No Regrets

I decided I needed a soundtrack for this week’s article. The theme is regret – the feeling that you wish you could change something that’s already happened. Edith Piaf laid the mark down. She had no regrets at all. Defiantly, she announced:

Je repars á zéro. Non, rien de rien. Non, je ne regrette rien!

Non, je ne regrette rien (No, I Regret Nothing) topped French charts for seven weeks in 1960 and became more famous for its use in countless movies since. Edith is musical tonic for the gin of regret. Still feeling guilty about that nice guy you ghosted after you found out he owned six cats? Edith at full blast will fix that.

Need a song that shows a little remorse, but still basically says “f*ck ’em”? Leave it to Ol’ Blue Eyes. In 1969, Frank Sinatra crooned with feigned modesty:

Regrets, I’ve had a few. But then again, too few to mention… And more, much more than this, I did it my way.

Artists were more introspective in the post-Vietnam era. Regret began to fill the airwaves. Take the easy-going beach classic Margaritaville by Jimmy Buffett. The 1977 ballad seems innocuous on the surface. Tequila, salt, sand and sun. But don’t let those steel drums fool you. Margaritaville, the anthem for an entire cult following, is all about regret. Jimmy Buffett is basically drowning his sorrows because he knows he blew his chance at true love.

I know it’s my own damn fault.

By the 1990’s, Regret was on full display. All Apologies by Nirvana immediately comes to mind, but I prefer Pearl Jam’s Black for its gut-wrenching agony.

I know someday you’ll have a beautiful life. I know you’ll be a star in somebody else’s sky. But why, why can’t it be. Oh, can’t it be mine?

Need more? Johnny Cash covered Trent Reznor’s Hurt:

If I could start again. A million miles away. I would keep myself. I would find a way.

That’s some painful regret right there. If you’re reaching for the tissues, let’s close our little musical journey on a lighter note. Taylor Swift’s, Back to December:

It turns out freedom ain’t nothing but missing you.

Ah, that’s better.

Regret is a dish served cold in Leverkusen, Germany. If you call Bayer headquarters and get placed on hold, you probably have to listen to Radiohead. The regret of which I speak is the 2018 purchase of Monsanto for $63 billion. It has been nothing short of a disaster for the venerable aspirin-maker which dates its founding to 1863.

Bayer operates in three segments: Crop Science (2024 revenues, €22.3 billion), Pharmaceuticals (€18.1 billion), and Consumer Health (€5.9 billion). Crop Science features the RoundUp herbicide franchise and DeKalb seeds. Pharmaceuticals offer a wide range of treatments with success in cardiology and women’s health. Consumer Health includes the famous Aspirin brand as well as Aleve, Claritin, MiraLax, and AlkaSeltzer.

The Crop Science business presents the largest challenge. Between 2019 and 2024, Bayer has taken over $13 billion in goodwill impairment charges. The company has accumulated over $19 billion for litigation expenses. The problem has been claims that RoundUp, the indispensable weed-killer, causes cancer. Monsanto has reached settlement agreements on nearly 100,000 lawsuits for approximately $11 billion and estimates that 58,000 cases remain. However, Bayer won a significant victory last August when the US Circuit Court of Appeals ruled that Federal law shields the company from claims at the state level. The court rejected a plaintiff’s claim that Monsanto placed farmers in danger by failing to place a cancer warning label on the product. The ruling conflicts with other decisions and leads to a belief that the commerce-friendly US Supreme Court could soon weigh in and reduce Bayer’s liabilities.

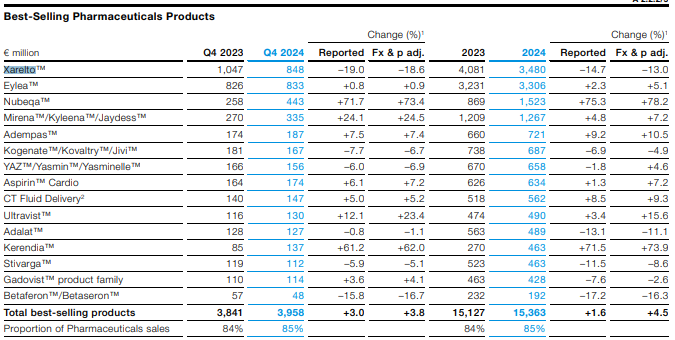

The Pharmaceutical division faces an urgent need to replenish its drug pipeline. Xarelto is Bayer’s bestselling drug, but its patent expired in 2024. Generics have started to cut into sales of the anti-coagulant. Xarelto sales topped $4 billion in 2023 and declined to $3.5 billion in 2024. The top 15 medicines accounted for $15.3 billion of sales, or 85% of the pharmaceutical segment. The next best performer is Eylea at $3.3 billion and 1% annual growth, and Nubeqa at $1.5 billion and 73% annual growth. The drugs are for retinal diseases and cancer treatment, respectively. Only a German company could withstand the irony of producing medicines to cure cancer while simultaneously making a herbicide that is a carcinogen. Somewhere, Friedrich Nietzsche is having a laugh.

