Don’t know much biology

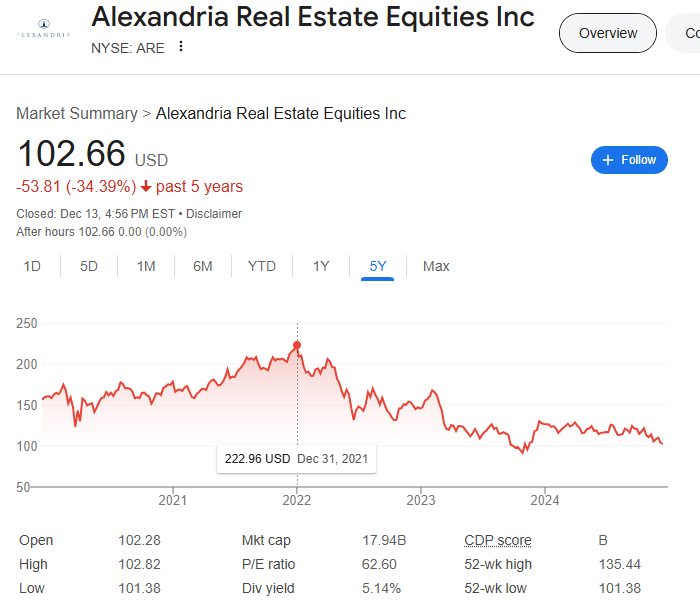

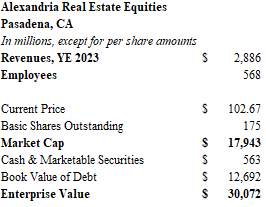

Alexandria Real Estate Equities is the leading landlord for the pharmaceutical and biotechnology industries. The Pasadena-based firm boasts 41.8 million square feet of office and laboratory space, with a further 5.3 million square feet under construction. Shares of the real estate investment trust with the ticker ARE closed at $102.66 on Friday. Total market capitalization of $18 billion represents a slight discount to the book value of equity on the balance sheet.

Alexandria focuses on campus “clusters” where it has been proven that the proximity of multiple science innovators stimulates creativity. These clusters have been developed in locations with robust university ecosystems such as Boston, the Bay Area, San Diego, New York, the DC metro, Seattle, and the “Research Triangle” of North Carolina. Most recently, the company announced a 260,000 square foot lease with the bacterial disease biotech firm Vaxcyte at the San Carlos, CA campus.

Occupancy is a healthy 94.7% across the portfolio. Alexandria’s balance sheet shows $33 billion of real estate assets (undepreciated) and $12 billion of debt. Standard & Poor’s regards the debt as investment grade with a BBB+ rating.

Despite the good metrics, Alexandria stock has been pummeled over the past three years, falling by more than half from the $223 peak at the end of 2021. The biotech industry boomed during the early stages of the pandemic, but the subsequent collapse has been brutal. Deals in the pharmaceutical industry have fallen to their lowest level in a decade. This is a far cry from the halcyon days of 2020 and 2021, when over 183 firms raised more than $30 billion from initial public offerings. Today, most trade below their IPO price, and many are cash-burning zombies.

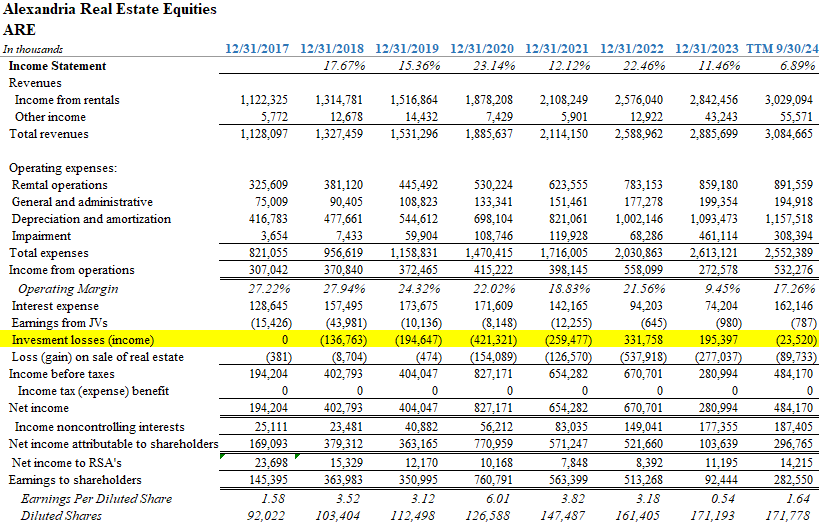

Over the years, Alexandria has invested in many of its tenants with it’s own venture capital arm. Between 2018 and 2021, Alexandria booked over $1 billion in investment gains on its portfolio.

Unfortunately, as the market turned hostile, investment losses in 2022 and 2023 exceeded $527 million. At the end of September. Alexandria carried $1.5 billion of investments among its assets. Some are publicly-traded and marked-to-market on a consistent basis, but most are illiquid and the value is highly subjective.

