In the 1950’s, some of Ben Graham’s disciples would exchange investment ideas. They weren’t managing vast amounts of capital at the time, so investors like Bill Ruane and Walter Schloss might pass along a thesis about an undervalued business to Warren Buffett and vice versa. They called the practice “coat-tailing.” By teaming their resources, their coordinated efforts might trigger a change at a company. New leadership, asset sales, dividends, etc. By the 1960’s Buffett kept his ideas to himself. He was wealthy enough to hoard his best plans.

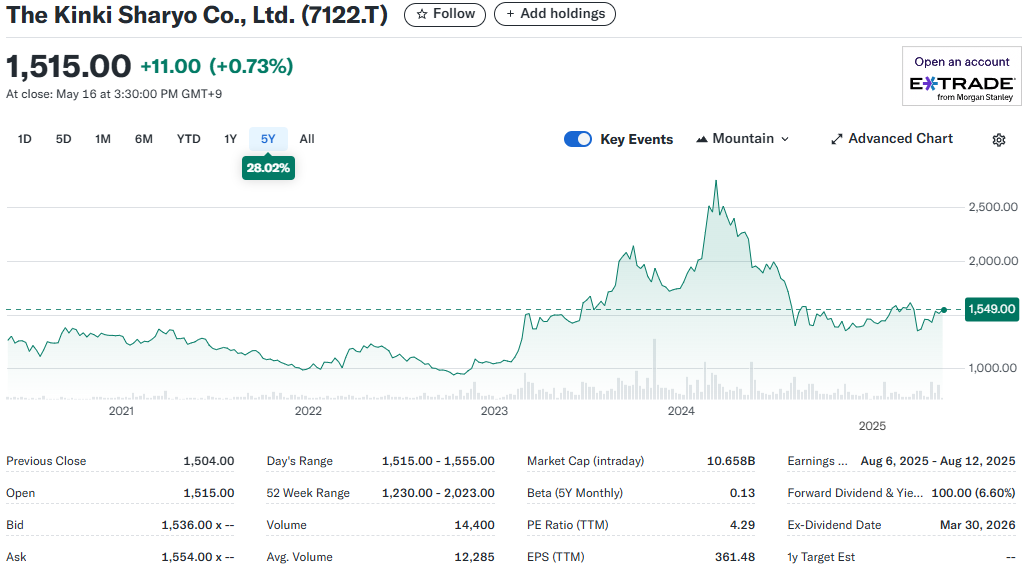

I am coat-tailing this week on the research of Altay Capital, a value investor with a focus on Asian companies. Altay recently posted a compelling investment case for Kinki Sharyo (T.7122), a Japanese manufacturer of railroad vehicles based in Osaka. With a market capitalization just below ¥10.5 billion ($72 million), the company is primarily focused on light rail and subway passenger vehicles. The domestic Japanese market accounted for 69% of sales in FY 2024, but their work can also be seen riding the mass transit systems of Los Angeles, Boston, Dallas, Seattle and Phoenix. Kinki Sharyo delivers cars to the Doha and Dubai metro systems as well. Altay Capital believes that the company is a candidate for a full takeover by its parent, Kintetsu, which holds over 40% of the stock.

Kinki Sharyo is incredibly cheap. Trading at an EV/EBITDA multiple of 2x, the company could be worth more than double its current share price. I won’t elaborate on the characteristics of the business, or some of the pros and cons. Altay’s article provides all the rationale you need. My intention here is to simply offer a few more calculations to bolster the investment thesis.

