Find me in the club with a bottle full of bub

I was in a couple of clubs this past week. Let’s start with the fun club. The Irish band Fontaines DC played a sold-out Slowdown on Saturday night. The band went on at 9 and I almost missed the opener. Maybe they saw the prevalence of white males over the age of 40 and reckoned it would need to be an early bedtime. This is a Grammy-nominated group of guys in their 20’s touring in support of their fourth album, so we’re not talking Van Morrison here. Where were all the kids? It made me think of the recent article with the hypothesis that rock and roll died with Kurt Cobain. This is a pretty dramatic take on the music industry, but I think a lot of youngsters are gravitating towards hip-hop and EDM where most of the sonic barriers are being broken.

You could hear the appeal to an older set: Carlos O’Connor has the guitar stylings of a Jonny Greenwood, and listeners of a certain vintage surely hear echoes of Nirvana, The Pixies, The Church, The Cure and even Weezer in the mix. Grian Chatten has an impressive vocal range and his cadence can sound almost like a Dublinesque Eminem at times. Maybe it’s the cyncial nature of the songs. After all, the band’s most powerful track “I Love You” has a chorus of “Say it to the man who profits, and the bastard walks by.” Jaded stuff. Excellent music, nonetheless.

Dublin rockers would sneer at the other club I visited last week. Jim Grant held his annual conference in New York, and I decided I wanted to see some different rock stars: Stan Druckenmiller on slide guitar and Bill Ackman on drums. Druckenmiller got the most headlines when he said that his old boss, George Soros, would be a little disappointed that he hadn’t committed more capital to his high-conviction trade: Short the long end of the yield curve. In a country running peacetime deficits of roughly 7-8% of GDP where neither presidential candidate has made a peep about a balanced budget, a long duration Treasury has much to blush at. Toss in a recession and war, and you have real downside risk holding anything longer than two-year paper. He was also firm is his belief that no foreigners were safe investing in a China controlled by Xi Jinping, despite David Tepper’s recent optimism.

I was most intrigued by Boaz Weinstein’s presentation. This chess prodigy was a Deutsche Bank managing director at 27. His firm, Saba Capital, has targeted the closed-end fund universe where wide discounts to underlying net asset values can persist for a long time. Saba has pressured some managers to narrow the discounts by taking large positions in the funds and gaining sufficient board control to advocate buying back shares or liquidating altogether.

Weinstein was particularly vocal about his legal brushes with BlackRock. The battles with the asset management behemoth have been contentious (and expensive), and it was slightly appalling to hear about the lengths BlackRock would go to suppress actions that could benefit widows and orphans trapped in underperforming closed-end vehicles. Saba’s Closed-End Funds ETF trades a with the ticker CEFS and has a current distribution rate of 7.62%. There’s limited downside, and you get to earn a nice yield while you let Mr. Weinstein work his craft. Seems like a good club.

Michael Green’s presentation on the distortion of passive vehicles in the market was compelling, but I couldn’t help but think he was preaching to the choir. I invite you to read his thought-provoking pieces. His point has validity: The concentration of market capitalization in the biggest stocks is increasingly reinforced by the automated passive funds which allocate towards a market-cap weighted index. Passive funds have made a mockery of most performances of the managers in the audience, however, and I had a feeling that Larry Fink was sitting down at Hudson Yards watching the proceedings remotely with a smile on his face.

