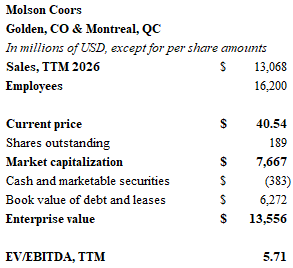

The alcoholic beverage industry has been experiencing a secular decline since the pandemic boom. So, borrowing an expression from the Hormuz-constrained oil industry, are we nearing tank bottom? Molson Coors, the brewing giant formed through a 2005 merger, looks like a bargain by most standard metrics.

Molson Coors had sales of $13 billion in 2025, representing a 5% annual decline. First quarter revenues ticked up slightly, and management expects 2026 to be a year of stability. The company trades for an EBITDA multiple of 5.7x. The 4.6% dividend yield is well-covered. Cash flow from operations was $1.8 billion dollars in 2025, so there was plenty left over for share buybacks and debt reductions after paying capital expenditures of $700 million and dividends of $376 million.

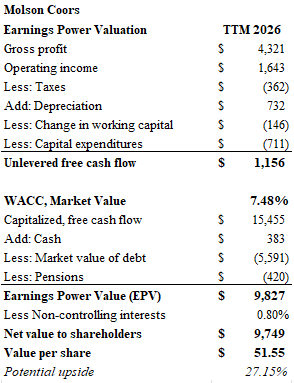

As usual, I calculated the intrinsic value of the business using the earnings power value (EPV) method favored by Bruce Greenwald and his value investment acolytes. This math simply takes normalized unlevered free cash flow and divides it by a weighted average cost of capital to arrive at a gross value for the business. Adjustments are made for cash and debt on the balance sheet to arrive at a net value, or “intrinsic value”.

My intrinsic value calculation shows that the shares trade for a 21% discount. Over the trailing twelve months, unlevered free cash flow amounted to approximately $1.15 billion dollars. I applied a discount rate, or weighted average cost of capital (WACC), of 7.5%. This percentage reflects an equity cost of 9.9% and an after-tax debt cost of 4.1% with a weight of 42%. The resulting quotient is $15.5 billion of capitalized value. Adding cash and subtracting debt and pensions of $6 billion leaves a value of $9.8 billion, or $51.55 per share.

I added some shares of Molson Coors to an account focused on generating income because I think the dividend is well-protected. The yield is better than Treasuries, and much of the downside is priced in. However, I am reluctant to take a large swig at the TAP. The return on capital in 2025 was only about 6.7%. This is less than the WACC of 7.5%. Molson Coors booked $3.6 billion of impairments in 2025, and I suspect more could be in the offing as management seeks to rationalize production. Also, to state the obvious problem, there is no foreseeable sign of growth in the alcohol industry. Finally, margins will continue to come under pressure from high aluminum costs.

Where’s the upside going to come from? Continued share buybacks is one answer. A takeover seems less likely since most brewers are struggling with their own debt hangovers. A leveraged buyout led by the Molson family is my other idea. But why add more debt? This one is for the patient coupon-clippers.

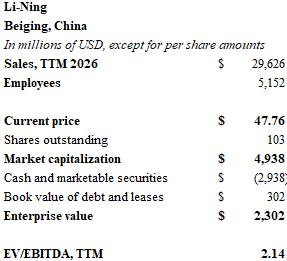

I had much more fun researching Li-Ning, the Chinese athletic footwear and apparel maker. Shares of the company appear to offer an exceptional bargain. And while sales growth is in the low single digits, sales are growing. A lot of the coverage of Nike $NKE and Lululemon $LULU has focused on various management missteps. I suspect one underreported factor has been the role of Chinese competition. The stature of Chinese athletic brands has been rising, and nowhere is this more apparent than on the feet on some of the NBA’s most talented players.

While Nike continues to dominate the NBA shoe league table with the Kobe Bryant, Michael Jordan and Kevin Durant franchises. Chinese brands have made significant inroads. Anta Sports $ANPDY is the largest Chinese brand (another undervalued stock, in my opinion), and has just signed Kyrie Irving to a major deal. 361° features two-time MVP Nicola Jokic. Meanwhile Peak and Rigorer have also made inroads. But the largest deal was recently made by Li-Ning who signed Steph Curry to a $400 million 10-year deal. Curry joins a stable of stars led by Dwayne Wade. The former Miami Heat legend teamed up with Li-Ning several years ago. The Way of Wade line from Li-Ning garners rave reviews from fans, athletes, and “sneakerheads”.

Li-Ning trades in Hong Kong and over the counter with the symbol $LNNGY. At the recent price of $48, the market cap is just below $5 billion. The company has virtually no debt and approximately $300 million of lease obligations. Cash on the balance sheet is an astounding $2.9 billion. They can afford Steph’s contract. With 2025 sales of $4.3 billion and EBITDA of $825 million, the EV/EBITDA multiple is only slightly above 2x. The chart isn’t pretty. The hype from the pandemic spending boom has evaporated, and shares are down over 80% from their peak.

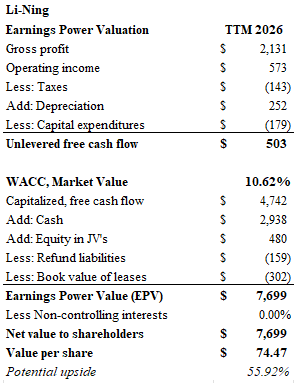

I think Li-Ning shares trade at a substantial 50% discount. Using a weighted average cost of capital of 10.6% and unlevered free cash flow of $500 million, the capitalized value is roughly $4.8 billion. Adding the $2.9 billion of cash and the company’s JV investments while subtracting those leases and about $160 million of warranty liabilities leaves an earnings power value of $7.7 billion or $74.50 per share. It appears that Li-Ning has 56% of potential upside.

The competitive landscape of athletic wear is challenging, to say the least. Hoka $DECK and On Running $ONON are brands that didn’t even register a pulse a decade ago, now they are staples. Meanwhile, spending on athletic apparel could come under pressure as European and American consumers grapple with higher energy costs. Chinese consumers are in year five of a major retrenchment due to the collapse of housing prices. Despite these headwinds, Li-Ning represents an exceptional opportunity at the current market price.

Until next time.

DISCLAIMERThe information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2026-06-28 15:28:322026-06-28 15:33:08Way of Wade

Chris Hohn’s interview with TheFinancial Times was sobering. He contends there are only about 200 companies in the world that are investable. These are the privileged purebreeds who can raise prices with impunity. Naturally, shares of these champions trade at massive premiums to the rest of the market. Exhibit A is Hohn’s largest holding, GE Aerospace which profits from a duopoly in the jet engine market. Sadly, trading at 38 times earnings, it’s no bargain.

When all the best companies are priced to perfection, what’s a value investor supposed to do? It reminds me of the Wall Street scene at 21 Club. Gordon Gekko instructs Bud Fox, “Cover the Bluestar buy, and put a couple hundred thou in one of those bow-wow stocks you mentioned. Pick the dog with the least fleas. And buy yourself a decent suit. You can’t come in here looking like that. Go to Morty Sills. Tell ’em I sent you.”

I know the feeling, Bud. When the pedigree canines are too expensive, you have to find a few mutts. I’m talking about finding a loyal hound, not the pug crossed with a Chihuahua. Maybe it’s a beagle that had a fling with a golden retriever. Or the Australian sheepdog who spent a spa weekend at Labrador camp. Man’s Best Friend. The kind of pooch that will fetch your slippers, carry a keg of brandy and guard your kids. Those are the mutts I’m looking for.

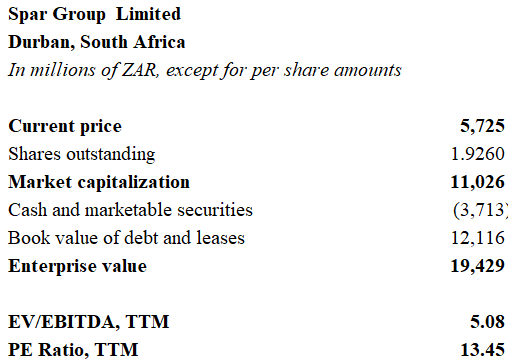

Where are the dogs with the least fleas? Well, I found a few in the South African consumer sector. One standout is Spar Group Limited, South Africa’s second leading grocer. Spar generated over $8.1 billion in sales from continuing operations during the last fiscal year ended September of 2025. Having shed its unprofitable operations in Poland, Switzerland and the UK, Spar Group has narrowed its focus to its to core markets: Southern Africa and Ireland. The company also operates a joint venture in Sri Lanka. Debt has been reduced by $250 million following the divestitures. Spar’s market capitalization of $700 million represents a 14% discount to my estimate of the company’s intrinsic value.

Spar is better understood as a wholesaler. It doesn’t actually own and operate its retail stores. Instead, each retail operator brands its location with the Spar livery and agrees to purchase its inventory from Spar. Store operators also agree to pay marketing and inventory management fees to Spar, akin to a franchise model. Spar Group is affiliated with Spar International which is based in Amsterdam, where it began business in the early 1960’s. Spar International awards country licenses to various wholesalers around the world, and Spar Group holds the licenses for Southern Africa, Ireland, and Sri Lanka. While some products on sale in a Spar are locally sourced, much of the inventory consists of “Spar” private label products.

Spar Group is headquartered in Durban, South Africa where it recently moved after selling off its offices in nearby Pinetown. Spar is the second largest food retailer in South Africa. Spar stores generally fall into two categories: large-format grocery stores, and smaller convenience stores. Spar also offers a collection of DIY of home improvement retail destinations. There are 2,523 outlets in Southern Africa serviced by 9 distribution centers. Gross retail margins during the last fiscal year were 10.8%, and operating margins amounted to 2.1%. The Ireland market is stronger with a 3.1% operating margin. Unfortunately, Ireland accounts for only 20% of group sales. The Irish market hosts 1,161 stores serviced by 25 distribution centers.

Shares of Spar could be purchased last week on the Johannesburg bourse for 57.25 rand, or about $3.50 per share. The chart is abysmal – down nearly 70% since the Covid peak. The price represents a multiple of 5 times EBITDA and about 13.5 times FY 2025 earnings.

To calculate the intrinsic value of the business, I used the earnings power value (EPV) method favored by Bruce Greenwald and his value investment acolytes. This method takes unlevered free cash flow and divdes it by a weighted average cost of capital to arrive at a gross value of the business. Adjustments are made for cash and debt on the balance sheet to arrive at a net value, or “intrinsic value”.

My calculation uses 13% as a weighted average cost of capital. Spar’s 50% debt load, including leases, carries an approximate cost of 9.8%, or 7.15% adjusted for tax deductibility. Equity, the other 50%, bears a cost of 19%. This factor takes the sum of the equity risk premium of about 10.6% on top of the country’s 10-year note yield of 8.5%. I probably could have reduced the rate to account for the 20% of sales from Ireland, but I didn’t bother. 13% seems like a reasonable discount rate.

At 13%, unlevered free cash flow of 2.7 billion rand capitalizes to 21 billion rand. Deducting net debt results in a valuation of 12.6 billion rand, or 65.30 rand per share, or roughly 14% above its recent closing price. I prefer investment candidates with a 30% margin of safety, so Spar doesn’t pass muster.

I also compared Spar with its grocery peers. The gallery included the Canadian grocer Metro, the UK’s Tesco, Kroger, and Spar’s leading competitor Shoprite. Numbers were adjusted to US dollar terms in the accompanying chart. Metro is the most profitable of the group, while Kroger and Tesco show operating margins of 3 and 4 percent, respectively. Spar trails the sector.

Spar’s gross revenue margin exceeds 12.2% when you include revenue from operator contracts. The operating margin last year was the meager 2% mentioned above. Returns on equity are lackluster at just slightly above 10%. Meanwhile, Shoprite trades with an 8.5 EBITDA multiple and posted a 27% return on equity last year. Spar needs to aim for this target if it hopes to improve shareholder value.

