurich will surely be buying when the alternative is less than 1% domestically. The yield on American bonds can not escape the gravity of sub – 2% yields elsewhere. The international market for capital won’t let this US diver come up for air.

The truly international scope of cheap money infects housing as well as securities. Try bidding on properties in San Francisco, Sydney, Vancouver or Toronto and you’ll see what I mean. Even in Omaha, the numbers are distorted. When developers can continue to borrow money at cheap rates, the estimate of risk gets diminished.

I identify five major risks threatening the Omaha apartment business today: The first is the persistently low interest rate cycle. As mentioned above, the cheap cost of capital is giving green lights to developers who might have otherwise tapped on the breaks by now. The second is student loan debt. Young people are the lifeblood of new apartments. They are under tremendous financial pressure today due to the enormous amount of college debt that’s been incurred. While we have a robust economy with local unemplyment rates hovering near 3% today, a slowdown in the economy would stall wage growth and diminish the affordability of high rents. Student loan debt has surpassed the eye-watering level of $1.4 trillion dollars. Yes, that’s trillion with a “T”. Number three is the challenge facing university enrollment. UNO has been growing but is nowhere near it’s target of 20,000 students by 2020. Small colleges are shrinking or disappearing (Grace University is the most recent casualty). National college enrollment peaked in 2011. Fourth, the possible limitations on international workers from the current administration could dampen population growth. Omaha grew by 9,800 people in 2016 and over 1,000 represented international migration.

The fifth challenge facing apartments deserves its own paragraph. The apartment market must also compete with its big brother: the single family home market. The very slow recovery in single family home starts has worked in the apartment market’s favor. Peaking near 6,000 units during 2005, the supply of houses has only now climbed back above 3,000 on an annual basis. The lack of inexpensive new homes has prolonged the renter experience. But this trend will reverse if the economy stays strong and wages continue to grow. Single family permits are on an upward trajectory. When coupled with multifamily permits, the entire supply of housing is exceeding levels not seen since 2008. The same low interest rates that help apartment developers are the double-edged sword that drives house affordibility.

What’s more, I do not subscribe to the belief that there has been a permanent paradigm shift away from homeownership. Young people still want to start families. When they have children, and if they have the means, they will move to Elkhorn and Sarpy County where pristine schools beckon. Homeownership will probably never return to the insanity of the mid-2000’s but the dream of owning a home did not vanish from society. Millenials may have delayed their family expansion, but the overwhelming human instincts of procreation and self preservation have not ceased. And there’s no place better than a good suburban home for this most American of pursuits.

There aren’t many places in Omaha where you can see an outdoor concert, grab drinks and dinner with friends, take in a movie, and then walk home. We’ve been proud to call Aksarben Village home since 2009. We like it so much, we are inviting more of you to join us.

Alchemy Development has recently purchased two lots adjacent to the new HDR headquarters building in what is informally known as Zone 6. The plan calls for 108 apartments in two separate buildings. Each one is five stories tall, serviced by elevators and indoor garage parking. A redevelopment agreement was signed with the City of Omaha this past summer, and construction is slated for 2018. The buildings will open in the first part of 2020 when HDR welcomes it’s 1,200 employees to its new tower.

Accredited investors seeking information on the new Zone 6 apartment project may contact us now.