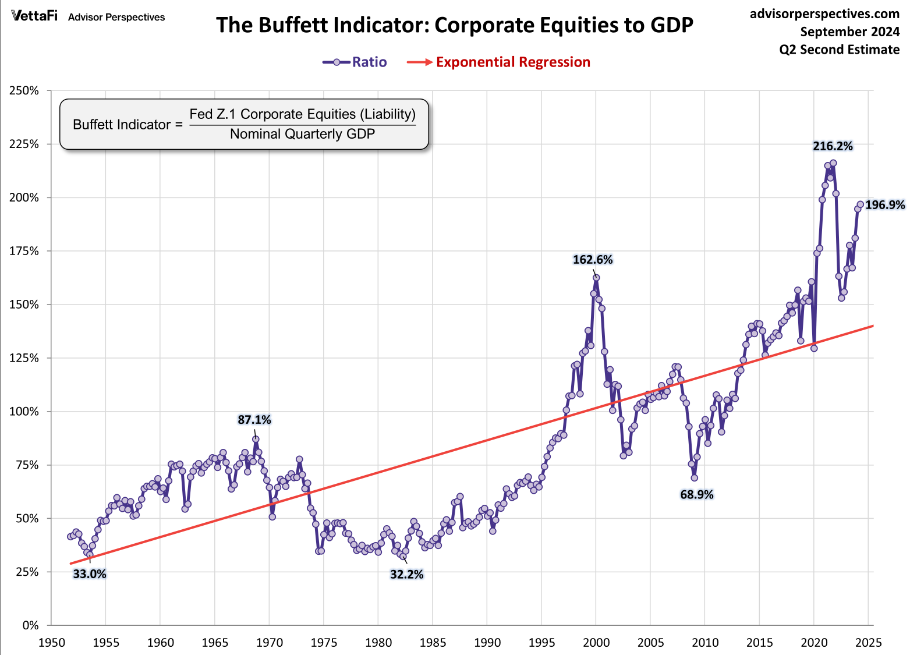

I can tell you who is not in the club: Warren Buffett. The man is sitting on nearly $300 billion of cash. Sure, he could be hedging the likely increase in capital gains taxes should the Democrats take control. He could be getting his “affairs in order,” as they say. But for a guy who famously says you shouldn’t time the market, it feels an awful lot like market timing to me. I offer the chart from Jennifer Nash at Advisor Perspectives:

Corporate equities as a percentage of GDP have rarely been so high. The Fed is cutting rates into an environment of very loose financial conditions. What could go wrong?

So where are the clubs that I want to hang? I mentioned Saba’s ETF above. A few weeks ago, I talked about relative value at Peakstone Realty Trust (PKST) and the ethanol producer REX American Resources (REX). Sam Zell’s (RIP) Equity Commonwealth has a no-brainer preferred yielding north of 6%. I’m supposed to hang out in the real estate club, but developing apartments at a 6.5% return on cost with a looming oversupply of units at rents that need to be 30% higher than pandemic era prices seems like an unfriendly wager.