Despite the divestments and improved balance sheet, Spar continues to face challenges. Rising gold and mineral prices have boosted the South African economy, but GDP growth is mired in the low single digits. An inventory management software upgrade has been a fiasco. Early in 2026, CEO Angelo Swartz resigned after three years in the role and 19 years with the company. CFO Reeza Isaacs has stepped into the vacancy. Spar will post first half FY 2026 trading results on June 10, and I expect the numbers will be underwhelming.

Although my calculations indicate that Spar is trading below intrinsic value, the stock is a pass for me. Yes, they can fix the software problems and improve management, but that won’t change the fundamental problem that Chris Hohn so clearly identifies: Spar has no ability to meaningfully lift prices. It is a price-taker, not a price-setter.

A bigger hurdle is the risk that independent operators become disenchanted with the Spar model and abandon the mother ship. Revenue from customer contracts amounted to 2.1 billion rand in FY 2026, or nearly 80% of operating income. Cyncially, one could argue that Spar makes virtually no money at all on the wholesaling business and is completely dependent upon the loyalty payments from independent operators to eke out its modest profits.

Store count is barely growing in Ireland and static or falling in South Africa. Recently, WalMart announced that it would enter the South Africa market. Although the Bentonville behemoth has had its own share of foreign misadventures, many independent operators won’t be able to withstand the siege. We haven’t even mentioned Amazon.

Grocery is a tough business in the best of times. Buffett lost $400 million in Tesco during 2014. Even if I could buy shares of Kroger or Metro at meaningful discounts, I still wouldn’t do it.

Like a good Bloodhound, the search continues. Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2026-05-26 08:54:232026-05-26 08:54:24Best in show

A Substack went viral the other day talking about how a minority of published posts on the platform generate the majority of views. When no part of earth shattered at this revelation, the author pressed the argument by citing something called Price’s Law. Since it had an equation with a square root in it, the whole concept seemed pretty legit.

To my eyes, it looked like a more sophisticated version of Pareto’s 80-20 observation. Regardless of which polymath you prefer, it drew the same conclusion – a few of your most successful ideas generate most of your income. The piece seemed to argue in favor of “flooding the zone” with material, since it couldn’t be known with any confidence what was going to catch fire. At least not until one applied rigorous scientific observation once sufficient data had been assembled. This reminded me of Ken Griffin’s remarks about needing to be right only slightly more than 50% of the time. Or was that Roger Federer?

Of course, this all assumes that any of us are capable of heroic levels of output. There are only so many Danielle Steels in the world. Nor do most of us have a team of geniuses generating such creations on our behalf. I can only hope I will live long enough to see the day when Silicon Valley invents a computerized program that can simulate human intelligence. Until then, it’s just me.

I suppose the counterargument would come from Grandpa B about only having 20 punch cards in your life, or something to that effect. There’s also his admonition to avoid the institutional imperative that comes to mind. Producing more content because everyone else is producing more content is how you end up with slop. Does Irenic really need to start an activist campaign to revitalize Snap? It’s also how you end up with the military-industrial complex that Eisenhower warned us about. But that’s a different newsletter.

All of this is a long way of saying: 1. It’s been awhile since I wrote anything. 2. That doesn’t mean I haven’t had any ideas lately. It just means I haven’t had the time to “craft” anything worthy of production. 3. Should that even matter? Perfection is not my goal. This is simply a forum for me to think out loud. And if a few people read it and give me constructive feedback, well then, I’m learning. If someone makes some money out of these observations, then that’s good too. 4. Perfection is not much fun anyway. We’re not writing the last page of Farewell to Arms for 47 iterations to find the answer. I have really enjoyed Eden Bradfield’s writing. There’s a grammar error here and there, but it’s real stuff. The rough edges are part of the charm.

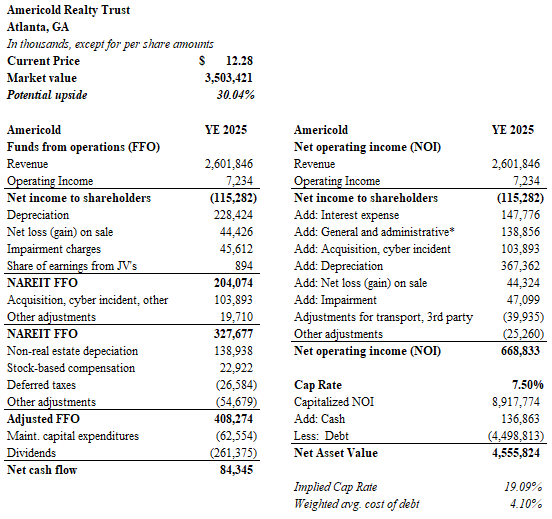

So, enough of the beard-stroking. Here are a couple of REITs I’ve been thinking about. The first one is BRT Apartments Corp. $BRT, and the second is Americold Realty Trust $COLD. I’ve taken a sizable position in BRT but remain on the sidelines for COLD. Yes, the sentiment for refrigerated warehouse space is especially bearish. The Wall Street Journal recently talked about the oversupply in the sector and the concomitant consumer spending slowdown.

I know a little about refrigerated warehouses from experiences early in my career and I can tell you a couple things. One, you are running a service business where tenants have high inventory turns. It’s more like a hotel than a warehouse. Two, it’s a hell of a lot more seasonal than you might think. It seems totally obvious, but most turkey gets consumed in November and December. Most of those birds are sold frozen. No matter how good your logistics are, it’s just not possible to kill millions of turkeys in October, freeze them, and then ship them in November. No, it’s a cyclical inventory build over several months. Kind of like Mattel placing orders for Barbie in July. It takes time to amass a lot of turkeys. And then whoosh. Out they fly, er, out they ship. I’m sure most of the high-end steak business has a similar cycle.

The point here is that you may think you can just evaluate a refrigerated warehouse portfolio as real estate, but you really need to factor in lot of management. Probably much more than you’d have in a net-lease industrial realty business. Let’s take Prologis, the biggest industrial landlord. In 2025, Prologis had general and administrative expenses of $469 million on $8.8 billion of revenue, or just about 5.34%. In contrast, Americold has $269 million of G & A expenses on $2.6 billion revenue. That’s almost double.

Why is this important?

Well, a lot of people use the exercise of applying a capitalization rate on net operating income (NOI) to arrive at value the underlying assets. NOI is a real estate cousin to EBITDA, and most REITs publish this number for us real estate hillbillies followers to consider. When they compute NOI, they add back general and administrative expenses. The theory here is that a buyer of the individual properties wouldn’t be burdened by the parent company’s management costs.

The casual observer might take the NOI for Americold at the end of 2025 and make the assumption that the assets are worth $13.3 billion. COLD published NOI of $800 million at the end of 2025, so $13.3 billion is what you get with a 6% cap rate. Let’s use 6%, since that’s about 200 basis points above the company’s current debt cost. Subtract debt of $4.5 billion and the net asset value could be $9 billion. The market cap for Americold is only $3.5 billion. Before you run to your Robinhood account, take a breath. Unfortunately, these assumptions are far too aggressive. Adding back $269 million of general and administrative expenses is not realistic. These are businesses as much as they are buildings, and sweeping aside a layer of management is simply not possible.

I decided to value the real estate using a 7.5% cap rate. Investors in institutional quality real estate would probably argue in favor of a lower rate, but I figure the current cost to borrow money is more like 5.5% and I’d still want to earn 200 basis points over that number. It’s also a soft market. As a general practice, I don’t think you should underwrite deals by penalizing them with the bigger cap rate. Rather, you should make the adjustments in your future rent assumptions. You may want to assume that revenues will fall by 10% for refrigerated warehouses given the oversupplied market conditions. Such a rent reduction would knock $260 million off the top line, and eviscerate $3.5 billion of value. Maybe the market knows this, and that’s why the chart for COLD looks worse than the Thwaites Glacier.

I don’t have time for a rent sensitivity analysis, nor do I know the market that well, so I will just use 7.5% as my cap rate in this exercise. Hypocrisy be damned.

Instead of adding back $269 million dollars of general administrative expenses, I added back $139 million. This number represents 5.34% of revenues, just like at Prologis. In other words, I’m saying $130 million of general and administrative expenses are an integral part of Americold’s business and can’t be removed for purposes of valuing the real estate. The resulting NOI is $669 million. Let’s capitalize that number at my 7.5% to arrive at an asset value of $8.9 billion. Less debt, the net asset value for Americold calculates to $4.5 billion. This is approximately 30% above COLD’s market capitalization. The market offers a decent discount, and it explains why Ancora Holdings has agitated for changes, including asset sales.

The 7% dividend yield is attractive and seems reasonably well covered if you believe management’s figures that maintenance capital expenditures amount to $62.5 million per year. This strikes me as a little on the low side, but I am just asking the question. I don’t have comparable data. I will say that refrigerated warehouses are filled with complicated cooling systems that require a lot of maintenance. Underestimate that number at your peril.

My verdict here is that a Americold presents a good value. The dividend seems like a solid way to earn some beefy yields while Ancora puts the company’s assets through their paces. Leverage is about 50% of my estimated value, so that’s a little high. One could envision a dividend cut if funds need to be marshalled for principal reductions. Fortunately, the company’s debt maturity timeline is long. The oversupply in the market will eventually be absorbed. I set Americold on the back burner for now, but I will likely revisit the business soon.

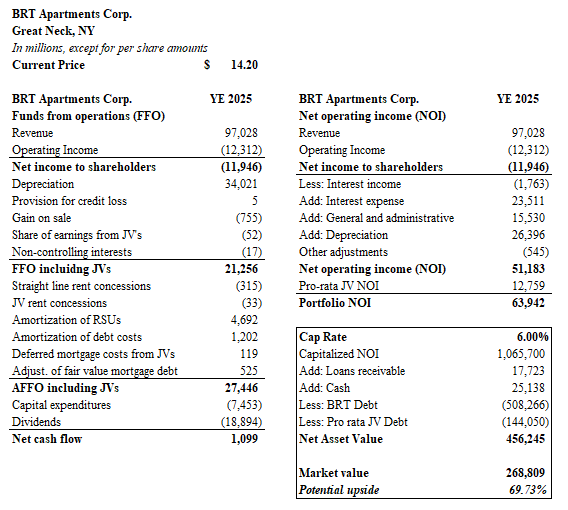

I have much more confidence in BRT Apartments Corp. The company is based in New York and owns about 5,400 units throughout the southeast. Many properties are held through joint ventures. The company is controlled by the Gould family. I have read various estimates about the amount of insider ownership at BRT, and it seems like it is nearly 95% when I toted up the 13-Fs. So, there’s not much float. No activists are going to come along and move the needle. The Goulds probably aren’t in a hurry to make any aggressive changes. The company’s dividend reinvestment program works in their favor. There’s no identifiable catalyst, in value investor parlance.

Despite these caveats, BRT is an exceptionally cheap stock. I owe a hat-tip to an Omaha fund manager. I would name him but I won’t, since I suspect he would like to add to his own position under the radar. The thin trading volume has meant that recent purchases have already pushed the share price above $14. It was $13.50 when I made my initial buys. The current market capitalization is $269 million, but I think the net asset value exceeds $456 million. BRT pays a 7% dividend yield – far higher than Avalon Bay $AVB and Mid-America $MAA. The assets are solid B+/A- apartment communities in dynamic metro areas. Yes, some of those markets have been fairly soft and the share discount may reflect some concerns about looming vacancy issues. The portfolio is also 60% leveraged, so there’s a riskier element to the business than some of the bigger multifamily REITs.

