3rd Quarter Apartment REIT Review

“Grief is nature’s most powerful aphrodisiac” – Chazz Reinhold (Will Ferrell), Wedding Crashers (2005).

Back in 2005, I watched in disbelief while apartment leases were being broken left and right as residents began to purchase homes at a frenzied pace. While the economy boomed, the apartment industry suffered. Now, some have begun to whisper about the formation of a new bubble stimulated by the zero-rate environment established by the Federal Reserve to prop up an economy battered by the pandemic. In a surreal world where low wage service workers struggle to pay rent, more affluent renters have the sugar rush of cheap money to feed a new home-buying surge. Throw in a desire for more space to work from home and host dinner guests in the backyard, and buying a house… well, as Owen Wilson would say, “just, wow”.

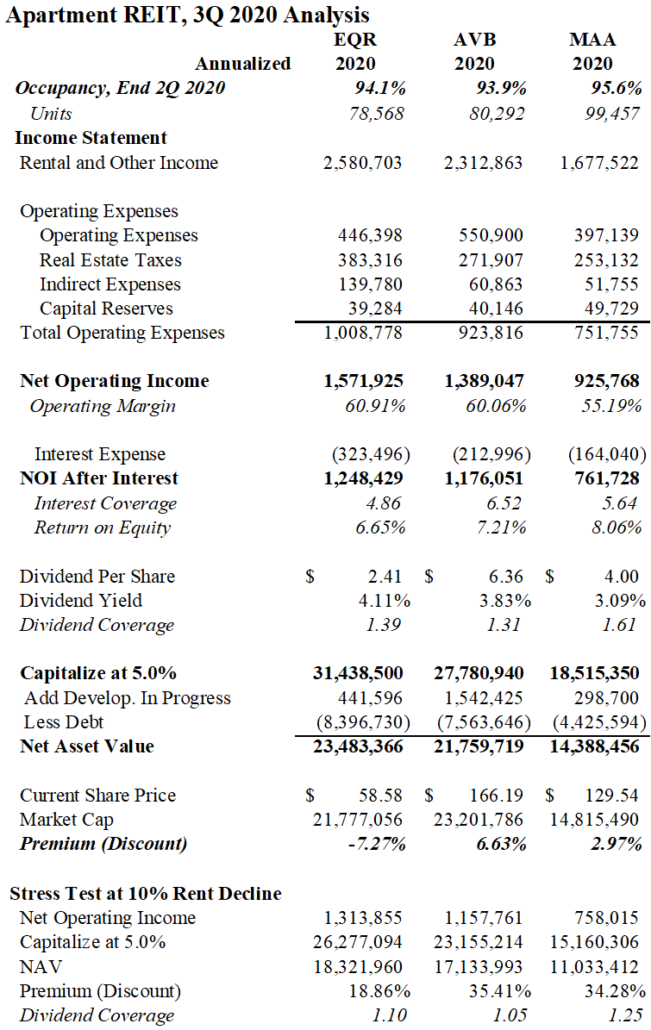

Back in August (which was eight months ago in pandemic time), I decided to look at quarterly results from publicly traded apartment owners to gain insights into where the market was heading. Third quarter results have been posted, so I revisited three of the biggest apartment real estate investment trusts: Equity Residential (EQR), AvalonBay (AVB) and Mid-America Apartment Communities (MAA).

The stocks have continued to trade at discounts to their March peaks and their dividend yields exceed 3%. The announcement of a vaccine breakthrough earlier this week sent the stock prices higher by 10%. The recent price increases have largely erased the deep discounts to net asset values, but they remain attractive as liquid income-producing investments. Their dividends are well-funded, leverage is manageable, and it is hard to envision further downside. EQR is the riskiest of the three because of the company’s high exposure to struggling urban markets, but MAA remains the star of the group due to its focus on sunbelt cities.

The attached article contains brief comments on the quarterly results, a numerical comparison of income and asset values as well as a back-of-the-envelope “stress test” to determine the safety of the dividend payments. Finally, I offer a few observations on the Omaha market where home purchases have caused increased turnover and vacancy.

Sunbelt Success Continues

Mid-America exhibits the divergence in the apartment industry: urban coastal cities are losing residents and many are relocating to dynamic growth centers in the south. As they had in August, executives exuded confidence in their quarterly call. Occupancy exceeded 96% and traffic was positive. Rent growth was muted due to increasing supply and competition from home purchases but remained positive. MAA is a standout performer because of its concentration in sunbelt cities throughout the southeast and Texas. The stock has nearly recovered its losses for the year.

Suburban vs. Urban

AvalonBay and Equity Residential noted positive leasing trends during October but reported that rent declines and move-outs exceeded expectations in urban markets, particularly Manhattan, Boston, and San Francisco. Rent declines surpassed 10% in big coastal cities. Occupancy dropped below 90% in central San Francisco – a stunning figure. Meanwhile suburban properties performed well. Overall occupancy at both firms was at the 94% level. At AvalonBay, rents declined 6% for the quarter on a year-over-year basis and 2% on a sequential quarterly basis. At EQR, rents declined 7.5% for the quarter on a year-over-year basis and 2.7% on a sequential quarterly basis. Collections remained strong – above 97%, but turnover increased. There were some glimmers of hope in the New York City core where major rent discounts and incentives have enticed bargain-hunters to seek upgrades within the market.

Similar Trends in Omaha

In large measure, the observations made by the leading apartment executives on their earnings calls mirror our experience in Omaha. Occupancy levels which had been above 95% for the past two years have fallen dramatically over the past 90 days – approaching 93% in many areas of the city. Effective occupancy may be even lower as one month of free rent has become a common incentive.