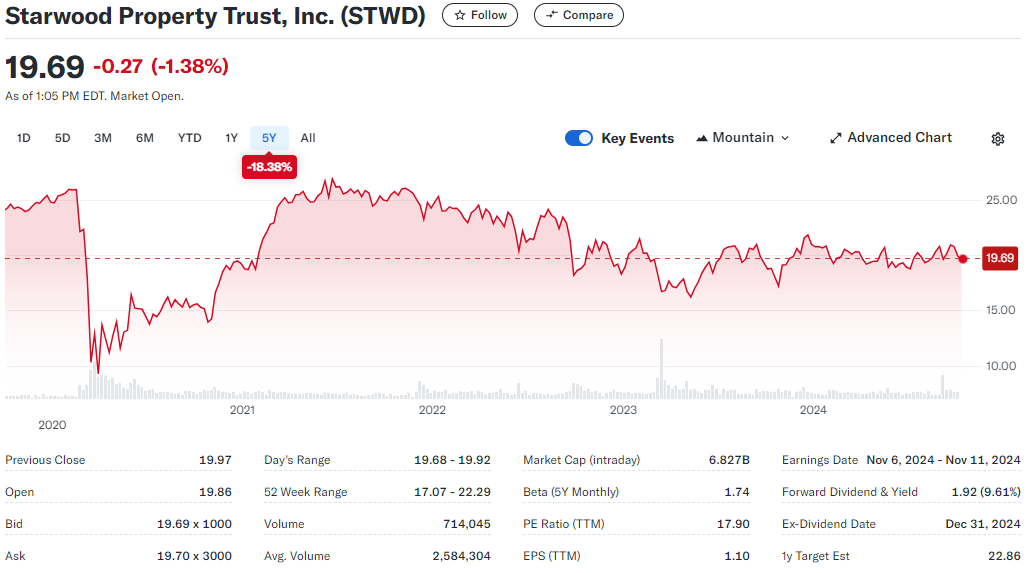

I’d rather hang out with Barry Sternlicht. He can often be found on CNBC lately crying the blues and talking his book, but the guy is a legend. Starwood will probably have some messes to clean up, but they will also seize opportunities to profit from distress. Meanwhile you can hold STWD at a 9.5% dividend yield with the best capital allocators in the business. It makes illiquid and highly leveraged suburban Omaha apartments seem like a visit to the yearbook club after school. Anchored to old memories, the club is far too optimistic that the good times will return. Go to the reunion in 30 years and see what decades of high leverage and “equity” subordinated to a 9% preference can do to a guy. It ain’t pretty.

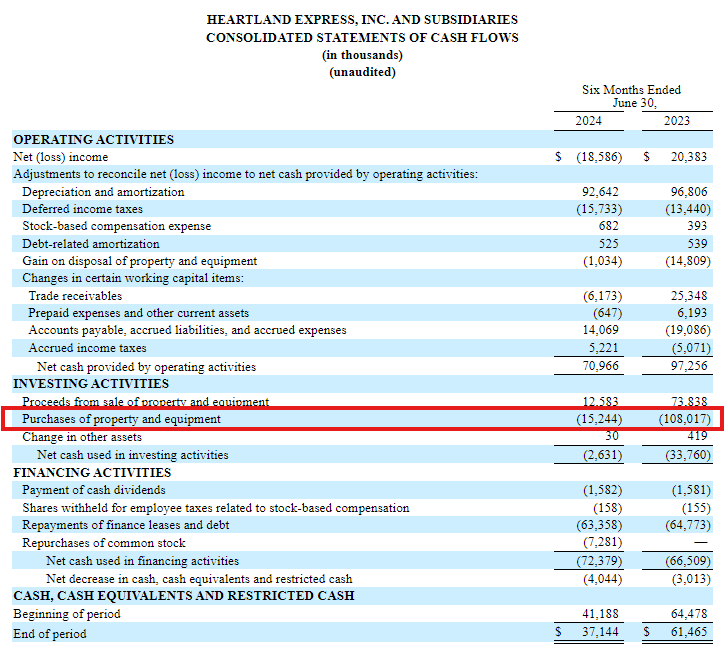

I tried to get interested in Heartland Express trucking (HTLD) recently. The company’s stock has seen a lot of insider buying in recent months. I can make an argument that HTLD is selling at a discount to its intrinsic value. It trades at an EBITDA multiple of about 7x. If you figure free cash flow can hit $115 million in 2024 during a freight recession, then there should be a lot of upside. The recent market cap is around $900 million for a company that could be worth $1.2 billion.

My enthusiasm waned quite a bit when I noticed that much of the aforementioned cash flow came from a lack of investment in trucks. Heartland depreciated nearly $100 million of its vehicles in the first six months of 2024, but only invested about $3 million (net) in new trucks. By comparison, local company Werner Enterprises depreciated $146 million of vehicles during the first six months of 2024 and reinvested a net $118 million in new equipment. The freight market is probably recovering, but it will take a lot of capital for Heartland to modernize its fleet. This one’s a pass for me.

I’m working on a write up for Welltower (WELL). I mentioned it several weeks ago as a very expensive stock with slightly dubious amounts of asset churn. There is a lack of a clear strategy with medical office buildings paired with B-quality senior living assets. The company is a REIT and yields a sub-par 2.2%. The stock has risen 54% over the past 12 months and trades hands at a $76 billion market cap. It strikes me as absurdly overvalued and is my strongest candidate for a short position. You can talk all you want about favorable demographics, but the earnings are weak and the operating costs are not improving as more states impose minimum staffing requirements. Medicare reimbursements are dropping and the company is highly levered.

Until next time.

Appendix: Heartland Trucking income statement and return on capital.