I’m not going to write a lot more here since I’ve already overstayed my welcome, but I will say that it is very hard to justify digging a hole for a new apartment complex right now when an investment like BRT is available as a public entity. One would be hard-pressed to generate a 7% cash-on-cash return today on most new developments using an equivalent percentage of leverage. With tons of money still out there chasing deals, the yield on most acquisitions would be even lower. BRT is certainly very attractive when compared to private market alternatives.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

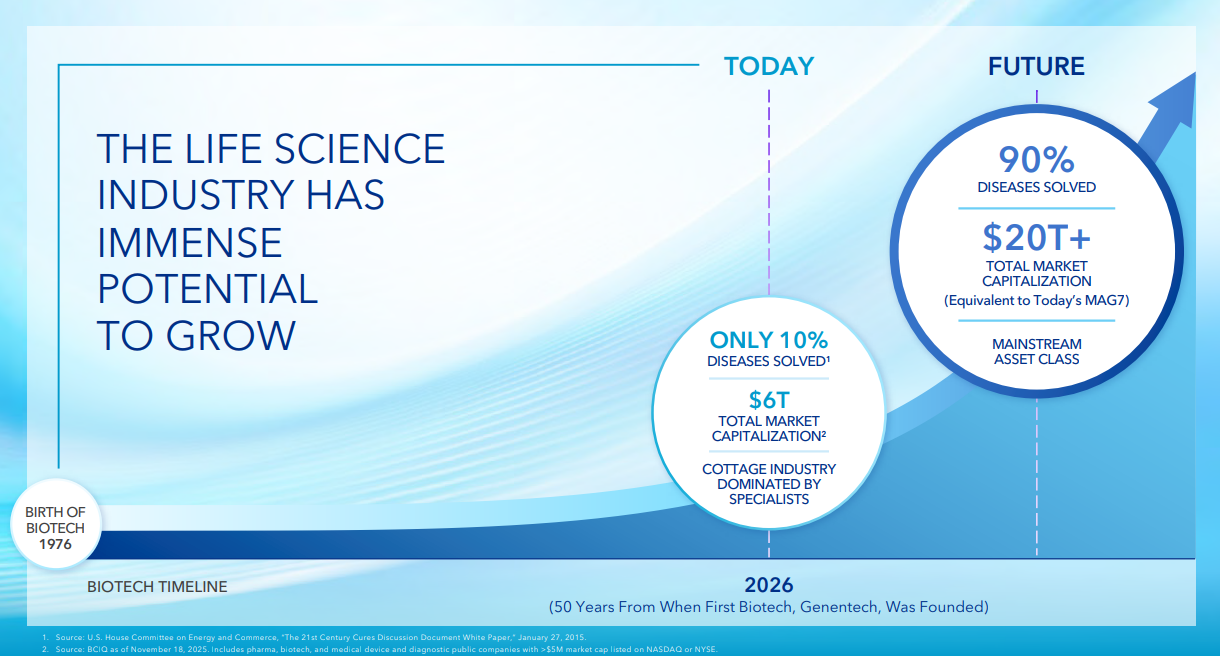

I don’t know if they hand out awards for the most optimistic investor relations team, but the gang at Alexandria Real Estate Equities just opened 2026 with a banger that will surely make them the top candidate. Yes, it’s been a rough three years for the nation’s largest owner of buildings dedicated to the pharmaceutical and biotechnology industries. The share price has fallen by 75% since the pandemic and they just slashed the dividend. But despair not ye of little faith. Just think about all of those diseases out there looking for a cure!

The Alexandria slide deck announces our glorious pharmaceutical future by declaring that only 10% of earthly diseases have been “solved”. That leaves 90% of the rest of the diseases left to cure. Talk about upside! The current market capitalization of the biotechnology industry is estimated by Alexandria to be $6 trillion. Extrapolating this figure for the next 80%, well, that’s another $14 trillion of potential market capitalization lying just beyond the rainbow. The god-like powers of capitalism will save humanity.

Alexandria’s team must have considered the irony of this future. After all, once 100% of the remaining diseases are “solved”, the market capitalization of the biotech industry should be closer to zero than $20 trillion. Realizing the potentially adverse effect of curing all diseases, they left open the possibility that 10% of the remaining diseases are beyond the grasp of even the most miraculous biotechnical engineering.

Because, when you get right down to it, solving all diseases isn’t great for business. No, what we really need is a sort of Munchausen-by-proxy economy. By all means, come up with ways to treat the ills of mankind which improve comfort and extend lifetimes. But cure? Now, hold on there, that’s a lot of jobs we’re talking about. Healthcare is now more than 16% of our nation’s GDP. You know what might work even better? What if we re-introduced diseases that were already “solved”? Take measles, for instance. Who knows? A resurgence of leprosy might be just what we need to avoid the next recession.

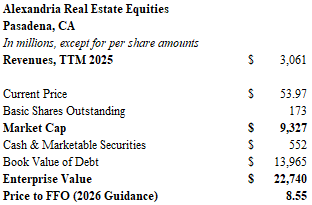

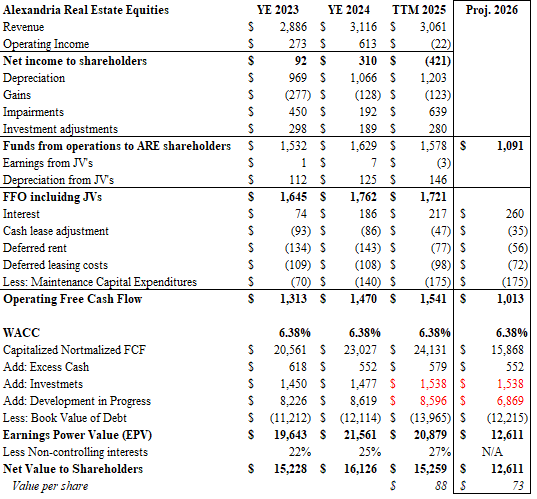

Ok, enough joking around. In fairness to Alexandria, much of the presentation describes the precarious state of the life sciences real estate market and the challenges facing the company. The real question before the house is whether shares in Alexandria Real Estate Equities (ARE) offer investors compelling value. The nation’s largest owner of real estate dedicated to scientific research claims that the net value of its assets is far higher than the current $54 share price. Alexandria’s investor presentation asserts that the true value is closer to $94. In my estimation, the shares are worth about $73. However, I won’t be buying stock any time soon. Much of this premium is based upon the book value of an uncertain development pipleine and the value of its speculative securities investment portfolio.

In this article, we’ll take a brief overview of the latest investor presentation, and I will guide you through some numbers that compose my valuation.

Alexandria has shaped its nationwide real estate portfolio into 26 dynamic innovation campuses. Primary markets include Boston, San Diego, San Francisco, Seattle, and DC. The company boasts a tenant roster of 700 companies in 27.1 million rentable square feet. Tenant retention has been over 80% over the past five years. Scientific innovation thrives when disparate groups of creative thinkers interact on a frequent basis. Despite the rise of remote work, it seems likely that medical technology will continue to emerge from the laboratories and offices of pharmaceutical companies, research universities, and medical device manufacturers.

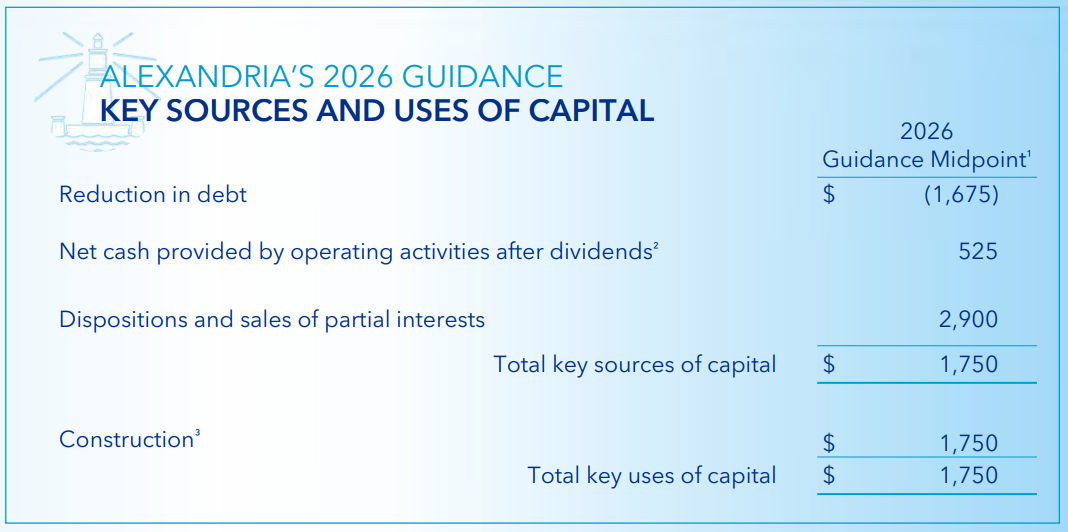

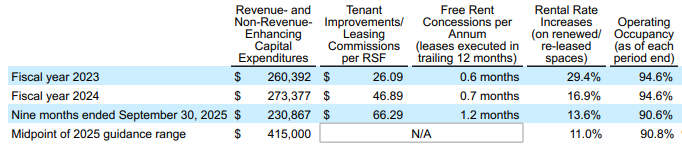

Alexandria trades with a market capitalization of $9.3 billion and the current price allows for a 5.3% dividend yield on the reduced payout. The share price is roughly 8.6 times management’s guide for 2026 funds from operations (FFO). The undepreciated book value of real estate on its ledger amounts to $29.3 billion, with another $8.6 billion of construction in progress at the end of the 3rd quarter of 2025. The company has approximately $13.9 billion of debt and lease obligations. To improve the balance sheet, Alexandria intends to dispose $2.9 billion of “non-core” real estate assets and joint venture interests in 2026. ARE forecasts 2026 operating cash flow (after dividends) of $525 million. The resulting $3.4 billion cash pile will be split: $1.7 billion for debt reduction and $1.7 billion for the completion of construction projects.

Alexandria is rated BBB+ by Standard and Poor’s but has been placed on a negative credit watch. Still, the company does benefit from a low cost of financing and a long runway for debt maturities. The weighted average interest rate for ARE’s debt is 3.97% and the weighted average maturity is 11.7 years. Unfortunately, recently issued debt came with a 5.6% coupon.

The reasons for worrying about Alexandria’s future are easy to find. Winter has arrived for the medical technology industry. Demand for life science space has fallen 60% since the pandemic. To make matters worse, the most recent Senate budget presents a 40% decline in spending for the National Institutes of Health (NIH) to $48.7 billion. It is estimated that 1,500 jobs will be eliminated. Meanwhile, only about $9 billion of venture capital funding is anticipated for the medical technology industry in 2026. This represents a substantial reduction from 2021 when $41 billion was raised. Pharmaceutical company spending on research and development peaked in 2023 at $317 billion and has fallen the past two years.

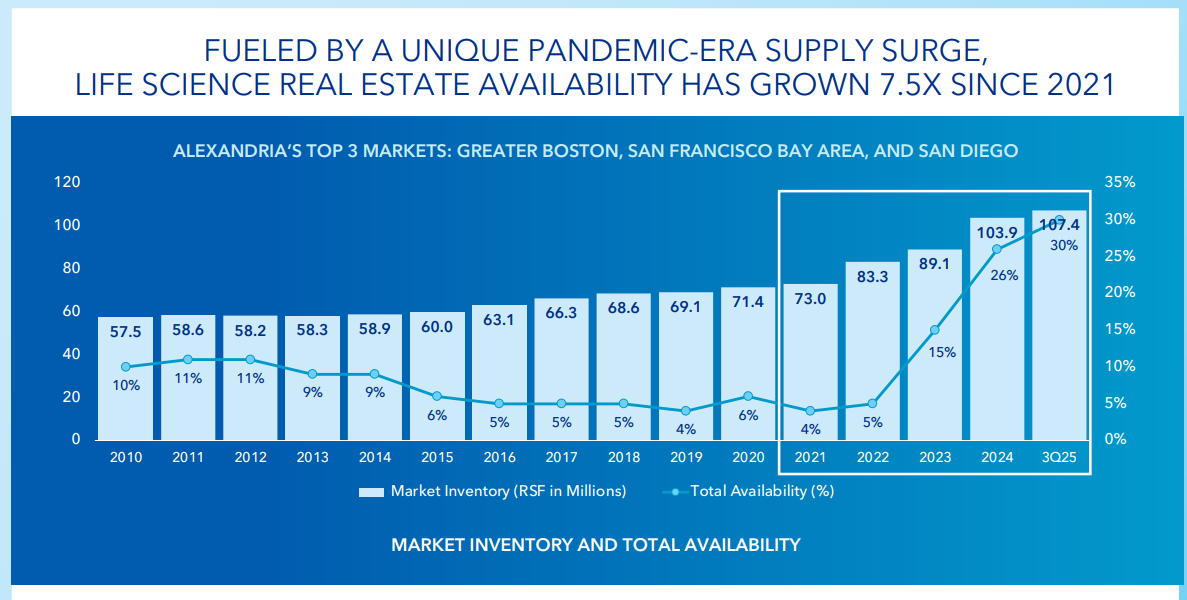

Market occupancy levels have dropped precipitously. Over 30% of space is available in the company’s top three markets of Greater Boston, the San Francisco Bay Area, and San Diego. Occupancy levels at Alexandria’s buildings reflect the industry decline. They fell dramatically from 94.6% at the end of 2024 to 90.6% at the end of the 3rd quarter of 2025. Any time real estate owners see an occupancy level with an 8 in front of it, beads of sweat start to appear. Occupancy at Alexandria is forecast to drop to as low as 87.7% by the end of 2026.