Home Purchases Pressure the Top End

The top end of the Omaha apartment market has been hammered by an acceleration of home-buying. Low interest rates are spurring a race to purchase houses despite rising costs amid a tight inventory and expensive lumber prices. There is a 2005-feel to the environment with a high number of lease-breaks. It has not reached a mania level, but loose credit has allowed buyers to emerge who probably wouldn’t have qualified for a mortgage at the beginning of the year. In certain submarkets, added new apartment supply is also depressing the leasing environment.

More Space

All three firms have noted an increase in demand for larger apartments as working from home seems to have spurred a choice for bigger apartments. Studios are difficult to rent across the country, and Omaha is no exception. EQR reported that many of their Manhattan buildings have experienced transfers to larger units within the same property.

Students and Lower-Income Challenges

EQR and AVB reported serious challenges in their Boston and Cambridge properties due to a lack of students in the area. Omaha is no different. Although UNO has strong enrollment figures, many have opted to remain at parents’ homes. International students are a major driver of central Omaha apartment demand, and they have not returned. Rent delinquencies had vanished over the summer, but have made a growing re-appearance as stimulus payments have been exhausted. Workers in the service sector are seeking assistance once again. Delinquencies are not catastrophic – probably running 1%-2% higher – but the trend is worrying.

Stress Test

Last quarter, I used a hypothetical 5% income decline to determine whether the firms could continue to fund their distributions. I increased the pressure to 10% this time around. The dividends appear safe but would certainly come close to being curtailed in such a scenario. It should be noted that the 10% reduction of rental income was taken from an annualized rental figure that already incorporates two quarters of rental declines. The annualized figures are simply the aggregation of results through September 30, 2020 plus an assumption that 4th quarter results will match those of the 3rd quarter.

Note: This article contains the opinions and observations of the author. No investment recommendations are being provided and no representations are made to the accuracy of the content provided.

Bert Hancock

November 12, 2020

nitro bahis giriş güncel

The digital drugstore features a broad selection of medications at affordable prices.

You can find both prescription and over-the-counter drugs suitable for different health conditions.

We strive to maintain high-quality products without breaking the bank.

Quick and dependable delivery guarantees that your medication gets to you quickly.

Take advantage of getting your meds on our platform.

https://www.podchaser.com/podcasts/the-journey-of-cenforce-100-5681357/episodes/cenforce-100-a-reflection-of-p-206226502

The digital drugstore features a broad selection of pharmaceuticals with competitive pricing.

Customers can discover all types of remedies to meet your health needs.

We work hard to offer safe and effective medications while saving you money.

Quick and dependable delivery provides that your medication gets to you quickly.

Take advantage of shopping online with us.

https://podcasters.spotify.com/pod/show/alexandr5704

https://lioleo.edu.vn/christmas-section/4.png.php?id=bet-kosaka

Na [522bet](https://522-bet-br.com), você encontra uma grande variedade de jogos de apostas populares, todos em uma plataforma justa e confiável. E para garantir que sua experiência seja ainda mais emocionante, a plataforma oferece bônus exclusivos para dar mais chances de ganhar.

https://api.lioleo.edu.vn/public/images/skills/4.png.php?id=216-bet

A [flames bet](https://flamesbet-br.com) combina jogos de cassino populares com um ambiente de apostas justo e seguro. A plataforma oferece bônus generosos para que você tenha mais chances de ganhar enquanto se diverte. Aproveite a combinação perfeita entre justiça, emoção e recompensas!

Ganhe um bônus de US$ 100 para jogar na [marjack bet](https://marjackbet-br.com) assim que se registrar! Essa oferta é exclusiva para novos usuários e é uma excelente maneira de começar sua experiência com um incentivo para explorar os jogos de cassino. Cadastre-se hoje e aproveite ao máximo!

Baixe o aplicativo pixbet e experimente uma navegação otimizada para uma experiência de jogo única. A plataforma foi projetada para ser fácil de usar, com uma interface intuitiva que permite realizar apostas rapidamente, sem perder qualidade no jogo.

สำหรับผู้ใช้ใหม่ที่ทำการลงทะเบียน [url=https://sexy-778.com]sexy[/url] ยังมีโบนัสต้อนรับที่น่าสนใจเพื่อเพิ่มโอกาสในการชนะการเดิมพัน โบนัสนี้จะช่วยให้ผู้เล่นมีเครดิตเพิ่มเติมในการเล่นเกมต่างๆ ซึ่งสามารถนำไปใช้เดิมพันได้ตามต้องการ การรับโบนัสนี้เป็นวิธีที่ดีในการเริ่มต้นเล่นเกมและเพิ่มความสนุกสนานในการเข้าร่วมกิจกรรมต่างๆ ที่เว็บไซต์ [url=https://sexy-778.com]sexy[/url] มีให้

Na [misterjackbet](https://misterjackbet-br.com), Jogos Populares de Azar e Bônus Irresistíveis Te Esperam – Venha Conferir!

Your Questions Answered Anytime: sherbet – https://sherbet-ph.com Offers 24/7 Customer Support

The Stake Casino gameathlon.gr is one of the leading crypto gambling as it was one of the pioneers.

The online casino market is growing rapidly and there are many options, however, not all of them provide the same quality of service.

In this article, we will review the best casinos accessible in Greece and the benefits they offer who live in Greece.

The best-rated casinos this year are shown in the table below. The following are the best casino websites as rated by our expert team.

For every casino, it is important to check the licensing, security certificates, and data protection measures to ensure safety for users on their websites.

If any of these elements are missing, or if it’s hard to verify them, we exclude that website from our list.

Casino software developers also play a major role in choosing an gaming platform. Typically, if the previous factor is missing, you won’t find reputable gaming companies like Play’n Go represented on the site.

Top-rated online casinos offer classic payment methods like Visa, but they should also include electronic payment methods like PayPal and many others.