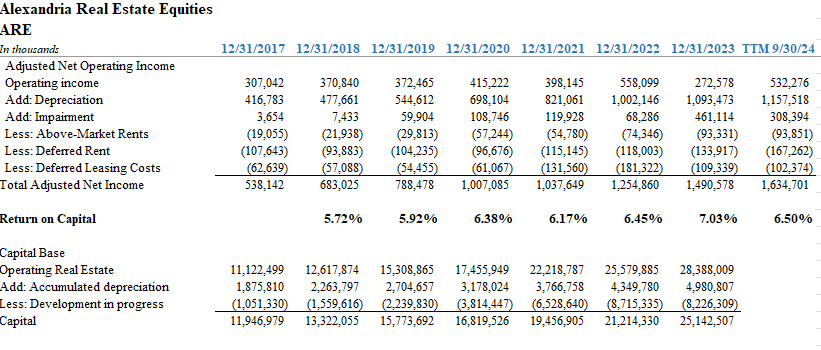

Trouble in the biotech industry also led to losses of rental income. Between 2020 and 2023, ARE faced lease impairments in excess of $750 million.

Is Alexandria’s stock now a bargain? Not quite. I consider a stock trading 25% or more below its intrinsic value to signal an investment green light. Based on my calculations, the stock trades at a 7% discount to the value of its underlying assets.

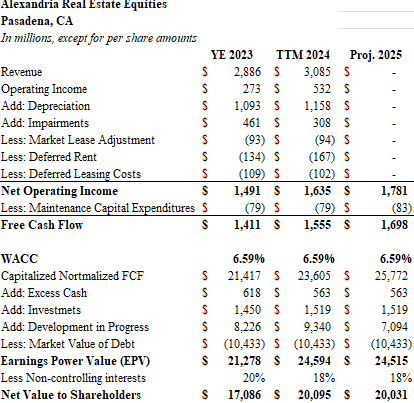

Intrinsic value calculation:

By my estimates, 2025 free cash flow will be approximately $1.7 billion. Capitalizing this amount at 6.59% leads to a value of $25.7 billion for the operating real estate. Adding development in progress and the company’s investment portfolio, both at book value, leads to a total asset value of $34.9 billion. Subtracting the market value of debt results in a net value of $24.5 billion. Many of the company’s assets are held in joint ventures with developers, so about 18% of the value is attributable to these partners, leaving a net asset value of $20 billion.

There are some important caveats to consider:

- I’ve mentioned the risky nature of the venture-backed tenants. They sow the seeds of major upside for Alexandria, but they could also prove to be a source of future impairments.

- Interest expense is mostly capitalized. The company reported about $162 million of interest over the trailing twelve months. In reality, this figure is much higher. In 2023, about $364 million of interest was capitalized because it was related to debt on new developments. This is entirely appropriate, but the failure to lease pending space could lead to a drag on results if this interest must be deducted from operating profits

- New developments are significantly more costly. Although ARE is only expanding its portfolio by 13% with its current development pipeline, the cost of new projects equate to more than 28% of undepreciated book real estate assets. Construction costs suffered massive inflation since 2020, and it will be difficult to obtain future rents that need to be 30-40% higher than current market levels to drive adequate returns.

- Returns on capital have never been much better than 6%. Taking a look at cash operating income as a percentage of undepreciated operating assets shows a company that has earned returns that aren’t exactly eye-popping. This is institutional-quality real estate with very low debt costs, so the 6% neighborhood may be respectable, but its not the kind of number that will drive exceptional growth.

Which brings me to my final issue with all REITs in an environment of sustained higher interest rates: the prospect of equity dilution.

REITs, by virtue of their tax-exempt status, must distribute most of their profits. Retained earnings are a limited source of growth capital. External capital and the reinvestment of gains from property sales provide the funding for growth. In the low-rate era between 2009 and 2021, earning a 6.5% return on capital drove returns on equity to the low double digits when borrowing costs were in the 3-4% range. Indeed, as share count rose by 65% over the past six years, assets on the balance sheet increased by 170%. This positive leverage is the key to building real estate wealth.

In the current rate environment, the math isn’t so hot. If Alexandria finds itself unable to grow with low-cost debt, incremental shares must be offered to the public in ever-increasing quantities. When capital is expensive, REIT shareholders face dilution.

So where does this leave us?

Alexandria has a solid business renting space to big pharma companies. Most of its debt is financed at 3.8% for another 13 years. The stock trades at a slight discount and offers a nice dividend in excess of 5%. However, ARE also relies on the ability of many cash-burning high-risk ventures to continue paying rent.

Many firms will fail. Some may become blockbusters. Alexandria doesn’t have to bet on one horse, it owns the thoroughbred farm. They know which smaller tenants are growing and making progress on their drug pipelines. In fact, their venture business gives the firm upside when a tenant wins the derby.

If you have a favorable outlook on the biotechnology industry, Alexandria shares seem like a decent way to receive a nice dividend while a recovery forms. Indeed, there are signs of a thaw. Several new funds have found traction. Venture money may be flowing to the industry once again.

As for me, I would prefer to wait for a further decline in the share price to make an acquisition. The company has $9.3 billion of development in progress that may struggle to find tenants willing to pay top dollar for lab space. The new paradigm for inflation-adjusted rents has not been “battle-tested” in a market where firms are looking to preserve cash. Splashing out big dollars on fancy office space probably won’t sit well with venture capital investors who have seen much of their pandemic era gains evaporate. Corporate austerity may be the new watchword for the biotech industry.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.