More problems could lie ahead. Alexandria has a plan for 2026, but what about the completion of projects in 2027 and 2028? Future capital raises to finish buildings in progress may be needed, and they will certainly dilute current shareholders. At the end of the 3rd quarter of 2025, Alexandria projected that 4.2 million rentable square feet will be placed into service between the end of 2025 and 2028. 43% of the new space is under lease or in negotiation. This new space is expected to generate more than $390 million of NOI. But that assumes another 2 million square feet has yet to be absorbed in what promises to be a soft market. It could take many years to backfill the overall 30% market availability in Cambridge, Massachusetts.

Finally, the entire cost structure of newer assets may face a pricing reset. Capital improvements amounted to $260 million in 2023, but they were expected to rise to $415 million by the end of last year. On a per square foot basis, TI’s and commissions rose from $26 to $66 over three years. Free rent to secure new leases has doubled during the timeframe. Even the strongest pharmaceutical companies will balk at the rental rates on offer and demand substantial concessions.

Alexandria forecasts that 2026 FFO will fall from approximately $9 per share in 2025 to $6.40 per share in 2026. While dispositions account for a large portion of the reduction, rents on lease renewals are forecast to fall by as much as 12%. Same-store net operating income will drop by as much as 9% in 2026.

Valuation

My valuation method is very simple. I took $1.1 billion of projected funds from operations for 2026, added back the forecast interest expense of $260 million, subtracted $175 million for maintenance capital expenditures, and subtracted cash lease adjustments. The cash lease adjustments are identical to the numbers for 2025, but they have been reduced by 27% to estimate the portion attributable to joint ventures. The resulting free cash flow from operations for 2026 is estimated to be approximately $1 billion. This sum was divided by a capitalization rate of 6.38% to arrive at $15.9 billion of value.

Next, I added $552 million of cash on hand, the securities investment portfolio of $1.5 billion and the book value of construction in progress of $6.9 billion. Construction in progress was calculated by subtracting $1.75 billion from the September 2025 balance of $8.6 billion. Finally, after accounting for management’s guidance of $1.75 billion of debt reduction, the 2026 debt level of $12.2 billion was subtracted. The net value is $12.6 billion, or approximately $73 per share.

The table shows the change in computed net asset value over the past three years. In 2023 through 2025, I “grossed up” funds from operations to include joint venture partnerships before capitalizing the cash flow. An adjustment was made at the bottom using a percentage of book value attributable to noncontrolling interests. My calculation for 2025 indicates a net asset value of $88 per share, showing that a substantial decline in the stock was justified.

My capitalization rate is based on a weighted cost of capital where the market value of net debt accounts for 56% of the measure. At a BBB+ rating, the cost of debt was attributed as 5.1%. This is a forgiving number considering the recent placements at higher rates. Equity, the remaining 44% of the weight, was awarded a simple 8% rate. I don’t have a sophisticated explanation for the use of 8%, but it generally “feels right”.

You may think my cap rate is too high considering the gold-plated roster of tenants like Lilly and Merck and the proximity to the best universities in the world. Alexandria touts its asset values utilizing capitalization around 6% and below. Yet, the company has sold assets at cap rates above 8.5%. The building sales may may not represent “core assets,” but such a wide discrepancy can’t persist as long as interest rates remain elevated.

Although the calculation offers the appearance of upside, far too much weight is placed on the book value of construction in progress and the value of the company’s securities. Alexandria often took equity stakes in their tenants in lieu of rent. Given the uncertainty around new drug approvals, much of the securities portfolio could become impaired. Meanwhile the full lease absorption of $6.8 billion of construction in progress is far from certain. In the early years following completion, hefty concessions will be required to attract tenants. One can easily see that a 30% impairment of the development pipeline would eliminate the premium calculated in my valuation. The market may well be ascribing such a discount already.

Alexandria Real Estate Equities offers an intriguing way to invest in the future of the pharmaceutical industry. Medical innovations will continue to emerge, of course, and they may occur more frequently than not at one of Alexandria’s campuses. The company has a best-in-class real estate portfolio and has proven to be a skilled operator and attractor of premier tenants. But nobody is immune to the laws of supply and demand. There is simply too much laboratory space on the market, and the engines of demand are looking fairly dormant. When the government is no longer a key partner in the development of new drugs, your runway looks a lot cloudier. Is there upside? Probably so. But, I think there are better places to put your money in the meantime.

If you are attracted to Alexandria’s robust dividend yield, I would look elsewhere. Some of the pipeline master limited partnerships (MLPs) are more appealing. Western Midstream (WES) and Hess Midstream (HESM) yield about 9%, and the demand for natural gas seems much more reliable as power generation capacity continues to grow. Along those same lines, some of the big miners stand to benefit from the copper and minerals boom. BHP yields 3.5%, Rio Tinto is on 4.6%, and the much riskier Vale yields more than 8%. I would add that the large mining companies provide the added benefit of diversifying away from a deflating dollar.

We’ll leave it there for now. Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

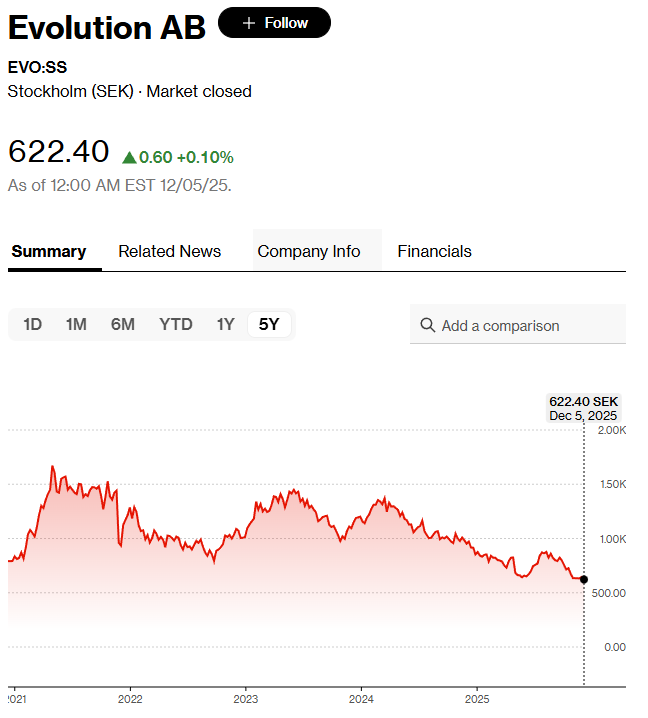

Evolution AB is a Swedish gaming company that trades on the Stockholm bourse. About 622 krona will buy you a share, and that price gives Evolution a market capitalization of about €11.6 billion. Evolution develops and operates games that “sit behind” many well-known gambling sites. They continually find new dopamine-enhancing ways to keep punters glued to their devices, losing money to the house in rapid-fire succession. Most games seem to target the unsophisticated bettor. “Coin Flip”, “Cash Hunt” and “Crazy Time” are just a few of the offerings. More interestingly, they also offer traditional casino games like poker and roulette by hosting players online with live studios situated around the world.

I passed on Evolution earlier this year, but I decided to take another look at after reading a recent Bloomberg article about the investment activities of Kenneth Dart who is taking large positions in the gambling industry through Evolution and Flutter. Flutter owns FanDuel, Paddy Power Betfair, SportsBet, and Poker Stars. Or, if you prefer, just about half of the kit sponsors for English football. In a clear indication of modern society’s moral compunctions, England has banned alcohol sponsors on their team jerseys for well over a decade, but they have no problem with gambling companies emblazoned across players’ chests.

Kenneth Dart is the billionaire heir to the plastic container fortune. When he’s not crafting ways to avoid paying taxes, he is busy investing in “sin stocks”. He had a phenomenal run of success with tobacco firms recently. The thesis seems to be similar for his investments in online gambling: it’s widespread, increasingly legal, and totally addictive.

Evolution trades with a trailing PE slightly above 10, and an EV/EBITDA multiple of 7.4x. After a brief summer rally, shares hover near 52-week lows. Evolution is 62% below its all-time Covid high, and down 26% since the beginning of 2025. Notably, Dart’s largest investment in the company occurred before the most recent drawdown.

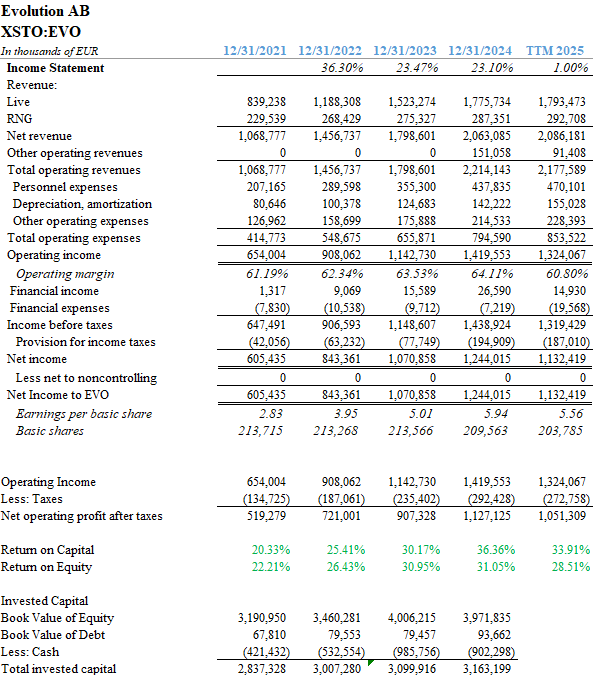

Revenues at Evolution grew at a compound rate of over 25% annually between 2021 and 2024. Unfortunately, the combination of high growth and diverse worldwide internet hosting services attracted the sort of nefarious folks who’ve always lurked in the gambling shadows. Hackers in Asia inflicted widespread outages and security breaches upon Evolution last year. Revenue has plateaued over the past 12 months. The stock price reflects the lost momentum.

Evolution’s leaders assure shareholders that the security problems have been solved and the company is ready to grow once again. I have found CEO Martin Carlesund’s messages to shareholders to be refreshingly blunt in their assessment of the company’s shortcomings. Accountability seems to be part of the vernacular at Evolution. It is a sharp contrast with another downtrodden company I have been researching: DentsplySirona (XRAY).

One might think that straight talk would be needed at a company which has lost 83% of its market capitalization, but that is not the case! DentsplySirona is not only a really horrible name (did they leave out letters to remind us of missing teeth?), the annual report is a load of jargon-filled blather that leaves one wondering if the company is a dental supply company or a multi-level marketing scheme. It certainly makes no apologies for an atrocious capital allocation track record and probably isn’t worth my time putting pen to paper. But we’ll talk about that later. Moving on.

Evolution is asset-light, has an operating margin of 60%, and posts returns on capital in excess of 30%. The company pays a well-covered dividend, and the yield is nearly 5%. If they can right the ship and return to growth, the upside is compelling.