24/7 Availability for Your Queries: casumo – https://casumo-in.com’s Professional Customer Service

The following time I review a blog, I really hope that it does not dissatisfy me as high as this set. I mean, I recognize it was my choice to review, yet I really assumed youd have something interesting to state. All I hear is a lot of yawping concerning something that you might deal with if you werent as well hectic searching for attention. Francisco Rava

The GameAthlon platform is a popular gaming site offering dynamic gameplay for gamblers of all preferences.

The site features a extensive collection of slots, real-time games, classic casino games, and sports betting.

Players have access to fast navigation, top-notch visuals, and intuitive interfaces on both PC and tablets.

gameathlon casino

GameAthlon focuses on safe gaming by offering encrypted transactions and transparent outcomes.

Reward programs and VIP perks are regularly updated, giving registered users extra chances to win and enjoy the game.

The helpdesk is ready day and night, supporting with any inquiries quickly and efficiently.

GameAthlon is the top destination for those looking for an adrenaline rush and huge prizes in one trusted space.

I appreciate the level of detail in this post. It really helped me get a better understanding of the subject.

ติดตั้งแอป z1688 – https://zaav7.com แล้วรับการแจ้งเตือนแมตช์สำคัญ โปรโมชั่นพิเศษ และข่าวสารก่อนใคร

เดิมพันกับ l86 – https://l86-th.com ได้ง่ายยิ่งขึ้น พร้อมเกมสล็อตและโต๊ะคาสิโนแนว Sci-Fi ที่ได้รับแรงบันดาลใจจาก Starfield และ Mass Effect พบกับกราฟิกสุดล้ำ และโบนัสแจ็คพอตที่ให้คุณลุ้นรางวัลใหญ่เหมือนอยู่ในโลกอนาคต

เดิมพันกับ u318 – https://hdis5.com ได้ง่ายยิ่งขึ้น พร้อมเกมสล็อตและโต๊ะคาสิโนแนว Sci-Fi ที่ได้รับแรงบันดาลใจจาก Starfield และ Mass Effect

Hỗ Trợ Khách Hàng Tại kubet – https://kubet-vn.com – Trực Tuyến 24/7, Giải Quyết Nhanh

ดาวน์โหลดแอป ทางเข้าw69 – https://zrs12.com ง่ายๆ เพียงไม่กี่คลิก สนุกกับการเดิมพันกีฬา คาสิโน และสล็อตในที่เดียว

A [betpix](https://betpix-88.com) Oferece Bônus Atraentes e Jogos Populares Que Você Vai Adorar

Hmm it seems like your website ate my first comment (it was super long) so I guess

I’ll just sum it up what I submitted and say, I’m thoroughly enjoying

your blog. I as well am an aspiring blog blogger but I’m still new to everything.

Do you have any tips and hints for newbie blog writers? I’d really appreciate it.

Aproveite os Jogos Populares e Bônus Generosos da [greenbets](https://www.greenbets-br.com) Agora Mesmo!

Enjoy uninterrupted gaming at taya777 slot – https://taya777-slot-ph.com, where our professional customer service team is available around the clock. We understand the importance of quick and reliable support, so we’re committed to providing fast resolutions to any issues you may face. Whether it’s questions about promotions, account management, or payment options, our 24/7 customer service team is always available to assist you.

New to 22bet – https://22bet-in.com? Register Now and Receive a $100 Bonus!

สมัครสมาชิก hp888 – https://hp888-th.com วันนี้ รับโบนัส 100$ ไปเดิมพันฟรี

ความสะดวกสบายในการติดต่อบริการลูกค้า 24 ชั่วโมงทำให้ pxj เป็นแพลตฟอร์มที่ได้รับความไว้วางใจจากผู้เล่นจำนวนมาก ทั้งในไทยและต่างประเทศ เพราะไม่เพียงแต่การเล่นที่สนุกสนาน แต่ยังมีการบริการที่ตอบโจทย์ทุกความต้องการของผู้เล่นอย่างครบวงจร

Na marjack bet, Você Joga os Melhores Jogos Populares com Grandes Oportunidades de Bônus

Download the slotv App for Faster Access to Your Favorite Casino Games

Ensure Quick Withdrawals at betshah: What Documents Are Required?

w69 วันนี้ รับโปรโมชั่นพิเศษมากมาย

ใช้งานสะดวก ปลอดภัย และรองรับทุกอุปกรณ์

ดาวน์โหลดแอป w69com

วันนี้ รับโปรโมชั่นพิเศษมากมาย ใช้งานสะดวก ปลอดภัย และรองรับทุกอุปกรณ์

w69 login – https://ukef2.com ปรับปรุงฟังก์ชันแอปใหม่

ใช้งานง่ายกว่าเดิม สนุกกับคาสิโนสดและเกมสล็อตได้ทุกที่ทุกเวลา

ดาวน์โหลดแอป w69 betวันนี้ รับโปรโมชั่นพิเศษมากมาย ใช้งานสะดวก

ปลอดภัย และรองรับทุกอุปกรณ์

เพลิดเพลินกับเกมคาสิโนออนไลน์ในแอป rm688 – https://ygic4.com ที่มาพร้อมระบบภาพและเสียงระดับ HD เพื่อประสบการณ์ที่เหนือกว่า

เพลิดเพลินกับเกมคาสิโนออนไลน์ในแอป

w69 ทางเข้า – https://rwho3.com ที่มาพร้อมระบบภาพและเสียงระดับ HD เพื่อประสบการณ์ที่เหนือกว่า

Прохождение сертификации в нашей стране является ключевым этапом легальной реализации товаров.

Процедура подтверждения качества подтверждает полное соответствие нормам и официальным требованиям, что, в свою очередь, гарантирует защиту покупателей от некачественных товаров.

сертификация

К тому же, наличие сертификатов способствует деловые отношения с партнерами и открывает возможности на рынке.

Без сертификации, возможны юридические риски и сложности при ведении бизнеса.

Вот почему, официальное подтверждение качества не только требованием законодательства, но и важным фактором устойчивого роста организации на отечественном рынке.