Bayer has two missions: clean up the Monsanto litigation and create a more robust pipeline of pharmaceuticals. Bill Anderson, a native Texan, was hired in 2023 to lead Bayer. Anderson is a drug industry veteran, having previously run Genentech’s oncology, immunology and opthamology divisions. He later served as CEO of Genentech, a subsidiary of the Swiss drug-giant Roche, and ultimately ran Roche’s entire pharmaceuticals division. Given Anderson’s background expertise, there is speculation that once the RoundUp litigation has been arrested, the crop sciences business could be sold.

What we need to know is whether or not Bayer has the makings of a good value investment. For all of Bayer’s problems, this is still a multinational company that generated $4.5 billion of free cash flow in 2024. If you can handle the rocky ride ahead, Bayer could prove to be a very lucrative investment with a great deal of upside.

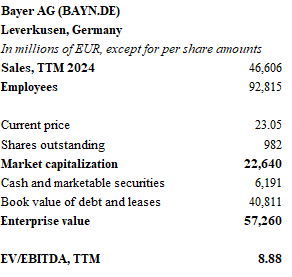

Shares trade on the DAX for about €23, giving the company a market capitalization of €22.6 billion, or $24.5 billion. American investors can buy ADRs with the BAYRY ticker for about $6.30 apiece. The company recently closed the books for 2024 and posted €46.6 billion of revenues, a decline of 9% from 2023. Operating income was €3.5 billion, with operating margins collapsing from 17.2% in 2023 to just below 7.5% in 2024. Mr. Anderson faces a stiff test.

Leverage is a concern. Over €40.8 billion of debt and leases weigh heavily. The board responded to the threat of losing Bayer’s BBB rating by eliminating the company’s hefty dividend which preserved about $2.4 billion last year. Debt was reduced from 2023’s level of $45 billion and is now on par with 2018 levels. Management is keen to reduce the debt further.

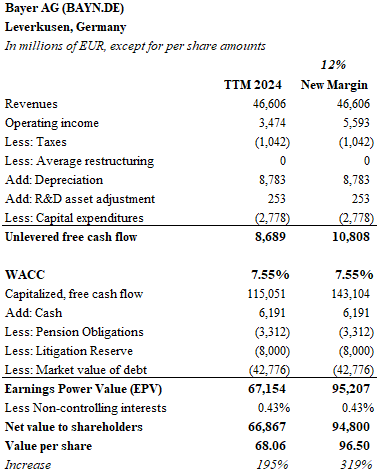

I decided to value Bayer using the preferred tool in Bruce Greenwald’s kit – a calculation of earnings power value (EPV) by taking normalized and unlevered free cash flow and dividing it by a percentage rate which reflects the company’s cost of capital. Using 2024 numbers, I calculated Bayer’s intrinsic value to be approximately €68 per share, or nearly three times its current trading price.

There are three items of note: First, I capitalized Bayer’s annual R&D spending which has hovered between €5 and €7 billion per year. The adjustment adds about €250 million to the annual income. Second, I made the computation of the weighted average cost of capital with a sledgehammer rather than a scalpel. Debt is fairly straightforward. As a BBB rated company, Bayer can borrow at 5.7% in the US market. I chose the US risk-free rate rather than the German bund rate that is about 150 basis points lower. For the equity (35% weight), I employed a 10% risk premium over our 10-Year rate, for 14.3%. The WACC, therefore, computes to 7.55%. Third, I deducted €8 billion from the value as a litigation reserve for future RoundUp claims.

Unlevered free cash flow of €8.7 billion is thus capitalized to €115 billion. Subtract net debt of €36.6 billion, pension obligations of €3.3 billion and the aforementioned litigation reserve, and the net value sums to €66.9 billion after a small adjustment for noncontrolling interests. The resulting share price of €68 gives an investor a very wide margin of safety.

Next, I made an assumption that Anderson and Co. can improve margins. Even if they rise to just 12%, still well below the recent past, it produces an additional €2.2 billion of operating cash. This boosts the share price above €96. One may quickly rebut my thesis by pointing out that the company very well may need every scrap of operating leverage if the Xarelto decline is more precipitous than expected, or the drug pipeline runneth dry.

The next exercise is to break down what a split-up Bayer might look like. Here’s a preview: The Crop Science business had an adjusted EBITDA of $4.3 billion in 2024. Corteva, spun off from DuPont in 2019 has a market cap of $41.5 billion and an EV/EBITDA multiple of 15. Even a 12 multiple would value Bayer’s agriculture division at €51.6 billion. Something to ponder.

Litigation is no way to run a business. If an investment thesis relies on a favorable ruling from the Supreme Court, you’re already on shaky ground. But Monsanto’s RoundUp isn’t like tobacco. It’s not a leisure product. RoundUp is an essential tool for the farming industry. Glyphosate is so effective, many farmers fear that it may disappear from the market and lead to replacement by cheap knock-offs from China which are likely to be unregulated and riskier to one’s health. RoundUp is not going away.

Things are looking better in Leverkusen. Even their fußball team, Bayer Leverkusen won the Bundesliga in 2024. It’s the first time a team other than Bayern Munich or Dortmund won since 2008. So, they’ve got that going for them, which is nice.

Hat tip to my friend Guillermo who hails from Vigo, Spain and put me onto the Bayer value story. Until next time.

DISCLAIMER

The information provided in this article is based on the opinions of the author after reviewing publicly available press reports and SEC filings. The author makes no representations or warranties as to accuracy of the content provided. This is not investment advice. You should perform your own due diligence before making any investments.