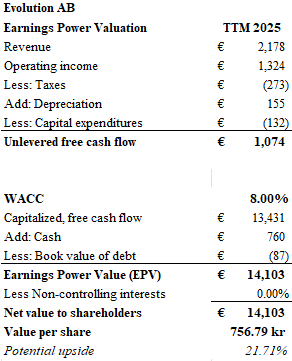

My preferred valuation model is the basic Earnings Power Value (EPV) method advocated by Bruce Greenwald and his peers at Columbia. In the tradition of Ben Graham, normalized unlevered free cash flow is simply capitalized by the weighted average cost of capital (WACC) to arrive at a value for the firm. Subsequently, net debt is subtracted to arrive at a value of the equity. In the case of Evolution, unlevered free cash flow over the trailing twelve-month period was just slightly less than €1.1 billion. Using a WACC of 8% to capitalize this amount results in a value of €14.1 billion once one accounts for the net cash position on the balance sheet. On this basis, Evolution trades at a 22% discount to its market price.

As always, I struggle with the proper cost of equity to employ in my valuation. I don’t use betas and assigning a cost to the equity is easier if you can assume a spread above the firm’s cost of debt. Since Evolution is unlevered, the 8% rate has a swaggy feel to it. Should it be lower? This is not a European company. Revenues are international, so pricing off the 10-year Bund doesn’t work. Arguably any company that is vulnerable to hacking and relies on programming talent anywhere from Tbilisi to Taipei should be valued accordingly. Using a WACC of 10% puts the value closer to par.

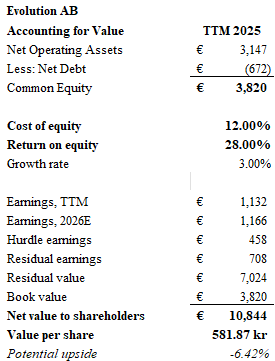

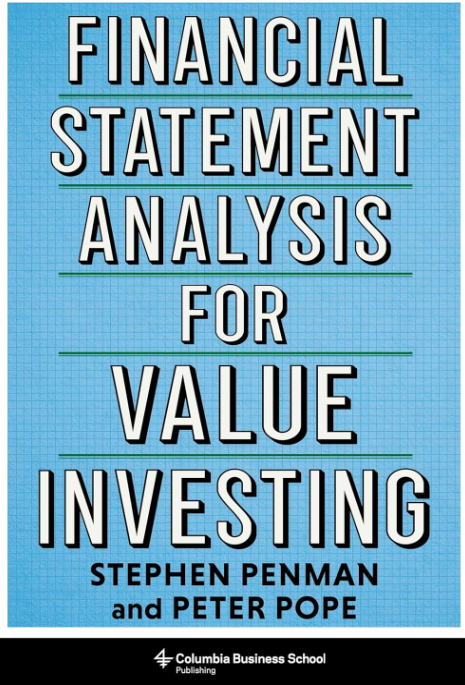

The other valuation model I’ve been using lately is the “accounting for value” method from the bookFinancial Statement Analysis for Value Investing. Stephen Penman and Peter Pope are CPAs by training and they take book value as the foundation. Next, they add the value of future growth. The authors rightly state that a company’s future growth is only valuable to the extent that the return on equity exceeds the cost of equity. They take this “surplus” return and discount it at the cost of equity less the assumed rate of growth. The higher the growth, the lower the denominator, the larger the value of future earnings. The model can be especially useful if one works backward: it tells you what level of growth is necessary to justify the current price.

If one assumes a cost of equity of 12% for Evolution, and a return on equity of 28% consistent with recent performance, the future “surplus” earnings calculate to €708 million assuming a growth rate of 3%. This results in a value 581 krona per share, once again, roughly in line with the current price.

But what happens if growth resumes at a rate higher than 3%? A 5% future growth rate results in a share value of $705 krona, or 13.4% upside. A 6% growth rate translates into $798 krona, or 28% upside.

Is the market for online gambling going to grow faster than worldwide GDP over the coming decade? It seems plausible. There is an insatiable willingness to gamble on literally everything, and the ubiquitous access to gaming through a phone makes it easily accessible. Might there be a backlash? Names like “Coin Flip” and “Cash Grab” imply a simplicity that can be very appealing to children, so it wouldn’t be surprising if there is a worldwide recognition that the proliferation of gaming is leading to problems with youth delinquency. But sadly, I think that regulatory horse has left the barn.

Evolution has created a lot of valuable intellectual property, its games are entrenched in the gambling site ecosystem, and the investment in live studios provides punters with the authentic feel of a casino. The lack of debt, high dividend yield and substantial margins seem to present downside protection. I believe the returns on equity are significant enough that the firm can reinvest its ample cashflow into growth that will exceed 5% over the next decade, so I consider the shares of Evolution to be priced 10-25% below the intrinsic value of the business. Fortis fortuna adiuvat.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

Unlike most Hollywood scripts, media deals rarely live happily ever after. Disney is still healing from the acquisition of 20th Century Fox for $71 billion in 2019, which drew the ire of activist investor Nelson Peltz. The AOL-Time Warner merger of 2000 proved to be a fiasco. Even now, the heavy debt load carried by Warner Brothers Discovery is part of that legacy.

It came as quite a surprise to see Warner Brothers shares surge more than 33% last week as news spread of a pending bid from David Ellison’s Paramount Skydance. It has only been five weeks since the son of Larry Ellison muscled his way into ownership of Paramount for $8 billion. A deal for Warner Brothers would be larger by several orders of magnitude – in excess of $71 billion, including WBD’s onerous $35 billion of debt.

Contrast the swashbuckling exploits of Ellison with Brian Roberts, the second generation CEO of Comcast. Roberts transformed the cable company into a modern media giant by launching attacks during moments of industry distress. Comcast acquired AT&T’s broadband business in 2002 in the wake of the dot-com bubble, and preyed upon the ailing General Electric to buy NBC Universal in 2011.

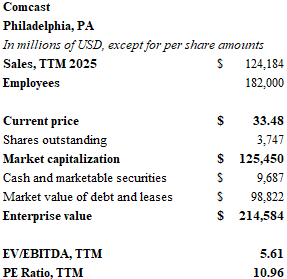

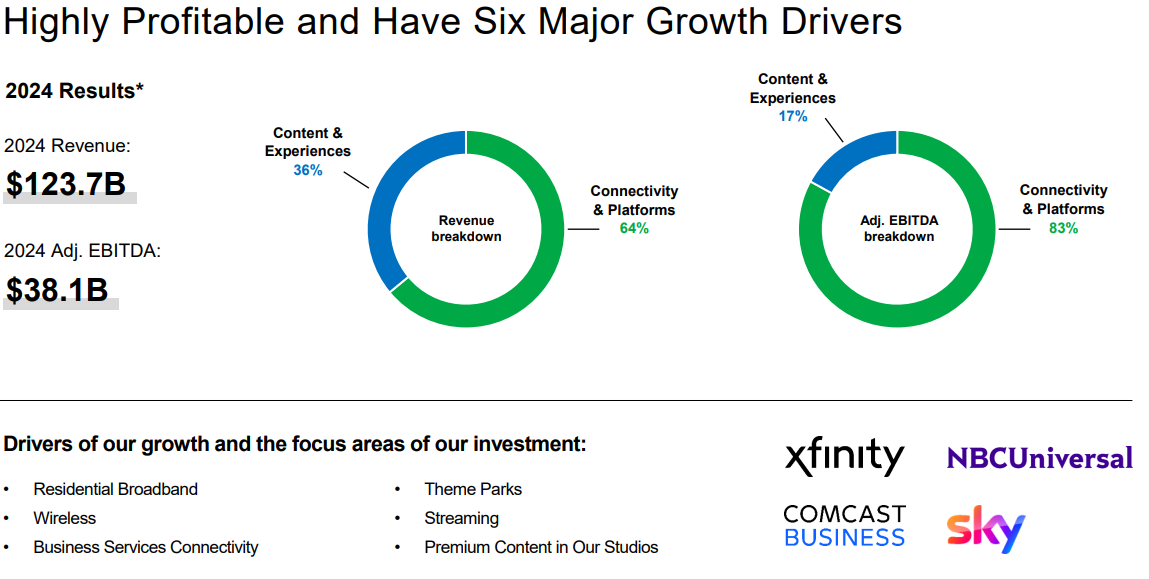

Comcast (CMCSA) stock presents an appealing investment opportunity. The share price has declined 46% since it peaked during the pandemic lockdown. Although the company faces growing competition from new fiber networks and fixed wireless providers, Comcast continues to increase revenues. In my estimation, Comcast trades at a 44% discount to the intrinsic value of its business.

Comcast, America’s largest broadband provider, generated over $124 billion in revenue over the past 12 months. The Philadelphia titan produced $12.5 billion in free cash flow in 2024.

The following article offers a brief discussion of Comcast followed by a simple valuation presentation. I employ the earnings power value model (EPV) favored by Columbia’s Bruce Greenwald in the tradition of Graham and Dodd.

Comcast shares currently trade with a PE ratio of 11 and an attractive EV/EBITDA multiple of 5.6. The free cash flow yield exceeds 10%. While the equity price languished, over $13.5 billion of cash was returned to shareholders in 2024: $4.8 billion in dividends were awarded, and $8.6 billion of stock was repurchased. The current dividend yield is nearly 4%.

Comcast recently announced that it will spin-off some lower-tier networks to shareholders later this year. The new company will be known as Versant and will hold legacy networks such as CNBC, E!, USA and the Golf Channel. Various digital assets like Rotten Tomatoes will also be included. Notably, NBC and the Peacock streaming service will remain with Comcast.

So why have Comcast shares performed so badly since 2021? Despite increasing revenues per user and a successful rollout of Xfinity mobile, Comcast has been losing customers in its legacy broadband and cable businesses. Although new lines of revenue are emerging, the content side of the business is much smaller. Unfortunately, it is also less profitable.

“Connectivity and platforms” accounted for 64% of Comcast’s $123.7 billion of 2024 revenue. These fixed-cost broadband and cable services offer tremendous operating leverage. EBITDA margins are 40%. Meanwhile the studio, network and theme park businesses have EBITDA margins of 20%. Reinvesting the cash from legacy broadband into media content is a fruitful exercise, but it can’t replicate near-monopoly profits the company once enjoyed.

Blockbuster movie releases like Jurassic World and Oppenheimer produce hundreds of millions in profits, not billions. New theme parks in Beijing and Japan are hitting their stride, but European expansion plans won’t move the needle much. The Peacock streaming service has yet to turn a profit, and Comcast recently bolstered the content of the streamer with an expensive NBA deal – a league suffering from declining viewership.

One can’t deny that a Paramount-Warner merger would represent a threat to Comcast. The venture could drive higher prices for content carried by Xfinity’s cable network, and a combination of two of the largest film studios might harness more resources into production. Ellison has already lured Jeff Shell, CEO of NBC Universal to Paramount.

The Roberts family controls Comcast through a solid lock on the company’s B shares. The lack of voting power in the A shares may be a further cause for a market discount.

Substantial growth will likely come from another transformative acquisition by Brian Roberts. The question is whether or not a bargain can be had. Will Comcast enter the fray and make a bid for Warner Brothers? It seems unlikely that Roberts would be interested in a bidding war.

And yet, the $71 billion enterprise value of WBD is roughly seven times EBITDA. Not cheap, but not unreasonable either. This multiple is slightly deceptive. Film and television content rights cost Warner Brothers more than $12 billion per year in working capital. Still, cash provided by operations was $5.4 billion in 2024 on $39.3 billion in revenues. All of the surplus funds went towards debt reduction.

William Cohan, the noted author and former Wall Street banker, has followed the Comcast story closely. Writes Cohan, “Though he was the son of Comcast architect Ralph Roberts, the entrepreneur who built the cable systems empire that mushroomed into the media behemoth, Brian rejected any sort of born-on-third base implications. He was immensely driven, aggressive, ambitious, and carnivorous.” While it may be nothing more than an anecdote, the word carnivorous is not usually associated with a patrician Philadelphia gentleman content with counting his stack of money. Growth is in his DNA. So is discipline.

Let’s turn to the value of the business.