ใช้แอป สล็อตw69 – https://ukil3.com เพื่อเดิมพันได้ทุกที่ทุกเวลา รองรับทั้งสมาร์ทโฟนและแท็บเล็ต

Join patti Today and Receive

a $100 Bonus Just for Registering!

Cadastro Rápido no onabet – https://onabet-88.com e 100$

de Bônus de Boas-Vindas!

Cách Đăng Ký ibet888 Để Nhận Thưởng 100$ Nhanh Chóng

Что такое BlackSprut?

Сервис BlackSprut привлекает интерес многих пользователей. Почему о нем говорят?

Эта площадка предоставляет разнообразные функции для аудитории. Интерфейс платформы отличается удобством, что делает платформу доступной без сложного обучения.

Стоит учитывать, что этот ресурс обладает уникальными характеристиками, которые отличают его на рынке.

При рассмотрении BlackSprut важно учитывать, что различные сообщества имеют разные мнения о нем. Некоторые отмечают его функциональность, другие же относятся к нему более критично.

В целом, BlackSprut остается объектом интереса и привлекает интерес разных слоев интернет-сообщества.

Рабочее зеркало к БлэкСпрут – проверьте здесь

Если нужен актуальный сайт BlackSprut, то вы по адресу.

bs2best

Сайт часто обновляет адреса, и лучше знать обновленный домен.

Мы мониторим за актуальными доменами и готовы предоставить актуальным линком.

Посмотрите рабочую версию сайта прямо сейчас!

อินเทอร์เฟซใหม่ของแอป w69 asia ช่วยให้การนำทางลื่นไหลขึ้น ไม่ต้องเสียเวลาค้นหาเกมโปรดของคุณ

w69 android app ปรับปรุงฟังก์ชันแอปใหม่ ใช้งานง่ายกว่าเดิม สนุกกับคาสิโนสดและเกมสล็อตได้ทุกที่ทุกเวลา

ดาวน์โหลดแอป w69 เครดิตฟรี 188 – https://avf05.com ได้ง่ายๆ เพียงไม่กี่ขั้นตอน พร้อมรับโบนัสต้อนรับ

100$ สนุกกับการเดิมพันที่ดีที่สุดบนมือถือ

ดาวน์โหลดแอป w69oi แล้วสนุกกับสล็อต แจ็คพอตแตกง่าย และอัตราจ่ายที่ดีที่สุด

ติดตั้งแอป w69 vvip แล้วรับการแจ้งเตือนแมตช์สำคัญ โปรโมชั่นพิเศษ และข่าวสารก่อนใคร

ดาวน์โหลดแอป w69เข้าสู่ระบบ แล้วสนุกกับสล็อต แจ็คพอตแตกง่าย และอัตราจ่ายที่ดีที่สุด

w69 casino login พัฒนาแอปให้รองรับเกมมากขึ้น มีตัวเลือกหลากหลายให้คุณเดิมพันได้อย่างอิสระ

ดาวน์โหลดแอป w69 ทางเข้า พร้อมรับโบนัสพิเศษเฉพาะผู้ใช้มือถือ สนุกได้ทุกเวลา

Buying medicine from e-pharmacies can be much easier than shopping in person.

No need to wait in line or stress over closing times.

Internet drugstores allow you to order your medications with just a few clicks.

A lot of digital pharmacies have discounts in contrast to physical stores.

https://eccentrictirade.com/forums/showthread.php?tid=135404

Additionally, it’s easy to check different brands quickly.

Quick delivery means you get what you need fast.

Do you prefer ordering from e-pharmacies?

http://site2.aesa.pb.gov.br/aesa/Cities/?id=google-bet

http://magdalenahoffmann.com/br/index.php?id=cukong-bet

http://sila-zerna.com/br/index.php?id=sersan-bet

365-bet-link

bet-6d

http://xn--l1acbdfo1f.xn--p1ai/br/index.php?id=indra-bet

bukit-bet

http://mail.crn-nieruchomosci.pl/br/index.php?id=yoman-bet

taring-bet

buy kick viewers

http://sila-zerna.com/br/index.php?id=limpul-bet

https://gvis.tramandai.rs.gov.br/web-console/Lifestyle/?id=merah-bet

http://hornoscasaemilio-valoriani.com/br/index.php?id=fg-bet-slot

ดาวน์โหลดแอป w69 slot ทาง เข้า แล้วเล่นคาสิโนสดพร้อมกับเกมสล็อตธีมแนว Monster Hunter และ Diablo รับรางวัลพิเศษทุกวัน

พร้อมกิจกรรมพิเศษที่แจกโบนัสฟรีสำหรับผู้เล่นที่เข้าร่วมล่ามอนสเตอร์

https://gvis.tramandai.rs.gov.br/web-console/Cities/?id=king-bet-88

แอป w69 slot รองรับการเล่นหลายหน้าจอ ให้คุณสนุกกับการเดิมพันได้หลากหลายพร้อมกัน

http://pribehyfotek.cz/br/index.php?id=naga-bet

11w-bet-slot

w69 slot thailand – https://tvbm6.com อัปเดตแอปใหม่ให้รองรับการเดิมพันแบบเรียลไทม์ เชียร์ทีมโปรดของคุณได้แบบไม่มีสะดุด

http://sila-zerna.com/br/index.php?id=sule-bet

Buying medications from e-pharmacies has become way easier than going to a physical pharmacy.

There’s no reason to deal with crowds or think about closing times.

Online pharmacies allow you to get your medications without leaving your house.

Many digital pharmacies provide discounts compared to physical stores.

http://old.pokvesti.ru/forum/viewtopic.php?f=42&t=433187&p=1222683#p1222683

Additionally, you can check alternative medications easily.

Fast shipping makes it even more convenient.

Have you tried ordering from e-pharmacies?

http://xn--l1acbdfo1f.xn--p1ai/br/index.php?id=bet-win

Любители азартных игр всегда найдут зеркальное альтернативный адрес казино Чемпион и наслаждаться любимыми слотами.