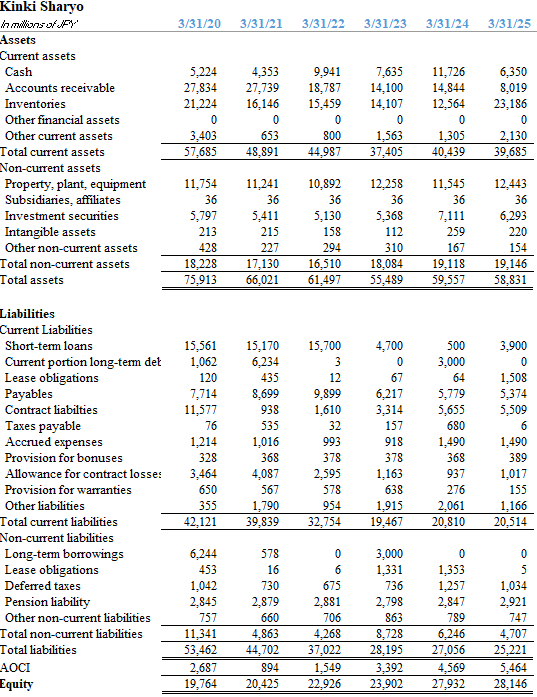

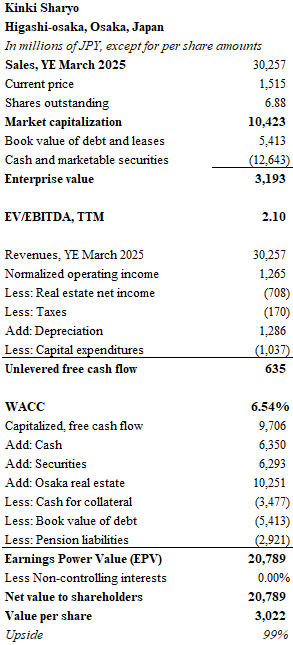

I am attracted to the real estate. Kinki Sharyo generates about ¥700 million of net income annually from commercial properties in Osaka. The fair value of these assets amounts to approximately ¥10.25 billion. There’s more. Kinki Sharyo just closed the books on fiscal year 2025 in March with over ¥6.3 billion of cash on the balance sheet. The company holds another ¥6.3 billion of liquid investment securities. On the liabilities side, the business has debt and leases of ¥5.4 billion and pension liabilities of ¥2.9 billion. We haven’t looked at the railway business yet, and the net assets already exceed ¥14.5 billion.

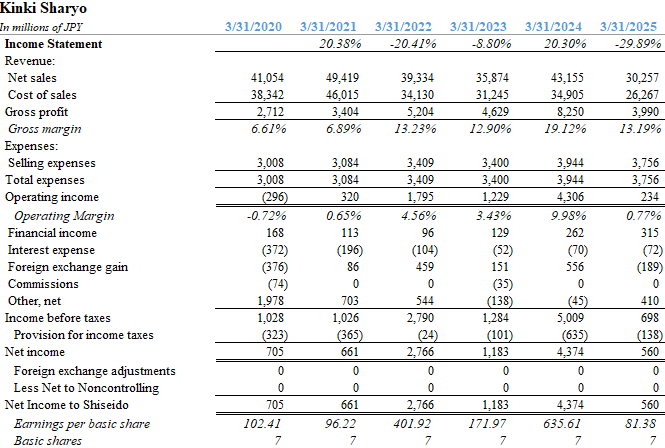

Per my customary practice, I employed an earnings power valuation of the business. First, I normalized operating income over six years. This included the loss-making year of the pandemic in 2020 as well as the surge of deliveries in 2024 which produced ¥4.3 billion of operating income. FY 2025 EBIT was 234 million yen. The six-year average is ¥1.265 billion. Next, ¥708 million of real estate income was subtracted, along with taxes, and just over ¥1 billion representing FY 2025 capital expenditures. ¥1.3 billion of depreciation was added back to arrive at normalized unlevered free cash flow of ¥635 million. This numerator was capitalized by 6.54%, a figure representing a weighted average cost of capital.

The WACC was computed using a cost of debt at 2.65% and a cost of equity of 8.75%. Although Kinki Sharyo pays barely more than 1% for its debt, I employed a rate that is 119 basis points over the current Japanese 10-year yield of 1.46% for the debt which accounts for 34% of capital. Kintetsu is rated BBB, so I applied the US spread to the Japanese yield. On the equity side, I took the risk premium for Japanese equities and default spread for Japanese bonds of 6.91% and added it to 1.46%. I figured 69% of equity is attributable to Japanese sales. The remainder was weighted towards US equity costs and about 12% for revenues derives from the “rest of the world”. My cost of capital feels a little low, but borrowing in yen keeps it that way.

The value of the rail business, by my computation, is just about ¥9.7 billion. This is rabout 85-90% of the depreciated book value of the company’s plant and equipment. By comparison, Alstom of France, trades at about 85% of book value. I added cash and securities, the Osaka real estate, and subtracted debt and pensions. To be conservative, I subtracted ¥3.5 billion of the cash because it is pledged as collateral for contracts in progress. The net calculation sums to ¥20.8 billion, or ¥3,022 per share. Kinki Sharyo is trades for half this amount. A true bargain.

The railcar business is cyclical, capital intensive and subject to the challenges of winning a new contract and delivering products over many subsequent months. The risks of an underpriced bid, production delays, raw material expense fluctuations and potential warranty claims all weigh on Kinki Sharyo. There is no denying that sales declined significantly in FY 2025 and there is little visibility into future bookings. The large infrastructure spending boost to transit systems in the United States is over. Maintenance contracts in Japan and growth in emerging markets will be needed to drive future sales. Despite these challenges, the share price reflects a wide margin of safety. The stock trades for less than the sum of investment assets on the balance sheet.

Tulip Mania or Dollar Hedge?

Is cryptocurrency a fantasy like Dutch tulips of the 1630’s, or is it a legitimate store of wealth? On the legitimate side would be the sophisticated blockchain system of accounting ledgers which offers a technologically advanced method of universal counting, sorting, and exchange. Then you have the uncertain future facing a US dollar eroded by inflation and foreign distrust. Gold has served as a store of value for centuries. Perhaps cryptocurrencies are the modern equivalent.