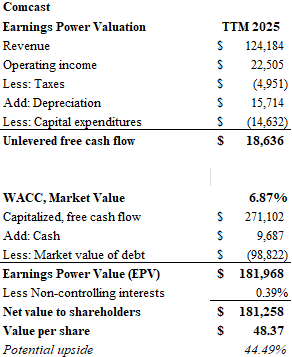

The earnings power valuation (EPV) model results in an estimated price of $48 for Comcast’s shares. This represents potential upside of over 43% compared to its current $33.50 trading level.

Comcast is rated A- by Standard & Poor’s. The company benefits from a well-managed debt profile amounting to $101.5 billion at the end of the June 2025 quarter. The weighted average interest rate on Comcast debt is 3.8% and the weighted average maturity is 15 years. Given that rates for similar quality obligations would be approximately 4.8% today, Comcast debt carries a market discount which puts it in the range of $98 billion.

The weighted average cost of capital for Comcast was calculated at 6.87%. This represents the aforementioned 4.8% debt cost (or about 3.7% after taxes) accounting for 41.5% of the company’s capital, and an equity cost imputed at 9.1%. The cost of equity is precisely imprecise. I don’t use beta, and I also don’t select an arbitrary “hurdle” rate. My cost of equity is a sum of the 10-Year Treasury Note at 4.03% plus a 0.75% debt spread for A- paper. Finally, I add an equity risk premium of 4.33%. The result is an equity cost of 9.1%, which seems reasonable given Comcast’s stable cash flow.

Operating income over the trailing twelve-month period amounted to $22.5 billion. Subtracting taxes of $5 billion, adding depreciation of $15.7 billion and subtracting capital expenditures of $14.6 billion, leads to unlevered free cash flow of $18.6 billion. Divide this number by the 6.87% WACC, and you have a capitalized gross value of $271.1 billion. Subtracting net debt of approximately $89 billion leads to a value for shareholders of $181.2 billion, or roughly $48 per share.

Patience will ultimately prove to be profitable for Comcast investors. While one waits for Roberts and his team to take advantage of turmoil in the Disney, Paramount and Warner Brothers universe, share repurchases and a hearty dividend make the waiting worthwhile.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2025-09-14 22:45:532025-09-15 09:19:06Jurassic World

Unless you’re shopping for vacant office buildings in ghostly business parks or depleted central business districts, there aren’t many bargains in commercial real estate. Investment cap rates defy logic. Plentiful sources of capital chase yields that are often below the cost of debt. This “negative leverage” conundrum only makes sense if we have major rent inflation. While this may well turn out to be true, inflation isn’t a one-way street. It will be difficult for rents to outpace operating expenses. Insurance and labor costs march relentlessly upwards, and I don’t expect struggling city governments to offer any property tax relief. But when your debt costs are fixed, inflation is usually your friend.

So are we witnessing a rational investment decision based on inflation outrunning the cost of debt, or are investors simply justfying a need to deploy capital? I suspect its mostly the latter. Asset prices across all sectors are at peak metrics. The casino is open. ETFs outnumber stocks, cryptocurrency treasury companies trade for double their underlying “assets”, and credit markets are priced to perfection. NVDIA dropped 3.4% on Friday. While this decline is eye-catching, the fact that it amounts to $143 billion – a dollar figure on par with the entire market capitalization of companies like Progressive Insurance and Lowe’s – should make one pause.

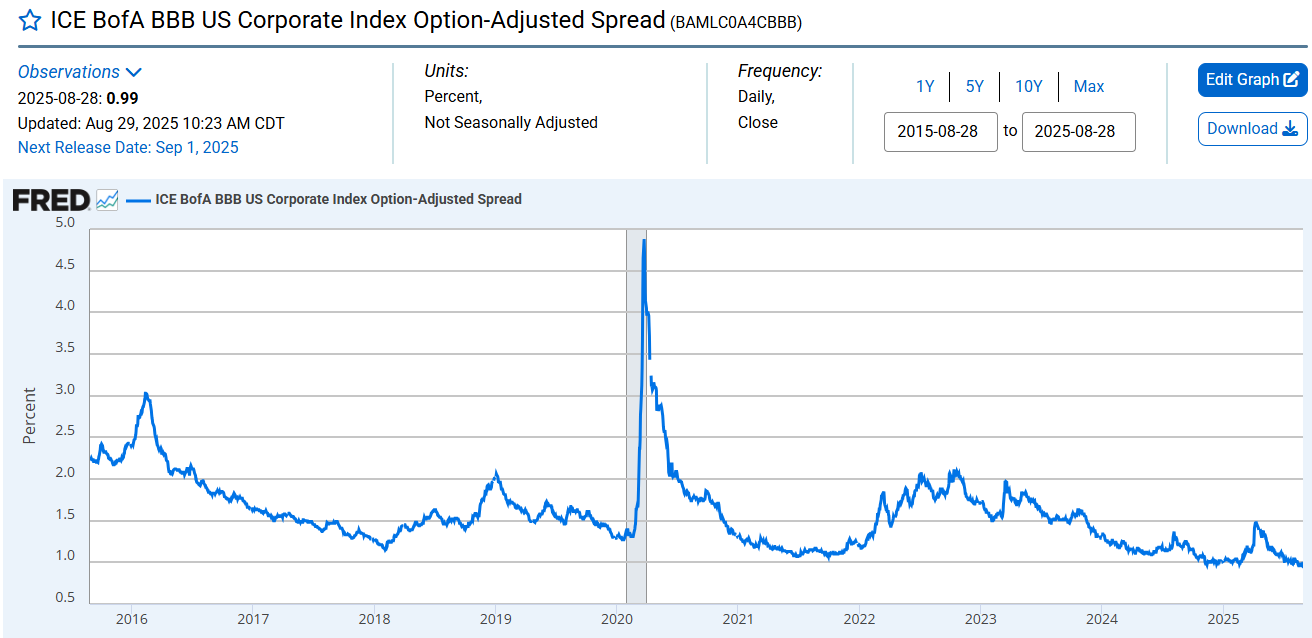

Nothing causes whiplash more than a painful case of mean reversion. Spreads have rarely been tighter. BBB spreads, a decent proxy for real estate cap rates, are below 1%. Meanwhile, new apartment deliveries are at generational highs. Many “hot” markets like Austin and Denver, now face an apartment glut. That rent inflation you were hoping for? It may take a while.

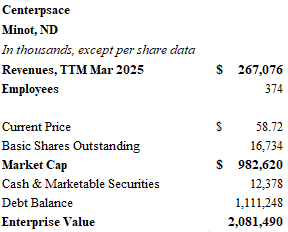

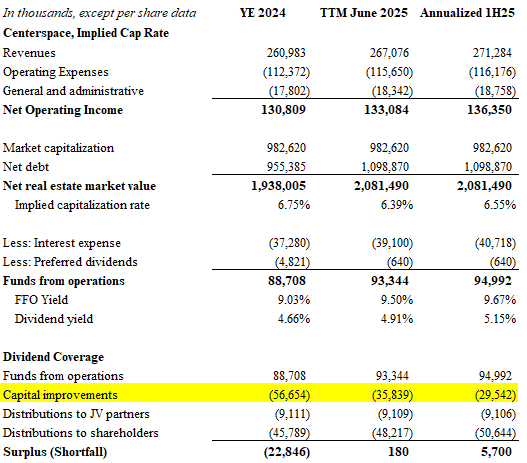

Given this backdrop, finding bargains among publicly traded apartment real estate investment trusts (REITs) is even more difficult. Let’s take the case of Centerspace, a Minot, North Dakota REIT with a market capitalization of $983 million. Centerspace (CSR) owns 13,353 units across the northern Midwest. Debt exceeds $1.1 billion. CSR has a strong presence in the Minneapolis area but has made an expansion push into Rocky Mountain markets. The 5.15% dividend yield looks appealing from a distance. Unfortunately, recent acquisitions at lofty prices will probably not improve the share price.

Investors in CSR have not had much joy over the past five years. Shares hover near $60, which is about where it stood prior to the pandemic. To management’s credit, CSR has begun to trade out of aging B-quality assets in favor of newly constructed apartment communities. The company also benefits from savvy borrowing moves during the COVID era. The cost of debt is safely below 4% and has a long maturity runway.

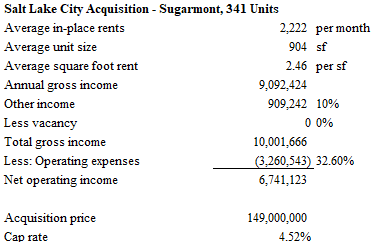

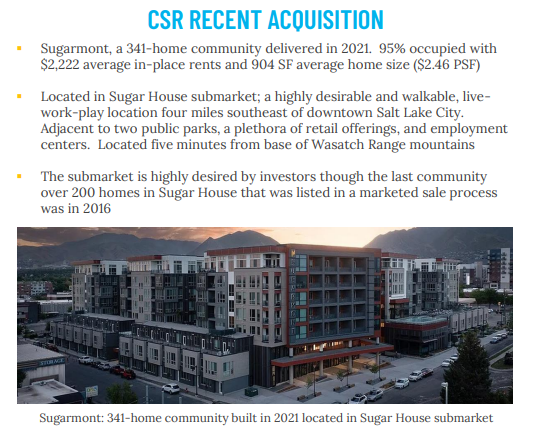

Efforts to modernize the portfolio seem to be having a positive impact on cash flow. Recent new acquisitions include a $149 million purchase of 341 units in Salt Lake City and a 420-unit property in Fort Collins, Colorado for $132.2 million.

In 2024, Centerspace generated $88.7 million in funds from operations (FFO). After capital improvements of $56.7 million, distributions to JV partners and shareholder dividends, free cash flow was negative $22.8 million. The dividend appears to be on a more sustainable path today. Capital improvements are on trend to decrease to $29.5 million which will produce $5.7 million of positive cash flow.

The acquisitions should enhance these results as they begin to filter through the income statement. However, it is hard to see how CSR meaningfully improves the languishing share price. The acquisition of Sugarmont, the 341-unit Salt Lake City property, wasn’t exactly a bargain. CSR paid $149 million for the vintage 2021 asset. I am not familiar with the SLC market, but it seems likely that the $437,000 per-unit price is not far from today’s inflated replacement costs. My estimation is that the purchase was made at a cap rate below 4.5%. Although CSR stands to benefit from the lower operating costs of a newer asset and a market with solid demographics, asset purchases at rates below the current dividend yield are unlikely to levitate share performance.

CSR informs us that they bought Sugarmont with average in-place rents of $2,222 per month. To be generous, I added 10% for other income. This would include items like pet fees, application fees, parking rent, and utility reimbursements. I was even more generous by assuming zero vacancy. Next, I took management at face value and assumed an NOI margin above 67%. The resulting net operating income (NOI) is $6.74 million. This figure translates into a capitalization rate of 4.52% on $149 million.

The reality is that even vertically integrated REITs have a very hard time running properties more efficiently than a 62% NOI margin. I don’t know the real estate tax and insurance landscape in Utah, but maintaining such a low level of operating expenses will be a challenge for Centerspace. As the company continues to shed aging properties for new assets, the cash flow performance should improve as capital improvement requirements decrease. However, acquisitions at lofty prices, and at cap rates below the dividend yield, will not improve investor returns. As loans begin to mature, even at a palatable pace, the debt must reset to rates that are 100-200 basis points above current levels. Centerspace is a pass for me.