В казино доступны разнообразные слоты, включая классические, и самые свежие игры от ведущих производителей.

Если главный ресурс не работает, рабочее зеркало Champion позволит обойти ограничения и продолжить игру.

чемпион слоты

Все функции полностью работают, включая открытие профиля, финансовые операции, а также бонусы.

Используйте обновленную ссылку, и наслаждаться игрой без блокировок!

türkçe altyazılı porno

Nanomedicine targets diseases microscopically. The iMedix Medical podcast explores this frontier technology. Researchers explain cancer-fighting “smart particles”. The extremely small could make enormous differences—learn how with iMedix health care!

Rare diseases collectively affect many people, requiring specialized knowledge. Understanding the challenges in diagnosing and treating rare conditions builds empathy. Learning about patient advocacy groups provides resources and support. Familiarity with medical preparations developed specifically for rare diseases is relevant. Knowing about orphan drug development highlights unique research paths. Finding reliable information sources is crucial for affected families. The iMedix podcast covers a wide range of conditions, including less common ones. As a medical podcast, it aims to shed light on diverse health challenges. Explore the iMedix best podcasts for comprehensive medical discussions. iMedix provides trusted health advice across the spectrum of conditions.

Taking one’s own life is a complex issue that affects millions of people worldwide.

It is often linked to emotional pain, such as anxiety, hopelessness, or chemical dependency.

People who contemplate suicide may feel isolated and believe there’s no other way out.

how-to-kill-yourself.com

Society needs to raise awareness about this subject and help vulnerable individuals.

Mental health care can make a difference, and reaching out is a crucial first step.

If you or someone you know is thinking about suicide, please seek help.

You are not without options, and help is available.

http://hydraulik-tuchola.pl/br/index.php?id=55k-bet

Здесь вам открывается шанс наслаждаться широким ассортиментом слотов.

Игровые автоматы характеризуются яркой графикой и интерактивным игровым процессом.

Каждая игра даёт особые бонусные возможности, улучшающие шансы на успех.

1xbet казино

Слоты созданы для игроков всех уровней.

Вы можете играть бесплатно, а затем перейти к игре на реальные деньги.

Испытайте удачу и насладитесь неповторимой атмосферой игровых автоматов.

http://mail.crn-nieruchomosci.pl/br/index.php?id=piston-bet

http://magdalenahoffmann.com/br/index.php?id=cakar-bet

На нашем портале вам предоставляется возможность наслаждаться большим выбором игровых слотов.

Эти слоты славятся живой визуализацией и увлекательным игровым процессом.

Каждый игровой автомат предоставляет уникальные бонусные раунды, повышающие вероятность победы.

1win games

Игра в слоты подходит игроков всех уровней.

Вы можете играть бесплатно, после чего начать играть на реальные деньги.

Испытайте удачу и насладитесь неповторимой атмосферой игровых автоматов.

На нашей платформе можно найти популярные слот-автоматы.

Здесь собраны ассортимент слотов от ведущих провайдеров.

Любой автомат обладает интересным геймплеем, бонусными функциями и максимальной волатильностью.

http://www.potthof-engelskirchen.de/out.php?link=https://casinoreg.net

Вы сможете играть в демо-режиме или выигрывать настоящие призы.

Меню и структура ресурса просты и логичны, что помогает легко находить нужные слоты.

Если вы любите азартные игры, данный ресурс стоит посетить.

Попробуйте удачу на сайте — тысячи выигрышей ждут вас!

На нашей платформе можно найти популярные слот-автоматы.

На сайте представлены ассортимент автоматов от топ-разработчиков.

Любой автомат предлагает интересным геймплеем, призовыми раундами и максимальной волатильностью.

http://wartank.ru/?channelId=30152&partnerUrl=casinoreg.net

Каждый посетитель может играть в демо-режиме или играть на деньги.

Меню и структура ресурса просты и логичны, что помогает легко находить нужные слоты.

Если вы любите азартные игры, данный ресурс стоит посетить.

Откройте для себя мир слотов — возможно, именно сегодня вам повезёт!

http://site2.aesa.pb.gov.br/aesa/Cities/?id=google-bet

На данной платформе вы обнаружите интересные слоты казино в казино Champion.

Выбор игр включает традиционные игры и современные слоты с качественной анимацией и уникальными бонусами.

Любая игра разработан для максимального удовольствия как на компьютере, так и на планшетах.

Независимо от опыта, здесь вы найдёте подходящий вариант.

скачать приложение champion

Игры доступны без ограничений и не требуют скачивания.

Кроме того, сайт предоставляет акции и рекомендации, для удобства пользователей.

Попробуйте прямо сейчас и насладитесь азартом с казино Champion!

Здесь вы сможете найти интересные игровые слоты в казино Champion.

Выбор игр представляет традиционные игры и актуальные новинки с захватывающим оформлением и уникальными бонусами.

Каждый слот разработан для удобной игры как на десктопе, так и на мобильных устройствах.

Независимо от опыта, здесь вы обязательно подберёте слот по душе.

скачать приложение

Игры работают круглосуточно и не нуждаются в установке.

Также сайт предусматривает акции и полезную информацию, чтобы сделать игру ещё интереснее.

Погрузитесь в игру уже сегодня и испытайте удачу с казино Champion!

http://hydraulik-tuchola.pl/br/index.php?id=studio-bet

อินเทอร์เฟซใหม่ของแอป w69 slot เครดิตฟรี – https://oii87.com ช่วยให้การนำทางลื่นไหลขึ้น ไม่ต้องเสียเวลาค้นหาเกมโปรดของคุณ

Thank you for the good writeup. It in fact was a amusement account it. Look advanced to far added agreeable from you! However, how can we communicate?