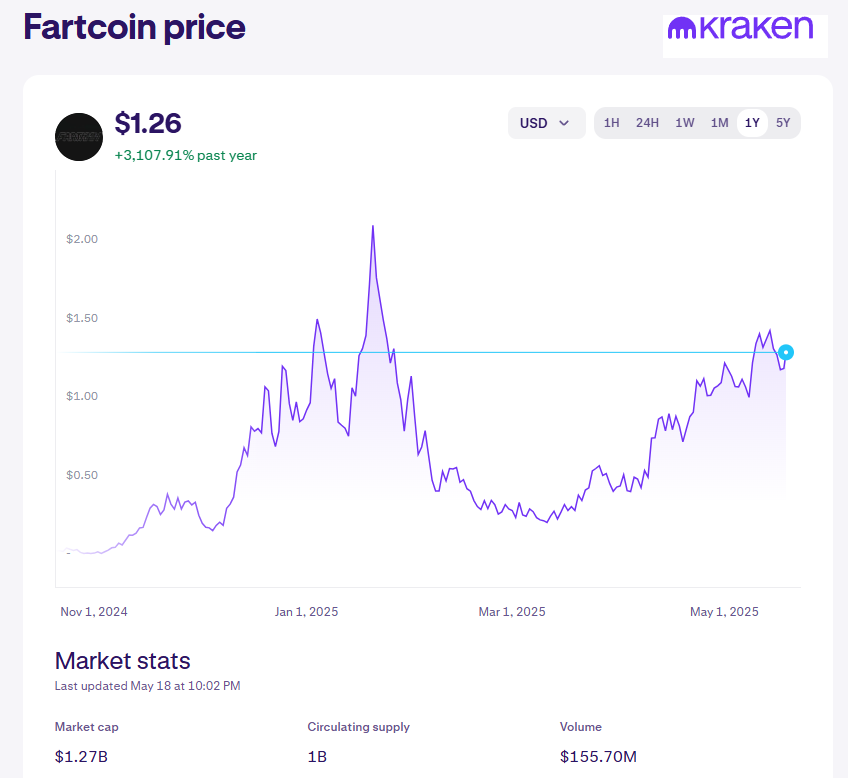

The case fo crypto-mania seems easier to prove. The original bitcoin was “minted” by a computer algorithm generated by an unknown programmer called Satoshi Nakamoto. The ”currency” has proven to be useful for criminals, but few others. And then there’s the world of “memecoins”. These are tokens that their creators sell to the public which represent, well, nothing at all. Exhibit A: Fartcoin. All the fartcoins in existence amount to $1.25 billion. We’re talking real money. The idea that something known as fartcoin has a value higher than zero is pure madness. Imagine presenting your financial statement to a bank and listing Fartcoin as an asset.

If you haven’t read any of Matt Levine’s columns, you need to. Nobody is better at separating the ridiculous from the sublime in modern finance. One of his favorite topics is the ability to buy stock in publicly traded companies that hold bitcoin. The most famous of these entities is MicroStrategy (MSTR), which is now known simply as Strategy, and led by the visionary (and/or delusional) Michael Saylor. If you buy stock in Saylor’s company you own shares in a business valued at $109.3 billion. Strategy holds bitcoin in the aggregate amount of $38.76 billion. They issue new shares, and they use the proceeds to buy bitcoin. On and on it goes. A perpetual money machine.

But there’s an obvious problem here. When you buy a share of MSTR, you are buying $1 of bitcoin for $3. Why would a rational human being undertake such a transaction? Why not just buy $1 of bitcoin for $1? Well, maybe you think that Saylor and his management team have better insights into managing this “portfolio”. What would you pay for such a brilliant management team?

Well, Berkshire Hathaway might be one comparison. Despite Warren Buffett’s retirement, Berkshire has some of the finest managers in the world. A lot of people talk about Warren Buffett’s capital allocation skills, but few discuss his ability to spot a talent. Berkshire Hathaway trades at a price to book value of 1.69x. It has never exceeded 2 times. We aren’t even talking about the dilution problem with MSTR. Berkshire hasn’t issued new shares in a generation. MSTR is constantly issuing $3 shares to buy $1 of assets.

Well, maybe you would rather hold bitcoin through a company because you trust the stock market more than the crypto market. You’re not sure you want to open an account at Coinbase. You might be a little nervous reading about the periodic hacks that occur at these “financial institutions”, or the horror stories of “lost wallets”. There are alternatives here too. One could simply buy the iShares bitcoin trust managed by BlackRock. Trading with the symbol IBIT, the ETF has a market capitalization of $56.5 billion. It’s price to “book” is 1x.

As Jim Chanos has pointed out, there is a way to hold these opposing views through arbitrage. You can believe that cryptocurrency has long term value and also believe that a speculative mania of vast proportions is currently underway. How does one go about making money from such cognitive dissonance? The trade would be to sell short MSTR while simultaneously holding a long position in IBIT. Over time, these contrasting positions should converge.

The Jam

You might have figured out that Paul Weller is one of my music heroes. The Jam released Down in the Tube Station at Midnight in October of 1978 and it reached 15 on the UK singles chart. It’s one of my favorite tracks and probably in my top five by The Jam. It’s definitely the best song I know about riding subway trains. I’d hate to see terminal decline set in for the El or MTA. It’s a convenient way to travel in a big city. As long as you don’t encounter “thugs who smell of pubs, and Wormwood Scrubs“, that is.

Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.