I have made this point many times in these pages: a REIT that fails to deploy capital at advantageous rates cannot grow without issuing new shares. Real estate investment trusts are exempt from income taxes so long as they distribute 90% of taxable income. The inability to grow through the reinvestment of retained earnings turns a REIT into a dilution machine. Chose wisely.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2025-09-01 11:48:482025-09-01 12:35:19Just a bit outside

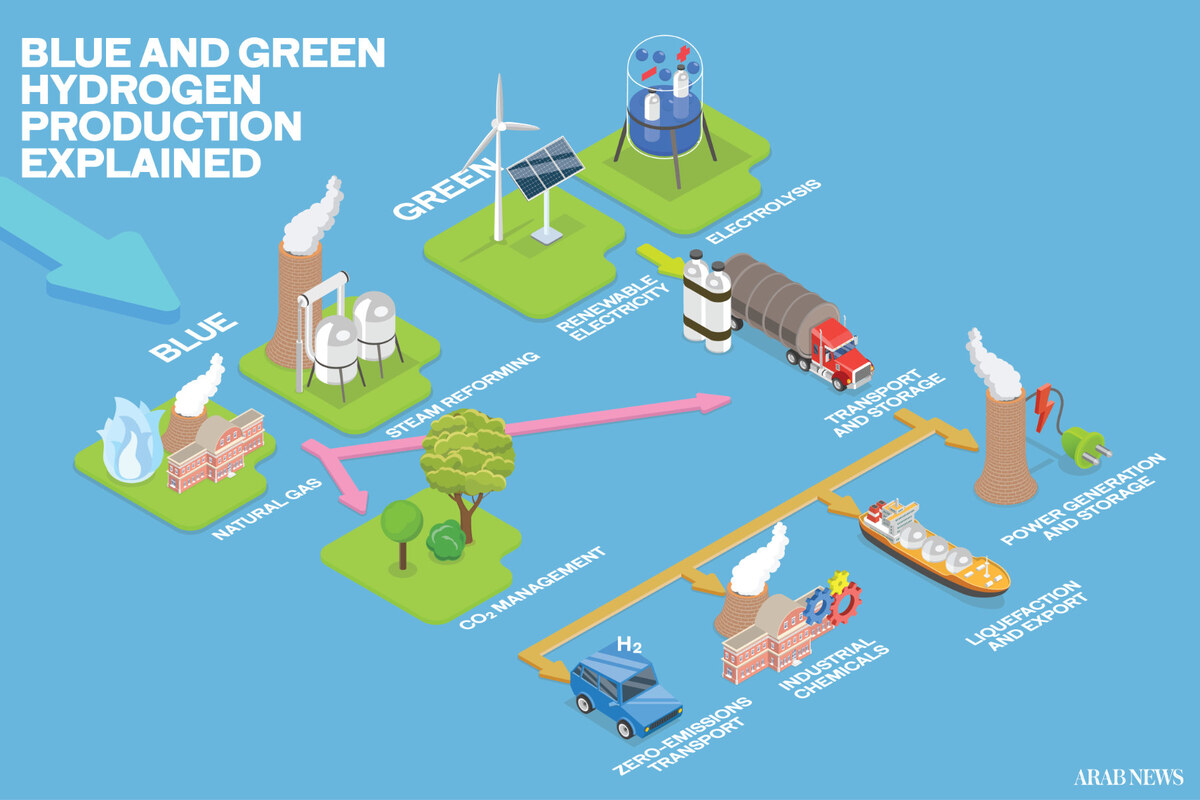

It was all going so well. Cigars and brandy around the hearth. Silk and cashmere. Fine Corinthian leather. The big industrial gas companies were having a jolly good time at the Oligopoly Club. Air Liquide, Linde, Taiyo Nippon Sanso and Air Products shared some laughs and enjoyed a few games of whist.

But across the street, a new eco-friendly club was opening. It was 2022, and the party was just starting. The DJ was laying down some insane beats. Air Products dreamily gazed through leaded glass at the crowd lining up behind the velvet ropes. It’s now or never…

Pulse quickening, cash in hand, Air Products suddenly stood below the green backlit sign. Club H2. One bouncer whispered to the other. Are they pointing at me? I’m in. This is happening.

Once inside, Air Products wasn’t so sure they made a good decision. Bottle service? Really? This seemed frivolous, but the hostess insisted. Three magnums of Cristal later, the room began to spin. Air Products saw an exit sign through the haze, but big guys in black t-shirts blocked the door. The next morning was, wait – it is the next morning.

I’m going to tell you about the misadventures of Air Products since 2022. The staid Allentown, Pennsylvania, company chased the illusive promises of a green future all the way to Saudi Arabia. Once the true costs and debt obligations became clear, shareholders revolted in early 2025. If you stick with me, I will also present two valuations for Air Products. Both methods indicate that the market price of the company’s shares is well above the intrinsic value of the business.

Industrial gases play a significant, if invisible, role in economic productivity. Hydrogen, oxygen, and their molecular cousins are essential for petroleum refining, fertilizer production, and the manufacture of metals and silicon wafers. Healthcare couldn’t function without oxygen and nitrogen. With such essential uses, industrial gas businesses can be very profitable.

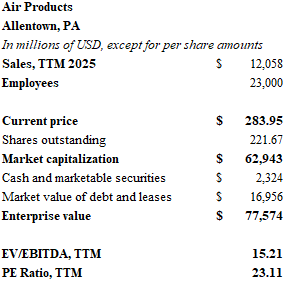

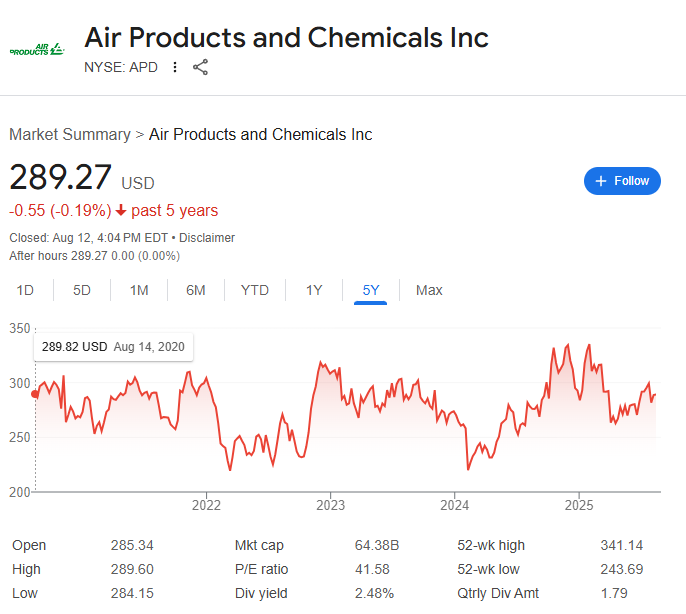

For many years, the world’s leading producer of industrial hydrogen was stable, boring, but steadily improving. Air Products was a stock you could recommend to your grandmother. APD generated over $12 billion in sales in fiscal year 2024. With a market capitalization of over $63 billion, Air Products grew earnings 7.5% per annum for a decade and dividends followed suit. Leverage was moderate. Capital investments flowed steadily from retained earnings. The company was responsible. It lived within its means. Returns on equity consistently posted in the mid-teens. Net margins hovered around 20%.

In 2022, Air Products was lured by the siren song of environmentally sustainable hydrogen production. Through a series of joint ventures, the company made substantial capital commitments. APD made an $8 billion promise to a blue hydrogen facility in Louisiana and a stunning $9 billion dollar commitment to a green hydrogen joint venture in Saudi Arabia. Three smaller sustainable hydrogen projects in the US accounted for a further $3.1 billion. Along the way, they divested their liquified natural gas business for $2 billion.

Air Products began to borrow. Big time. Long-term debt had hovered around $3 billion dollars for several years before surging to $7 billion after the pandemic, and then to over $13 billion today. Prior to 2022, capital expenditures were marching in line with depreciation at around $1 billion per annum. Recently, they have ballooned to over $4 billion per year. Free cash flow turned negative, and the dividend now seems precarious.

Most hydrogen is produced using a process known as steam methane reforming. High pressure steam separates hydrogen from methane (CH4), with carbon monoxide and carbon dioxide as the byproducts. Natural gas is usually the source of methane in this process. The less common production method is electrolysis which involves splitting water molecules using electricity. It’s uncommon because it’s very expensive.

Green hydrogen production means that the power for electrolysis is provided by renewable sources – mostly solar and wind power. Blue hydrogen is the moniker given to production using natural gas where the carbon byproducts are recaptured and stored. Both means of production are environmentally friendly, but they are dependent upon government subsidies to make the numbers work. The rug-pull for American production came from the Trump administration earlier this summer. Funding for major green and blue hydrogen production was dramatically curtailed.

Like the roommate holding your hair back while you heave into the toilet, shareholders recognized that the Cristal was a seriously bad idea. A proxy battle led by Mantle Ridge Capital resulted in the replacement of three directors and the installation of a new CEO early in 2025. Eduardo Menezes, who replaced the octogenarian Seifi Ghasemi at the helm, wasted no time shutting down three green and blue hydrogen joint ventures in California, New York and Texas which resulted in a $3.1 billion write-off.

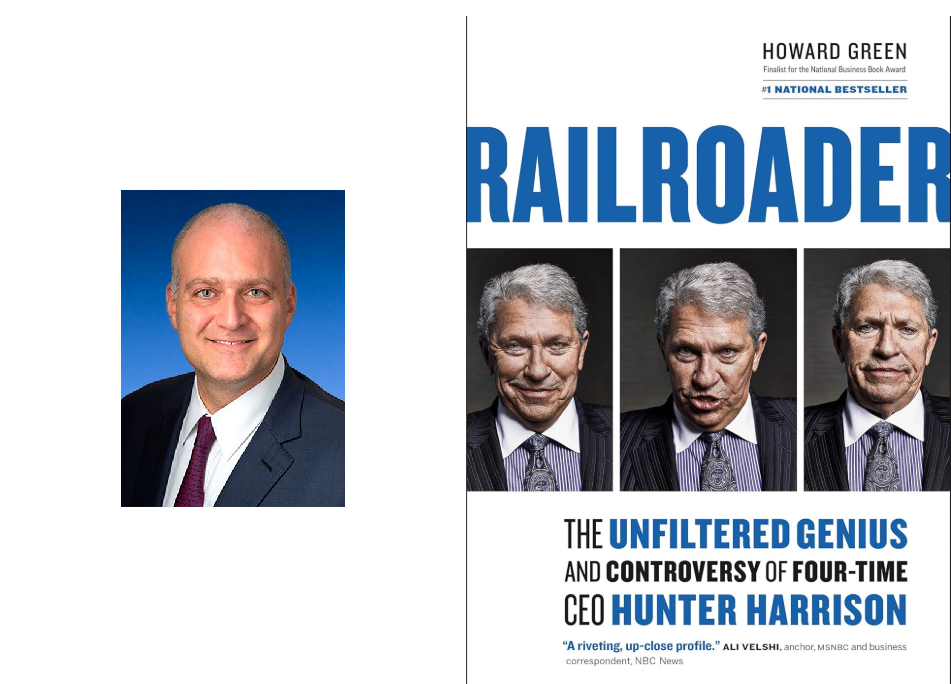

Ironically, nine years ago, Ghasemi had been installed by Mantle Ridge. By 2025, the worm had turned. Mantle Ridge is led by Paul Hilal, an activist investor who may be more famous for his tenure at Pershing Square with Bill Ackman. I first learned about Hilal while reading the highly entertaining autobiography of Hunter Harrison, Railroader. Harrison was a force of nature, and he revolutionized the railroad industry.

Pershing Square’s 2012 activist campaign for Canadian Pacific was arguably one of the finest investments in modern market history. While Ackman grabbed the headlines, it was Hilal who worked the numbers and recruited Harrison – already an industry legend – to western Canada. People said you could never get CP’s operating ratio below 60% because of the mountainous terrain. Harrison did it, and more.

So, when I see Hilal’s involvement with a company it comes with serious gravitas. The man knows how to generate shareholder value. The question now becomes, has Air Products mired itself so deeply in unfeasible green and blue hydrogen projects that its future profitability is in doubt?

I think the answer is yes. Menezes and Hilal have a long road ahead of them. While the Louisiana project may turn out to be a winner, the Saudi Arabian green hydrogen investment seems destined for trouble. Air Products has a 30-year offtake agreement for the ammonia expected to be produced by the project. While they have obtained a take-or-pay commitment from TotalEnergies for a third of future production, the lack of foreseeable sales is a dark cloud on the horizon.