Thank you for the good writeup. It in fact was a amusement account it. Look advanced to more added agreeable from you! By the way, how could we communicate?

Hi there just wanted to give you a quick heads up. The text in your article seem to be running off the screen in Opera. I’m not sure if this is a formatting issue or something to do with browser compatibility but I figured I’d post to let you know. The design and style look great though! Hope you get the problem fixed soon. Many thanks

No moverbet,

novos usuários podem aproveitar um bônus de 100$ ao se registrar no site!

Isso significa mais chances de ganhar e explorar uma grande variedade

de jogos de cassino, desde slots emocionantes até clássicos como roleta e blackjack.

Com o bônus de boas-vindas, você começa com um saldo extra, o que aumenta suas chances de sucesso.

Cadastre-se agora e use os 100$ de bônus para experimentar

seus jogos favoritos com mais facilidade. Aproveite a oferta e

comece sua aventura no cassino agora mesmo!

Сайт BlackSprut — это довольно популярная точек входа в теневом интернете, предоставляющая широкие возможности для всех, кто интересуется сетью.

На платформе предусмотрена удобная навигация, а структура меню понятен даже новичкам.

Пользователи отмечают стабильность работы и постоянные обновления.

bs2best.markets

BlackSprut ориентирован на удобство и минимум лишней информации при использовании.

Тех, кто изучает инфраструктуру darknet, площадка будет интересным вариантом.

Прежде чем начать рекомендуется изучить базовые принципы анонимной сети.

No iribet, novos usuários podem aproveitar um

bônus de 100$ ao se registrar no site! Isso significa mais

chances de ganhar e explorar uma grande variedade de

jogos de cassino, desde slots emocionantes até clássicos como roleta e

blackjack. Com o bônus de boas-vindas, você começa com um saldo extra, o

que aumenta suas chances de sucesso. Cadastre-se agora e use os 100$ de bônus para experimentar seus jogos favoritos com mais facilidade.

Aproveite a oferta e comece sua aventura no cassino agora mesmo!

queens, http://www.queens-br.com,: Cadastre-se

e Ganhe 100$ de Bônus para Apostar!

Receba 100$ ao Criar Sua Conta no brlwin – Bônus

Exclusivo!

Registre-se no bet esporte – https://betesporte-br.com Agora e

Receba 100$ para Suas Apostas!

Bônus de 100$ ao Registrar-se no betobet – Aproveite Agora!

Cadastro Rápido no esportebet – https://esportebet-br.com e 100$ de Bônus de Boas-Vindas!

На данной платформе вы сможете найти интересные онлайн-автоматы в казино Champion.

Выбор игр содержит классические автоматы и актуальные новинки с захватывающим оформлением и разнообразными функциями.

Всякий автомат разработан для комфортного использования как на компьютере, так и на планшетах.

Независимо от опыта, здесь вы обязательно подберёте слот по душе.

champion игровые автоматы

Автоматы доступны без ограничений и не требуют скачивания.

Кроме того, сайт предоставляет бонусы и обзоры игр, чтобы сделать игру ещё интереснее.

Погрузитесь в игру уже сегодня и оцените преимущества с брендом Champion!

No globalbet, novos usuários podem

aproveitar um bônus de 100$ ao se registrar no site! Isso significa mais chances de ganhar e explorar

uma grande variedade de jogos de cassino, desde slots emocionantes

até clássicos como roleta e blackjack. Com o bônus de boas-vindas,

você começa com um saldo extra, o que aumenta suas chances de sucesso.

Cadastre-se agora e use os 100$ de bônus para experimentar

seus jogos favoritos com mais facilidade. Aproveite a oferta e comece sua

aventura no cassino agora mesmo!

Aproveite a oferta exclusiva do juntosbet para

novos usuários e receba 100$ de bônus ao se registrar!

Este bônus de boas-vindas permite que você experimente

uma vasta gama de jogos de cassino online sem precisar gastar imediatamente.

Com o bônus de 100$, você poderá explorar jogos como roleta, blackjack, caça-níqueis e muito

mais, aumentando suas chances de vitória desde o

primeiro minuto. Não perca essa chance única de começar com um valor significativo – cadastre-se agora!

Register on mirax and Start Winning with Your $100 Bonus!

Register for gamdom and receive a

$100 bonus upon signing up! The registration process is quick, and once you log in, your bonus will be credited to your account.

This bonus is available to new users, providing a fantastic way to get started with extra funds.

Don’t wait – sign up today and enjoy your $100 bonus!

Get a $100 Bonus Right After Registering at refuel!

Start with a Bang! $100 Bonus Awaits You at maneki – https://maneki-in.com!

Looking for an online casino with exciting rewards? At oppa888, new users can enjoy a $100 bonus just for registering!

With this bonus, you’ll be able to explore a wide range of games, including slots, poker, blackjack,

and more. Don’t miss out on this exclusive offer—sign up now and claim

your $100 bonus to get your gaming experience off to a fantastic start!

New User? Learn How to Register on yoyo

and Get Your $100 Bonus!

Don’t Wait – Claim Your $100 Bonus Now at winny!

Sign Up Now and Enjoy a $100 Bonus at betobet!

$100 Bonus Available for New Users – Join nyspins Now!

Looking for a great start on nomini?

New users get a $100 bonus when they register! The registration process is quick and easy.

Just fill in your details, log in, and your bonus will

be waiting for you. With your $100 bonus, you’ll be ready to explore the exciting world

of online casinos, from classic slots to live dealer games.

Sign up now and take advantage of this amazing offer!

New Users Get $100 Free at 220patti – https://220patti-in.com – Claim Yours Today!

Get Your $100 Bonus as a New User at nextbet Today!

Join marvel bet Now

and Get Your $100 Registration Bonus!

Join lottoland Today:

Register and Receive a $100 Bonus Immediately!

New to ivibet? Register Now and Get

Your $100 Bonus!

Start Your Winning Streak with a $100 Bonus at goslot!

New Users Get $100 Free at 12bet – Claim Yours Today!

New to amunra? Register Now and Receive a $100 Bonus!

Join the Action with heyspin and Claim Your $100 Registration Bonus!

Sign Up for skol

and Receive a $100 Bonus for New Users

Sign Up Now at dreamz and Get a $100

Bonus Just for Joining

Get a $100 Bonus Right After Registering at mrrex!

New to nobonus? Register Now and Receive

a $100 Bonus!

Get started on pgebet

today and enjoy a $100 bonus upon registration! Signing up is quick and

simple. Just create an account, log in, and you’ll be instantly rewarded with a $100 bonus.

This welcome offer is exclusive to new users, providing a fantastic opportunity

to boost your gaming experience right from the start.

Don’t miss out on this limited-time offer.

Register today, and the bonus will be yours as soon as you complete your sign-up process.

A $100 Bonus is Waiting for You at puma –

Register Now!

Claim Your $100 Bonus with a Quick Registration at rant!

New Users, Register at slotbox

and Get a $100 Welcome Bonus

How to Log In and Claim Your $100 Bonus at 1xslots

Sign up today at casitsu and receive a $100 bonus to start your

journey! Once you register and log in, your $100 bonus

will be credited to your account. This is a fantastic way

to get started with extra funds, allowing you to try out various games.

Register today to take advantage of this exclusive offer and boost your gaming experience

right from the start!

Unlock Your $100 Bonus by Registering on national Today

Get Started on buumi: Easy Registration and $100 Welcome Bonus

How to Register on amon and

Start Playing with $100 Bonus

Sign Up for tsars and Get Your Hands on a $100 Bonus!

Join leon Today:

Register and Receive a $100 Bonus Immediately!

Join 24bet today and enjoy a $100 bonus

just for signing up! This bonus allows you to explore the wide selection of casino games, live dealer tables, and

sports betting opportunities. Register now and claim your $100 bonus to start your gaming adventure on a high

note!

Experience the thrill of winning at rummy with a special $100 bonus

for new users! By signing up, you’ll get access to exciting casino

games, sports betting, and much more. Whether you’re a seasoned player or new to the world of

online casinos, this bonus gives you the opportunity to start

strong. Register today, claim your $100 bonus, and explore a variety of games—all

from the comfort of your home!

No pgwin,

Você Começa com 100$ de Bônus Exclusivo!

This online store offers a wide selection of stylish wall clocks for any space.

You can discover modern and vintage styles to enhance your home.

Each piece is carefully selected for its design quality and accuracy.

Whether you’re decorating a functional kitchen, there’s always a beautiful clock waiting for you.

creative wall clocks

The collection is regularly renewed with exclusive releases.

We prioritize quality packaging, so your order is always in safe hands.

Start your journey to timeless elegance with just a few clicks.

This online store offers a great variety of interior wall clocks for all styles.

You can check out modern and vintage styles to complement your living space.

Each piece is carefully selected for its design quality and durability.

Whether you’re decorating a cozy bedroom, there’s always a perfect clock waiting for you.

best large beach wall clocks

The shop is regularly expanded with trending items.

We care about a smooth experience, so your order is always in trusted service.

Start your journey to better decor with just a few clicks.

This online store offers a large assortment of decorative timepieces for all styles.

You can browse urban and classic styles to match your living space.

Each piece is curated for its aesthetic value and reliable performance.

Whether you’re decorating a creative workspace, there’s always a fitting clock waiting for you.

karlsson little big wall clocks

Our assortment is regularly expanded with fresh designs.

We focus on secure delivery, so your order is always in safe hands.

Start your journey to perfect timing with just a few clicks.

No doce, Você Começa com 100$ de Bônus Exclusivo!

100$ de Bônus para Apostar no pgwin!

Cadastre-se Agora!

O bet7k oferece uma excelente oportunidade para quem deseja

começar sua experiência no cassino online com um bônus

de 100$ para novos jogadores! Ao se registrar no site, você garante esse bônus exclusivo

que pode ser utilizado em diversos jogos de cassino, como slots,

roleta e poker. Esse é o momento perfeito para explorar

o mundo das apostas com um saldo extra, aproveitando ao máximo suas apostas sem precisar investir

um grande valor logo de início. Não perca essa oportunidade e cadastre-se já!

Novo no bwin-789.com – https://bwin-789.com? Cadastre-se

e Receba 100$ de Bônus ao Fazer Login!

Cadastro Rápido no bk bet – https://bk-bet-br.com e 100$ de Bônus de Boas-Vindas!

Comece no fbbet com 100$ de

Bônus de Boas-Vindas!

Receba 100$ ao Criar Sua Conta no leao – Bônus Exclusivo!

Aproveite 100$ de Bônus ao Se Registrar no h2bet – https://h2-bet-br.com – Cadastre-se Já!

No umbet, novos usuários podem aproveitar um bônus de 100$ ao

se registrar no site! Isso significa mais chances de ganhar e explorar uma grande variedade de jogos de cassino, desde slots emocionantes até clássicos como roleta

e blackjack. Com o bônus de boas-vindas, você começa com um saldo extra, o

que aumenta suas chances de sucesso. Cadastre-se agora e use os 100$

de bônus para experimentar seus jogos favoritos com mais facilidade.

Aproveite a oferta e comece sua aventura no cassino agora mesmo!

Bônus de 100$ para Novos Jogadores no 193 bet – Cadastre-se

Agora!

No wazamba, novos usuários podem aproveitar um bônus de 100$ ao se registrar no site!

Isso significa mais chances de ganhar e explorar uma grande variedade de jogos de

cassino, desde slots emocionantes até clássicos como roleta e blackjack.

Com o bônus de boas-vindas, você começa com um saldo extra,

o que aumenta suas chances de sucesso. Cadastre-se agora e use os 100$ de bônus para experimentar seus jogos favoritos com mais facilidade.