The Saudi project is known as NEOM Green Hydrogen (NGHC), and it is breathtaking in its ambition and lack of market potential. A joint venture between Air Products and Saudi power companies, the massive site on the Red Sea will have 4 gigawatts of solar and wind power. By 2027, the venture is expected to produce 1.2 million metric tons of green ammonia per year. The ammonia is useful for fertilizer production, but it also aims to become a source of clean fuel.

Scientists have yearned for a hydrogen power solution for decades. A hypothetical pipeline route was drawn for Europe during the 1970’s. Many scientists regard hydrogen as the holy grail of clean energy (all that water!), yet production is economically unfeasible without massive government subsidies. Transport and storage is highly complicated and unproven.

NGHC is one of the industrial centerpieces of the futuristic master-planned development known as Neom. The vision, led by the Saudi crown prince, is to build a modern city of over a million people with a cost of over $1 trillion. It is designed to showcase the kingdom’s transformation away from fossil fuels and act as a technological innovation hub for the region. Already well over budget, the project has been scaled back. Yet NGHC moves forward, and construction is nearly 80% complete.

Air Products will tell you that you shouldn’t worry about NGHC because the financing in non-recourse. If that helps investors sleep at night, remember that this is a country that once held several errant business leaders captive at the Riyadh Ritz-Carlton for several weeks. Is there really such a thing as non-recourse when it comes to Saudi Arabia? You get a strange feeling when you watch Cristiano Ronaldo talk about playing soccer in his adopted land. Like maybe his soul has left his body. I had the same sinking feeling watching the Saudi national anthem played before the Bud Crawford fight.

Air Products is all-in on Louisiana and all-in on Neom. Economics be damned.

Air Products’ share price rallied after the boardroom coup d’etat. Investors seem placated by the choice of Menezes and they hope the steady returns of the past can be replicated once the new projects come online. After all, a 15% return on the $17 billion of green and blue hydrogen investments would effectively double current levels of net income which amounted to roughly $2.8 billion over the trailing twelve-month period.

Failure to deliver, however, and the company faces years of painful asset write-downs and a debt hangover. With few customers for Saudi green hydrogen on the horizon, the latter prospect seems more likely.

I present two valuation models below. The first is an earnings power valuation. The simple approach is advocated by Bruce Greenwald, heir to the Columbia value investment lineage that descends from Ben Graham. The model for EPV is simple. Take normalized free cash flow, or “owner’s earnings” in Buffett’s parlance, and divide by the weighted average cost of the firm’s capital.

The major limitation with the Greenwald method is its inability to account for growth. It takes the past results and capitalizes them, making no calculations for the future.

Value investors are a lonely bunch. The market has moved on. In a world trading on vibes and memes, the value investor is as quaint and archaic as the old boys’ club in the first paragraph. One could take a shot at projecting cash flows into the future and discounting them to the present. But the future is so uncertain. So someone from the value investment world needed to step up and properly account for a company’s future growth.

Into the breach stepped Stephen Penman and Peter Pope, again of the Columbian tradition. Their bookFinancial Statement Analysis for Value Investing(Columbia U. Press, 2025), is an excellent addition to the canon. They are accountants, and they contend that growth is only valuable to the extent that future earnings exceed a hurdle rate of return. If a company’s net earnings represent a 12% return on the company’s book equity, and the hurdle for such a company is 10%, then one can figure that this additional 2% is where real value is created.

They take the book value of the company’s equity and add a capitalized value for these residual or surplus earnings. Growth is factored in the denominator. The higher the growth, the lower the denominator, the higher the residual value.

A value investor can solve for the growth rate to see if a price makes sense. They offer a compelling example of Buffett’s purchase of Apple. At the time, in 2016, solving for the “g” in the growth portion of the equation showed that Apple’s price anticipated only a 2% growth rate. It was certainly a safe wager to think that Apple could manage better than 2% growth.

The problem with the model is that the authors don’t have much of an answer for the hurdle rates they choose. Yes, they spend several pages talking about risk and leverage, but ultimately they settle on the investor’s preference. The reader craves Damoradan’s rigorous precision. Penman and Pope (and Munger and Buffett) scoff at complicated equations. Precision can be precisely wrong. They would probably contend that its better to have that margin of safety in a 12% hurdle rate for a risky venture, than calculate some kind of Frankenstein-WACC with beta at its core.

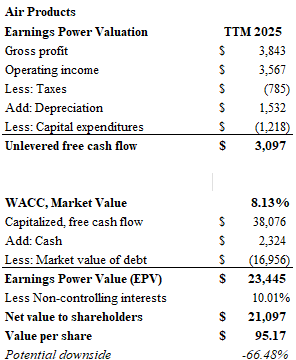

The earnings power valuation (EPV), a zero-growth model, indicates that APD may be worth less than $100 per share. This would mark a 66% decline from current levels. In this model, unlevered free cash flow is divided by a weighted average cost of capital of 8.13% to arrive at a value of $23.5 billion after subtracting $14.6 billion for the market value of net debt.

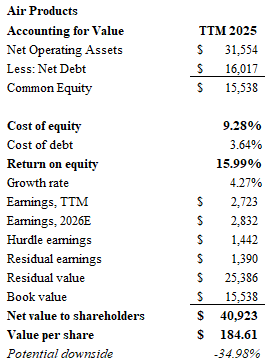

The “accounting for value model” or “Penman-Pope Model” is a lot more forgiving because it makes an accommodation for growth. We start with the base. Penman and Pope frequently ask the reader to “take the balance sheet with you.” Here we use the book value of equity, $15.5 billion, as the first half of the equation.

The second half of the equation is determining residual earnings for the following year. In this case, I simply increased trailing twelve-month earnings by 4%. This may be slightly hopeful, but its not unreasonable. Note: unlike the unlevered cashflows of the EPV model, earnings are net of debt expenditures. The “hurdle” I set for Air Products was 9.28%. This is the 10-year treasury yield, plus a spread for the company’s A-rated debt, and an additional 4.33% equity risk premium.

Air Products delivered a 16% return on equity for the TTM 2025 period, so the residual earnings – the amount above the hurdle – is $1.4 billion. The figure is divided by a denominator of r – g where r is the 9.28% cost of equity less a proxy for growth. In this case I used 4.27% (the 10-year Treasury yield). The residual value is approximately $25.4 billion. Added to book value, the sum is $40.9 billion or about $185 per share. This represents a level 35% below the market price.

The aspect of the model that is appealing, is that it allows one to see whether growth is reasonable. In other words, what level of growth would justify today’s price of $283 per share? The answer is 6.6%. If you think world demand for hydrogen meets or exceeds this level, you would conclude that Air Products is fairly valued.

So, these are just my estimates and they are certainly crude. I don’t make any attempts to understand the potential demand for green hydrogen in Europe or the possibility that production costs could be dramatically reduced through lower energy inputs from solar power. I certainly would think twice before betting against Paul Hilal.

However, despite our best intentions to improve the environment, the efforts at carbon recapture and electric hydrolysis have relied heavily on government subsidies. As governments reckon with yawning fiscal gaps and a need to re-arm for global conflicts, it seems likely that the green ammonia produced in Saudi Arabia lacks an end-market. The uncomfortable meetings in the Air Products boardroom could persist for many years as assets are written-down and debt service gnaws away the bottom line.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

http://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpg00adminhttp://www.alchemydevelopment.com/wp-content/uploads/2017/07/AlchemyLogo-1030x233.jpgadmin2025-08-12 16:06:182025-08-12 16:51:58Hot Air

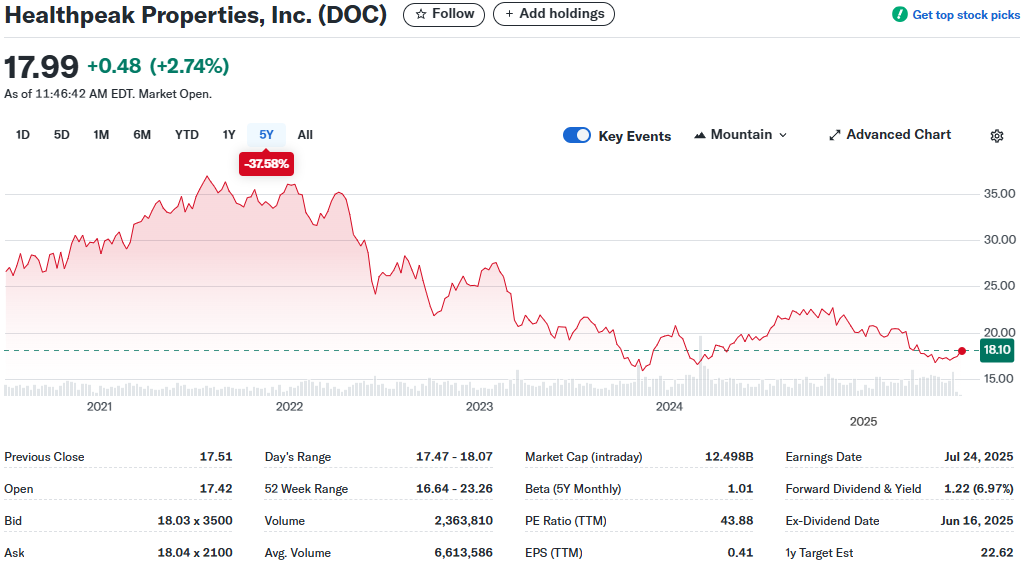

I don’t have much time this week, so I’m in shallow water. I’ve got a little back-of-the envelope one for you. Healthpeak Properties Trust (DOC) is a Denver-based owner of outpatient medical buildings and lab space. The company merged with Physicians Realty Trust in 2024. The stock has not performed well, but the 7% dividend yield is very enticing. DOC trades with a market cap of $12.5 billion.

The dividend seems well-covered, however the lab space (31% of revenues) is a wildcard. There has been an incredible amount of new supply, and the biotech market isn’t exactly robust. Despite the risks, this one deserves a closer look.

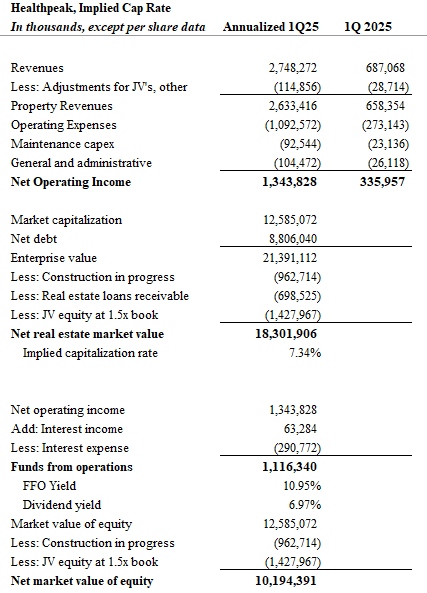

For now, here are my rough numbers. I am taking a leap of faith by annualizing just one quarter for the balance of 2025. The stock trades with an FFO yield of approximately 11%. I subtracted maintenance capital expenditures (taking management at face value) from net operating income, and it appears that the real estate trades for an implied cap rate of 7.3%. This seems pretty high, but it probably reflects the risks associated with lab space tenants. Leverage is also a little higher than I’d prefer, but the maturity timetable appears manageable.

The problem with Healthpeak, and so many other office REITs for that matter, is “what does upside look like?” How does this story improve? It’s not like the National Intitutes of Health is going to start writing grant checks for new clinical trials any time soon. Healthpeak doesn’t have the ability to refinance debt any more cheaply than what’s on its books today.

Beware the siren song of high dividend yields. Usually the market knows something about risk that you don’t. If you’re just buying debt with a single-B credit rating, you should definitely receive more than 7% on your money. The “equity” may not be worth more than a similar junk bond.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.

I keep a $5,000 short position in Welltower. It’s my hairshirt. I know it won’t change anything. My penance will not help mankind. I continue to view Welltower (WELL) as the most absurdly overvalued real estate investment trust in the market today. The company is a provider of senior living residential facilities. Welltower mesmerizes all who worhsip at the orthodox church of demographics. “Thou shalt not question thy trend of aging baby boomers” is the first commandment obeyed by all who kneel at the altar. Yet here I am. Tilting at windmills.