Aproveite a oferta e comece sua aventura no cassino agora mesmo!

Aposte no cbet

e Receba 100$ de Bônus ao Se Registrar!

betmotion:

100$ de Bônus para Novos Jogadores – Cadastre-se Já!

Платформа предлагает поиска занятости в Украине.

Вы можете найти актуальные предложения от уверенных партнеров.

На платформе появляются предложения в разных отраслях.

Частичная занятость — решаете сами.

https://my-articles-online.com/

Поиск простой и рассчитан на широкую аудиторию.

Создание профиля не потребует усилий.

Хотите сменить сферу? — начните прямо сейчас.

Đăng ký bet69 ngay hôm nay để nhận 100$ tiền thưởng khi gửi tiền lần đầu.

Chỉ cần vài thao tác đơn giản: nhập thông tin, xác thực và đăng nhập.

Đừng chần chừ – tham gia ngay để không bỏ lỡ ưu đãi

cực khủng này!

Hướng Dẫn Đăng Ký w88 Cho Người Mới

– Đơn Giản, Dễ Dàng

Cách Đăng Ký win2888 An Toàn – Không

Lo Khóa Tài Khoản

Good day! I know this is kind of off topic but I was wondering which blog platform are you using for this site? I’m getting fed up of WordPress because I’ve had problems with hackers and I’m looking at options for another platform. I would be awesome if you could point me in the direction of a good platform.

Hello, just wanted to tell you, I loved this blog post. It was inspiring. Keep on posting!

No Upsports Bet, novos usuários podem

aproveitar um bônus de 100$ ao se registrar no site! Isso significa mais chances de ganhar e explorar uma grande variedade de

jogos de cassino, desde slots emocionantes até clássicos como roleta e blackjack.

Com o bônus de boas-vindas, você começa com um saldo extra,

o que aumenta suas chances de sucesso. Cadastre-se agora e use os 100$

de bônus para experimentar seus jogos favoritos com mais facilidade.

Aproveite a oferta e comece sua aventura no cassino agora mesmo!

100$ de Bônus no roleta online (roletaonline-br.com) para Novos Usuários – Registre-se!

No simplesbet, Cadastre-se e Ganhe 100$ para Começar a Jogar!

With havin so much content do you ever run into any issues of plagorism or copyright violation? My blog has a lot of completely unique content I’ve either written myself or outsourced but it appears a lot of it is popping it up all over the web without my authorization. Do you know any solutions to help protect against content from being stolen? I’d certainly appreciate it.

Ao se cadastrar no fuwin,

você ganha um bônus de 100$ para começar sua

jornada no cassino com o pé direito! Não importa se você é um novato ou um apostador

experiente, o bônus de boas-vindas é a oportunidade perfeita para explorar

todas as opções que o site tem a oferecer. Jogue seus jogos favoritos, descubra novas opções de

apostas e aproveite para testar estratégias sem risco,

já que o bônus ajuda a aumentar suas chances de ganhar.

Cadastre-se hoje e comece com 100$!

O f12bet oferece uma excelente

oportunidade para quem deseja começar sua experiência

no cassino online com um bônus de 100$ para novos jogadores!

Ao se registrar no site, você garante esse bônus exclusivo que pode ser

utilizado em diversos jogos de cassino, como slots, roleta e poker.

Esse é o momento perfeito para explorar o mundo das

apostas com um saldo extra, aproveitando ao máximo suas apostas sem precisar investir um grande valor logo

de início. Não perca essa oportunidade e cadastre-se já!

Here, you can find a great variety of slot machines from top providers.

Users can experience traditional machines as well as feature-packed games with stunning graphics and bonus rounds.

Whether you’re a beginner or a casino enthusiast, there’s something for everyone.

casino games

All slot machines are available anytime and optimized for PCs and mobile devices alike.

You don’t need to install anything, so you can get started without hassle.

Platform layout is intuitive, making it convenient to find your favorite slot.

Register now, and enjoy the thrill of casino games!

Novos Usuários no pk55 Ganham

100$ de Bônus ao se Cadastrar!

On this platform, you can find a great variety of casino slots from famous studios.

Users can try out classic slots as well as feature-packed games with high-quality visuals and exciting features.

Even if you’re new or an experienced player, there’s a game that fits your style.

play aviator

Each title are instantly accessible 24/7 and optimized for desktop computers and mobile devices alike.

All games run in your browser, so you can get started without hassle.

The interface is intuitive, making it simple to browse the collection.

Sign up today, and dive into the world of online slots!

Ganhe 100$ de Bônus ao Se Registrar no ktobet – https://ktobet-88.com – Cadastre-se Agora!

No jonbet, Cadastre-se e Ganhe 100$ para Começar a Jogar!

Bônus de 100$ para Novos Jogadores no moverbet – Cadastre-se Agora!

Registre-se no luck 2 – https://luck-2.com Agora e Receba 100$ para

Suas Apostas!

I’m not sure why but this website is loading incredibly slow for me. Is anyone else having this issue or is it a problem on my end? I’ll check back later and see if the problem still exists.

Aproveite a oferta exclusiva do onebra para novos usuários e receba 100$ de

bônus ao se registrar! Este bônus de boas-vindas permite que você experimente

uma vasta gama de jogos de cassino online sem precisar gastar

imediatamente. Com o bônus de 100$, você poderá explorar jogos como roleta, blackjack, caça-níqueis e muito mais, aumentando suas chances de vitória desde o primeiro minuto.

Não perca essa chance única de começar com um valor significativo

– cadastre-se agora!

Novo no dobrowin?

Ganhe 100$ de Bônus Ao Se Registrar!

Ganhe 100$ no flames – https://flames-br.com ao Se Registrar – Comece a Apostar

Agora!

Ganhe 100$ para Apostar no allwin ao Se Registrar Hoje!